Summary: US consumer confidence remains weak in January; University of Michigan index below consensus figure; views of present conditions, future conditions both deteriorate; decline attributed to infections, escalating inflation rate.

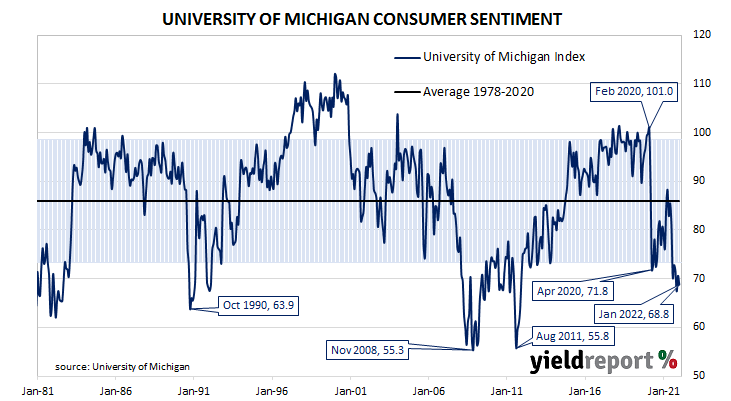

US consumer confidence started 2020 at an elevated level but, after a few months, surveys began to reflect a growing unease with the global spread of COVID-19 and its reach into the US. Household confidence plunged in April 2020 and then recovered in a haphazard fashion, generally fluctuating at below-average levels according to the University of Michigan. The University’s measure of confidence had recovered back to the long-term average by April 2021 but then it plunged again in the September quarter.

The latest survey conducted by the University indicates confidence among US households remained weak on average in January. The preliminary reading of the Index of Consumer Sentiment registered 68.8, below the generally expected figure of 70.0 and December’s final figure of 70.6. Consumers’ views of current conditions and expectations regarding future conditions both deteriorated in comparison to those held at the time of the December survey.

“While the Delta and Omicron variants certainly contributed to this downward shift, the decline was also due to an escalating inflation rate. Three-quarters of consumers in early January ranked inflation, compared with unemployment, as the more serious problem facing the nation,” said the University’s Surveys of Consumers chief economist, Richard Curtin.

US Treasury bond yields moved noticeably higher on the day. By the close of business, the 2-year Treasury yield had gained 7bps to 0.96%, the 10-year yield had added 9bps to 1.79% while the 30-year yield finished 8bps higher at 2.12%.

Less-confident households are generally inclined to spend less and save more; some decline in household spending could be expected to follow. As private consumption expenditures account for a majority of GDP in advanced economies, a lower rate of household spending growth would flow through to lower GDP growth if other GDP components did not compensate.