Summary: Prices received by producers rise by 0.1% on average in November; increase in line with expectations; indicates “lack of pipeline inflation pressures”; annual “core” PPI rate rises; US bond yields down a little; PPI rise again driven by higher goods prices.

Around the end of 2018, the annual inflation rate of the US producer price index (PPI) began a downtrend which then continued through 2019. Months in which producer prices increased suggested the trend may have been coming to an end, only for it to continue, culminating in a plunge in April. Figures from subsequent months suggest a return to “normal” may be taking place.

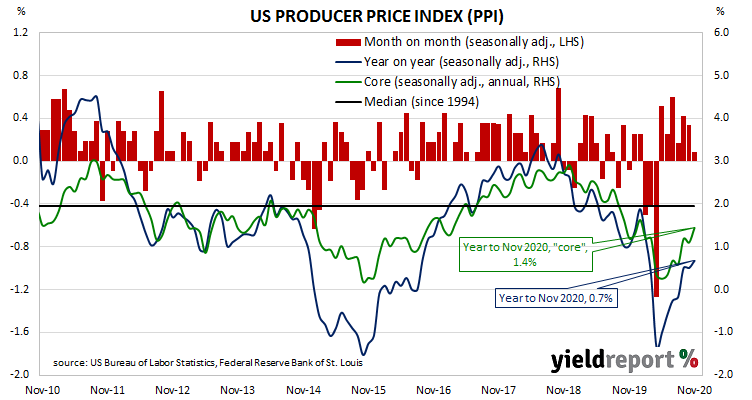

The latest figures published by the Bureau of Labor Statistics indicate producer prices rose by 0.1% after seasonal adjustments in November. The increase was in line with expectations but lower than October’s 0.3% rise. On a 12-month basis, the rate of producer price inflation after seasonal adjustments increased from 0.5% to 0.7%.

“The data indicate a lack of pipeline inflation pressures and they fit with the broader array of inflation releases to confirm a subdued price environment,” said ANZ economist Hayden Dimes.

PPI inflation excluding foods and energy rose by 0.1% in November after recording increases of 0.1% and 0.4% respectively in October and September. The annual rate accelerated from 1.1% in October to 1.4%.

The report was released on the same day as the University of Michigan’s latest reading of its consumer sentiment index and US Treasury bond yields moved a little lower across the curve. By the end of the day, the 2-year Treasury yield had shed 2bps to 0.12%, the 10-year yield had slipped 1bp to 0.90% while the 30-year yield finished 2bps lower at 1.62%.

The BLS stated higher prices for final demand goods accounted for all the month’s increase after they rose by 0.4% on average. Prices of services remained unchanged on average.