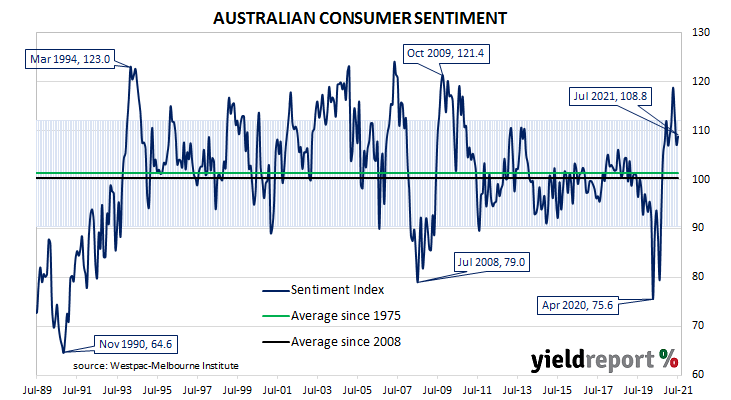

Summary: Household sentiment firms in July; holds up despite NSW fall as Vic, WA bounce back; still well above long-term average; four of five sub-indices higher; unemployment index slightly higher again; NSW concerns not spreading to other states so far.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again around July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery.

According to the latest Westpac-Melbourne Institute survey conducted in early July, household sentiment firmed after softening through May and June. The Consumer Sentiment Index increased from June’s reading of 107.2 to 108.8.

“Confidence has held up overall despite a sharp fall in New South Wales as other states, notably Victoria and Western Australia, recorded strong bounce-backs from COVID-related disruptions in June,” said Westpac chief economist Bill Evans. He noted the survey was held in the week in which Sydney residents were facing “stay at home” restrictions but before those restrictions were extended on 9 July.

Any reading of the Consumer Sentiment Index above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The latest figure is still well above the long-term average reading of just over 101.

Domestic Treasury bond yields increased modestly on the day, largely in line with overnight movements in US Treasury bond yields. By the close of business, the 2-year ACGB yield had crept up 1bp to 0.35% while 10-year and 20-year yields each finished 2bps higher at 1.35% and 1.93% respectively.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.03%, remained largely unchanged. At the end of the day, contract prices implied the cash rate would rise slowly, reaching 0.22% by October 2022.