Summary: US CPI jumps in April; well above expectations; “core” rate triple expected figure; “broad-based”; non-food/energy commodities, used car/truck prices main drivers; probably reflection of pent-up demand, production bottlenecks; New York Fed UIG annual rate also up noticeably.

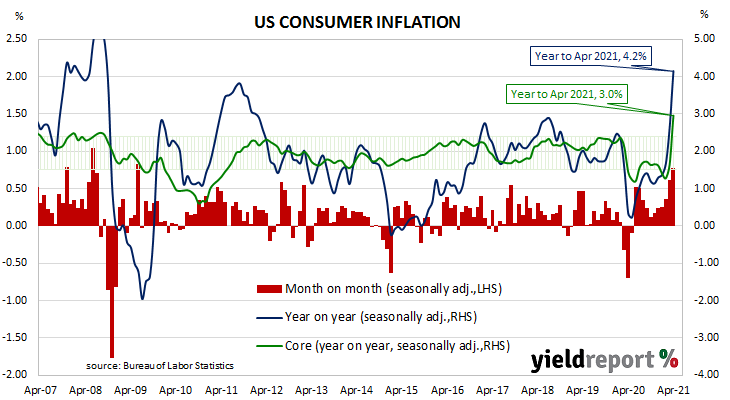

The annual rate of US inflation as measured by changes in the consumer price index (CPI) halved from nearly 3% in the period from July 2018 to February 2019. It then fluctuated in a range from 1.5% to 2.0% through 2019 before rising above 2.0% in the final months of that year. Substantially lower rates were reported from March 2020 to May 2020; falls in the index over these three months in 2020 are expected to raise annual inflation rates temporarily over the corresponding months in 2021.

The latest CPI figures released by the Bureau of Labor Statistics indicated seasonally-adjusted consumer prices rose by 0.8% on average in April. The result was well above the 0.2% increase which had been generally expected and above March’s 0.6% rise. On a 12-month basis, the inflation rate accelerated from March’s reading of 2.6% to 4.2%.

“Headline” inflation is known to be volatile and so references are often made to “core” inflation for analytical purposes. Core inflation, a measure of inflation which strips out the volatile food and energy components of the index, increased by 0.9% on a seasonally-adjusted basis for the month. The result was more than the expected 0.3% and triple March’s increase. The annual rate accelerated again, almost doubling from 1.6% to 3.0%.

“The key question for markets and for fears around inflation is how much of the rise in April is due to transitory one-offs, and how much reflects more permanent inflationary pressures,” said NAB senior economist Tapas Strickland. Westpac economist Lochlan Halloway noted “gains were broad-based.”

Longer-term US Treasury bond yields jumped on the day. By the close of business, the 2-year yield had inched up 1bp to 0.17% while 10-year and 30-year yields each finished 7bps higher at 1.69% and 2.42% respectively.

In terms of US Fed policy, expectations of any change in the federal funds range over the next 12 months remained fairly soft. May 2022 futures