Summary: Business conditions, confidence improve in February; “optimistic mood” broadly based across states, industry groups; capacity usage rate increases again; evidence labour demand growth will continue; results point to robust business sector recovery.

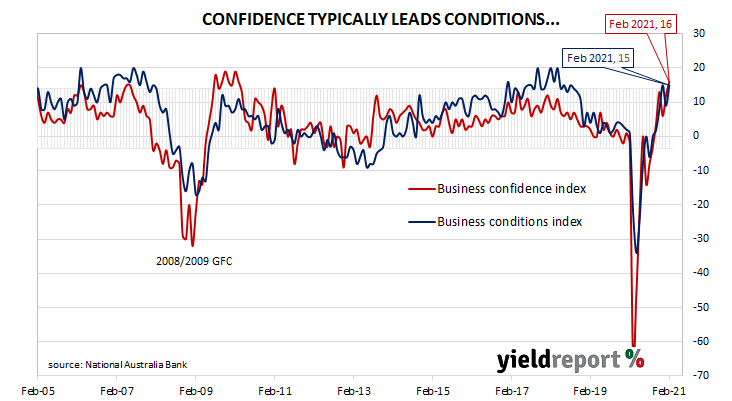

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s indices then began to slip, declining to below-average levels by the end of 2018. Forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 and the indices trended lower, hitting a nadir in April 2020 as pandemic restrictions were introduced. Conditions have improved markedly since then and NAB’s indices are both back to elevated levels.

According to NAB’s latest monthly business survey of over 400 firms conducted over the second half of February, business conditions improved. NAB’s conditions index registered 15, up from January’s revised reading of 9.

“Business conditions bounced to return to around multi-year highs…after slipping in the month prior, with trading, profitability and employment conditions all marking solid improvements,” said NAB chief economist Alan Oster.

Business confidence improved and NAB’s confidence index rose from January’s revised reading of +12 to +16. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

“This optimistic mood is broadly based across the states and across the broad industry groups. The roll-out of the vaccine is a major boost, reducing the risk of another round of state border closures,” said Westpac senior economist Andrew Hanlan.

Short-term Commonwealth Government bond yields declined while longer-term yields remained almost stable on the day, in contrast to higher US Treasury yields overnight. By the end of the day, the 3-year ACGB yield had lost 2bps to 0.27% while the 10-year yield remained unchanged at 1.77% and the 20-year yield finished 1bp higher at 2.45%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.03%, remained fairly stable. At the end of the day, contract prices implied the cash rate would inch up slowly to around 0.14% by mid-2022.