By Ken Atchison, Principal, Atchison Consultants

An Intergenerational Report has been prepared on five occasions. In the latest report, it considers an outlook for the economy and the Australian Government’s budget over the next 40 years. This outlook has been profoundly affected by the COVID-19 pandemic.

Two initiatives are proposed which are relevant for intergenerational equity and require attention. State government finance and retirement income policy are areas of material spending.

Firstly, the Federal Government, through the Council of Australian Governments (COAG) or some equivalent such as the National Cabinet, should apply a financial discipline structure on the states. Secondly, future obligations from age pensions should be acknowledged upfront and financed, initially through a debt issue to an investment fund. This fund would then finance pension payments.

Government Debt

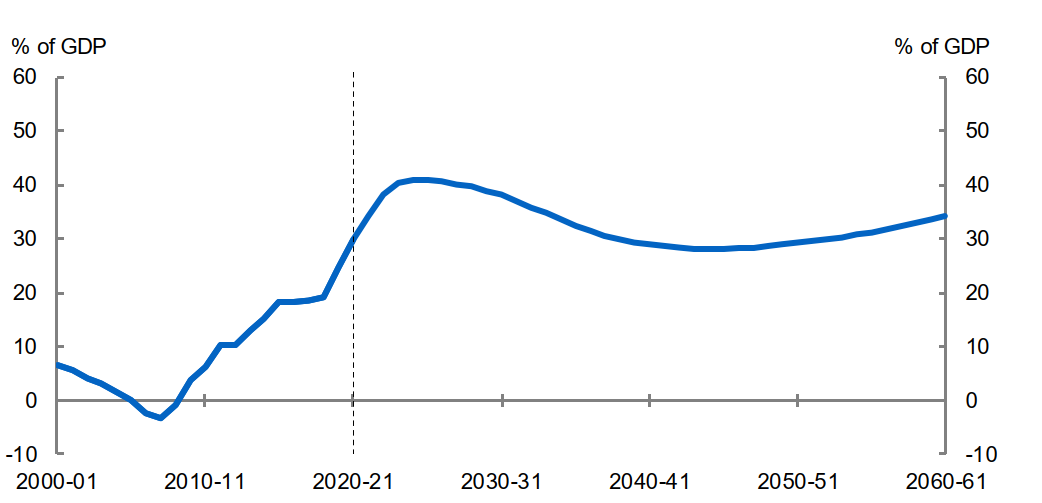

Net debt is projected to peak at 40.9% of GDP in 2024/25 before falling to 28.2% of GDP in 2044/45 and then increasing to 34.4% of GDP BY 2060/61 as shown in Chart 1.

Chart 1: Net Debt

Source: Treasury

This projection of debt confirms an expectation that continued prominence of government in the economy is accepted. When the states are included, the position is accentuated. Net debt including the states is estimated at 48.8%. Both Victoria and Queensland forecast increasing net debt to GSP of 27% and 61% respectively over the next three years. Neither state has addressed the future.

While the Australian net debt level is low compared with major developed countries, it is high in a historical context. In the cases of Queensland and Victoria, net debt is high on a comparative basis.

Two significant risks facing states with high debt levels are falling revenues and rising interest rates. States are heavily dependent on property-related taxes for revenue. Should residential property prices fall materially from current elevated levels, the consequences for state revenues will be severe.

Falling long-term government bond rates over fifty years are shown in Chart 2. Real interest rates have also been falling. Negative real interest rates, which are now evident, are not sustainable. Their presence has arisen through central banks, including the RBA, buying bonds in a process referred to as “quantitative easing” (QE). Additional buying pressure from these central bank purchases has resulted in higher bond prices, thus depressing bond yields to lows previously unseen in the past century.