06 August 2021

Summary: RBA forecasts September GDP contraction; 2021, 2022 GDP forecasts still robust; December 2021 core inflation rate raised, other periods unchanged; jobless rate expected to increase in short term but then fall by June 2022; headline inflation forecasts increased noticeably in year to December 2021, later periods raised more modestly.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In May’s SoMP, the opening sentence of the “Outlook” section stated, “The global economic outlook has firmed this year because of progress in vaccinations and additional fiscal support in some economies.” As far as Australia was concerned, the “economy is transitioning from recovery to expansion phase earlier and with more momentum than anticipated.”

August Outlook opened with: “A solid global economic recovery is underway but the near-term outlook for many economies remains uncertain and uneven.” On domestic matters, it stated, “Recent outbreaks of the Delta variant…and the resulting lockdowns, have introduced a high degree of uncertainty to the outlook for the second half of this year.”

“The RBA’s August Statement on Monetary Policy contains significant changes to the Bank’s near-term forecasts but retain a more upbeat view over the medium term horizon that frames the Bank’s policy decisions,” said Westpac senior economist Matthew Hassan.

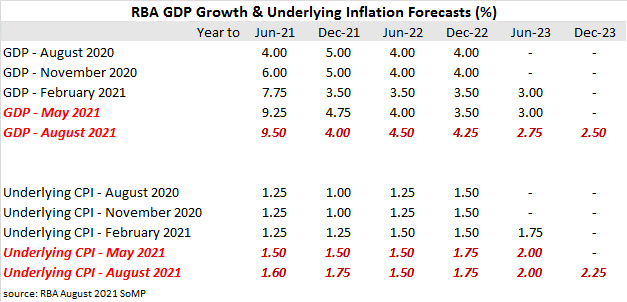

GDP growth rates have been amended to take into account what is expected to be at least a 1% contraction in the September 2021 quarter, a robust recovery in spending in the December quarter which then continues through the 2022 calendar year.

The RBA’s forecast GDP growth rate for the year to June 2021 (see table below) has been increased by 0.25 percentage points but the forecast for the year to December 2021 has been cut by 0.75% percentage points. The growth rate for the year to June 2022 had been raised by another 0.50 percentage points while the December 2022 growth rate has been upped by 0.75 percentage points. The June 2023 growth rate has been trimmed back to what is generally considered to be the trend growth rate at 2.75%.

“Activity will contract in the September quarter and some job losses are expected. Towards the end of this year, the economy is forecast to rebound from this setback as restrictions ease, as it has from previous lockdowns.” The RBA noted the Australian economy had been “in a strong position and fiscal policy is directly supporting households and businesses in the affected areas.” Its forecasts assumes “no further extended lockdowns are required.”

The RBA’s underlying inflation forecast for the year to December 2021 were raised by 0.25 percentage points but other forecast periods were left unchanged. “Underlying inflation has stabilised recently but will likely remain subdued over the next few quarters, given the decline in activity in the September quarter and the absence of broad-based inflationary pressures.” The RBA refers to average earnings per hour and the Wage Price Index as its preferred indicators of underlying inflation.

06 August 2021

Summary: RBA forecasts September GDP contraction; 2021, 2022 GDP forecasts still robust; December 2021 core inflation rate raised, other periods unchanged; jobless rate expected to increase in short term but then fall by June 2022; headline inflation forecasts increased noticeably in year to December 2021, later periods raised more modestly.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In May’s SoMP, the opening sentence of the “Outlook” section stated, “The global economic outlook has firmed this year because of progress in vaccinations and additional fiscal support in some economies.” As far as Australia was concerned, the “economy is transitioning from recovery to expansion phase earlier and with more momentum than anticipated.”

August Outlook opened with: “A solid global economic recovery is underway but the near-term outlook for many economies remains uncertain and uneven.” On domestic matters, it stated, “Recent outbreaks of the Delta variant…and the resulting lockdowns, have introduced a high degree of uncertainty to the outlook for the second half of this year.”

