Summary: Household sentiment softens; breaks four-month run of improvements; “still points to healthy consumer sentiment”; still well above long-term average; all index components lower;

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April but, after a few months of to-ing and fro-ing, it then staged a full recovery.

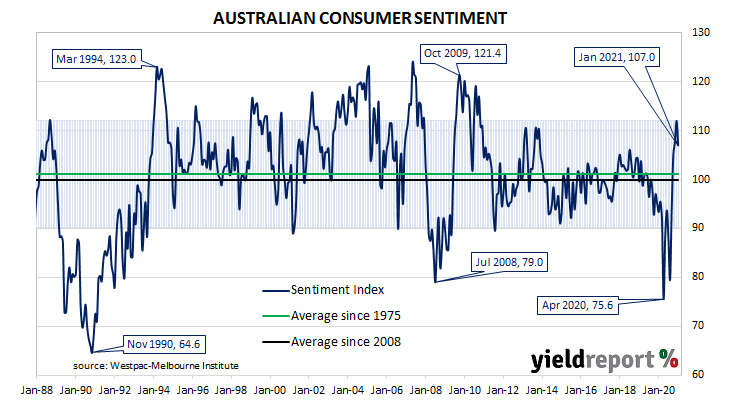

According to the latest Westpac-Melbourne Institute survey conducted in mid-January, household sentiment has deteriorated somewhat but remained quite robust. The Consumer Sentiment Index fell from December’s reading of 112.0 to 107.0, breaking a run of four consecutive months in which the index had increased.

Westpac chief economist Bill Evans said a pullback “was to be expected” given domestic border closures, clusters of infections in some states and rises in infections in the US and the UK. However, he noted the current reading “still points to healthy consumer sentiment.”

Treasury bond yields hardly moved on the day. By the close of business, the 3-year ACGB yields remained unchanged at 0.18%, the 10-year had slipped 1bp to 1.10% while the 20-year yield finished unchanged at 1.79%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.03%, did not change materially. At the end of the day, contract prices implied the cash rate would trade in a range between 0.030% and 0.055% through to mid-2022.

Any reading below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic. The latest figure is still substantially above the long-term average reading of just over 101.

All sub-indices were lower than a month ago, with the “12-month outlook” and the “5-year outlook” subindices recording “significant falls”.