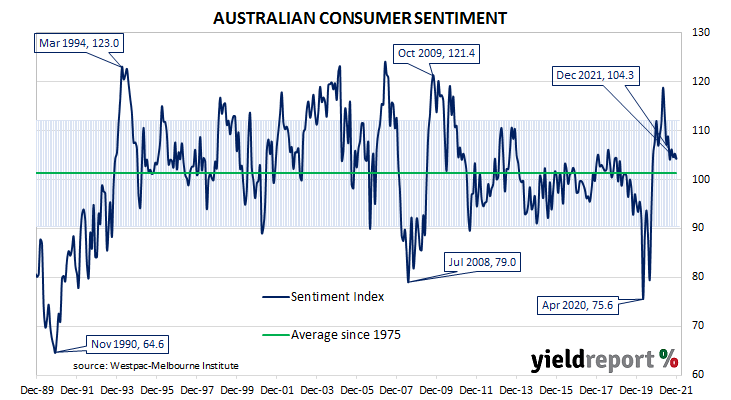

Summary: Household sentiment declines slightly in December; “clear difference” between NSW, Vic and Qld, WA, SA; still above long-term average; more negative responses to inflation, interest rates this year; three of five sub-indices lower.

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both readings then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery.

According to the latest Westpac-Melbourne Institute survey conducted in the week beginning 6 December, household sentiment has deteriorated slightly. Their Consumer Sentiment Index declined from November’s reading of 105.3 to 104.3.

“There was a clear difference in responses between the states hit hardest by recent Delta outbreaks and the rest of Australia. Both New South Wales and Victoria posted significant falls while sentiment was up in Queensland, Western Australia and South Australia,” said Westpac Chief Economist Bill Evans.

Any reading of the Consumer Sentiment Index above 100 indicates the number of consumers who are optimistic is greater than the number of consumers who are pessimistic. The latest figure is still above the long-term average reading of just over 101.

Domestic Treasury bond yields increased noticeably on the day, especially at the short end. By the close of business, the 2-year ACGB yield had jumped 17bps to 1.19%, the 10-year yield had gained 7bps to 1.62% while the 20-year yield finished 9bps higher at 2.18%.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.04%, remained fairly soft. At the end of the day, contract prices implied the cash rate would not reach the RBA’s 0.10% target rate until April 2022 and then rise to 0.80% by December 2022.

Evans noted a “heightened sensitivity to virus developments in those states where there is likely more concern about the newly emerging Omicron strain and the continued circulation of COVID locally.” However, he also said there were other factors at work which were making consumers more cautious. Negative responses to inflation and interest rates appear to be more common this year than at the end of 2020.

Three of the five sub-indices registered lower readings, with the “Time to buy a major household item” sub-index posting the largest monthly percentage loss. Readings for the sub-indices “Family finances versus a year ago” and “Family finances next 12 months both improved.

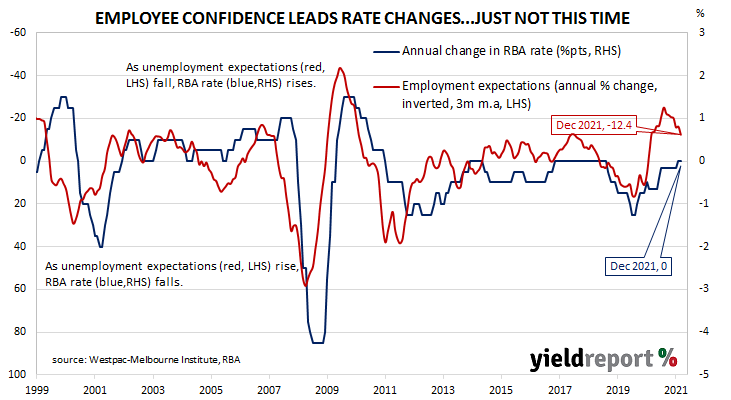

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, rose from 95.3 to 104.1. Higher readings result from more respondents expecting a higher unemployment rate in the year ahead.