“The RBA’s August Statement on Monetary Policy contains significant changes to the Bank’s near-term forecasts but retain a more upbeat view over the medium term horizon that frames the Bank’s policy decisions,” said Westpac senior economist Matthew Hassan.

GDP growth rates have been amended to take into account what is expected to be at least a 1% contraction in the September 2021 quarter, a robust recovery in spending in the December quarter which then continues through the 2022 calendar year.

The RBA’s forecast GDP growth rate for the year to June 2021 (see table below) has been increased by 0.25 percentage points but the forecast for the year to December 2021 has been cut by 0.75% percentage points. The growth rate for the year to June 2022 had been raised by another 0.50 percentage points while the December 2022 growth rate has been upped by 0.75 percentage points. The June 2023 growth rate has been trimmed back to what is generally considered to be the trend growth rate at 2.75%.

“Activity will contract in the September quarter and some job losses are expected. Towards the end of this year, the economy is forecast to rebound from this setback as restrictions ease, as it has from previous lockdowns.” The RBA noted the Australian economy had been “in a strong position and fiscal policy is directly supporting households and businesses in the affected areas.” Its forecasts assumes “no further extended lockdowns are required.”

The RBA’s underlying inflation forecast for the year to December 2021 were raised by 0.25 percentage points but other forecast periods were left unchanged. “Underlying inflation has stabilised recently but will likely remain subdued over the next few quarters, given the decline in activity in the September quarter and the absence of broad-based inflationary pressures.” The RBA refers to average earnings per hour and the Wage Price Index as its preferred indicators of underlying inflation.

06 August 2021

Summary: RBA forecasts September GDP contraction; 2021, 2022 GDP forecasts still robust; December 2021 core inflation rate raised, other periods unchanged; jobless rate expected to increase in short term but then fall by June 2022; headline inflation forecasts increased noticeably in year to December 2021, later periods raised more modestly.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In May’s SoMP, the opening sentence of the “Outlook” section stated, “The global economic outlook has firmed this year because of progress in vaccinations and additional fiscal support in some economies.” As far as Australia was concerned, the “economy is transitioning from recovery to expansion phase earlier and with more momentum than anticipated.”

August Outlook opened with: “A solid global economic recovery is underway but the near-term outlook for many economies remains uncertain and uneven.” On domestic matters, it stated, “Recent outbreaks of the Delta variant…and the resulting lockdowns, have introduced a high degree of uncertainty to the outlook for the second half of this year.”

“The RBA’s August Statement on Monetary Policy contains significant changes to the Bank’s near-term forecasts but retain a more upbeat view over the medium term horizon that frames the Bank’s policy decisions,” said Westpac senior economist Matthew Hassan.

GDP growth rates have been amended to take into account what is expected to be at least a 1% contraction in the September 2021 quarter, a robust recovery in spending in the December quarter which then continues through the 2022 calendar year.

The RBA’s forecast GDP growth rate for the year to June 2021 (see table below) has been increased by 0.25 percentage points but the forecast for the year to December 2021 has been cut by 0.75% percentage points. The growth rate for the year to June 2022 had been raised by another 0.50 percentage points while the December 2022 growth rate has been upped by 0.75 percentage points. The June 2023 growth rate has been trimmed back to what is generally considered to be the trend growth rate at 2.75%.

“Activity will contract in the September quarter and some job losses are expected. Towards the end of this year, the economy is forecast to rebound from this setback as restrictions ease, as it has from previous lockdowns.” The RBA noted the Australian economy had been “in a strong position and fiscal policy is directly supporting households and businesses in the affected areas.” Its forecasts assumes “no further extended lockdowns are required.”

The RBA’s underlying inflation forecast for the year to December 2021 were raised by 0.25 percentage points but other forecast periods were left unchanged. “Underlying inflation has stabilised recently but will likely remain subdued over the next few quarters, given the decline in activity in the September quarter and the absence of broad-based inflationary pressures.” The RBA refers to average earnings per hour and the Wage Price Index as its preferred indicators of underlying inflation.