Summary: near-term RBA GDP forecasts increased; underlying inflation forecasts unchanged; jobless rate expected to peak under 8%, followed by gradual decline; labour market conditions improve “a bit faster than expected” but “remain soft overall”; near-term headline inflation forecasts lowered; RBA balance sheet, potential for negative interest policy to be under scrutiny.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In August’s SoMP, the opening sentence of the “Outlook” section stated, “During the first half of the year, the COVID-19 pandemic led to the most severe contraction in global and domestic economic activity in decades.” The RBA then noted the beginning of a recovery “as containment measures have been eased and fiscal and monetary policies have provided significant support.”

November’s opening sentence continued in this vein. “Following the largest contraction in decades, the global economy is in the early stages of recovery, as is Australia.” The RBA document then provided a caveat, stating “the level of GDP in a number of major economies is expected to remain below pre-pandemic forecasts for the next couple of years and a high degree of uncertainty continues to surround the outlook.”

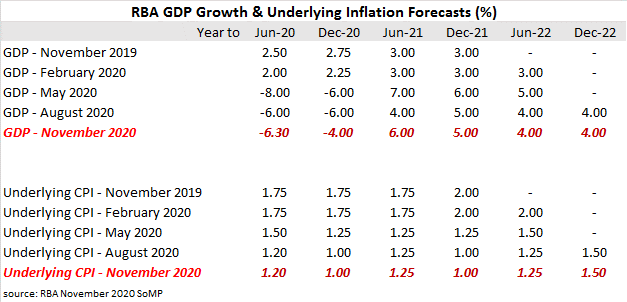

GDP growth rates in the early periods of the forecasts have increased while forecasts for later periods have been maintained. “This reflects stronger-than expected household consumption and additional policy support (including that announced in the Australian Government Budget), though a downward revision to resource exports has partly offset the firmer outlook for domestic demand.” The RBA’s forecast GDP growth rate for the year to December 2020 (see table) has been increased from -6% to -4% and its forecast for the year to June 2021 has been increased from 4% to 6%. Forecasts of later periods remained unchanged. The RBA’s latest forecasts assume “no additional large outbreaks and accompanying strict containment measures occur within Australia and that restrictions continue to be gradually lifted nationally, or are only tightened modestly for a limited time.”

The RBA’s underlying inflation forecasts remained unchanged. The RBA’s favoured measure of underlying inflation, the “trimmed mean” is expected to wobble through 2021 and 2022 and then rise in the second half of the latter. “Inflation remains very subdued at the end of the forecast period, reflecting the ample spare capacity that remains in the economy.” This statement is very similar to August’s analysis except for a dropping of a reference to low wages growth.

The RBA’s underlying inflation forecasts remained unchanged. The RBA’s favoured measure of underlying inflation, the “trimmed mean” is expected to wobble through 2021 and 2022 and then rise in the second half of the latter. “Inflation remains very subdued at the end of the forecast period, reflecting the ample spare capacity that remains in the economy.” This statement is very similar to August’s analysis except for a dropping of a reference to low wages growth.

In contrast to August’s Statement, more recent surveying by the RBA “suggests there is strong ongoing demand for household goods…putting upward pressure on prices.” However, “weak demand more broadly and the deflationary effects of ongoing rental price declines driven by the increased stock of rental properties and slower population growth” is expected to offset these effects. Wage growth “is also expected to remain very weak in the near term.”