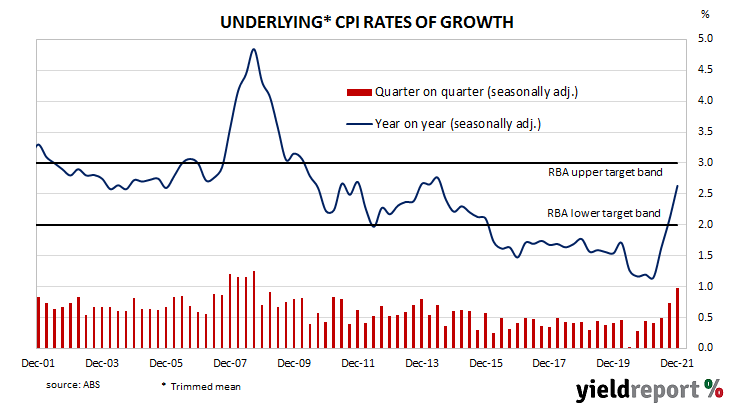

Summary: Annual Inflation rate accelerates to 3.7% in December quarter, above market expectations; RBA preferred measure rises from 2.1% to 2.6%, above expected; housing, transport costs again main drivers of result.

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020, despite the efforts of the RBA to increase them through historically low cash rates.

Consumer price indices for the December quarter have now been released by the ABS and the seasonally-adjusted inflation rate posted a 1.3% rise. The increase was noticeably higher than the generally expected figure of 1.0% and the September quarter’s 0.8%. On a 12-month basis, the seasonally-adjusted rate accelerated from 3.0% after revisions to 3.7%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 1.0% over the quarter, above market expectations of a 0.7% increase and the September quarter’s 0.7% rise. The 12-month inflation rate rose from 2.1% to 2.6%.

The report was released on the same day as NAB’s December business report and Commonwealth Government bond yields increased on the day. By the close of business, the 3-year ACGB yield had gained 5bps to 1.46%, the 10-year yield had inched up 1bp to 1.97% while the 20-year yield finished 3 bps higher at 2.48%.

In the cash futures market, expectations of a change in the actual cash rate, currently at 0.03%, firmed a little in favour of earlier rate rises. At the end of the day, contract prices implied the cash rate would rise gradually from the current rate of 0.050% to 0.14% by April, then increase to 0.58% by August and then to 1.25% by February 2023.

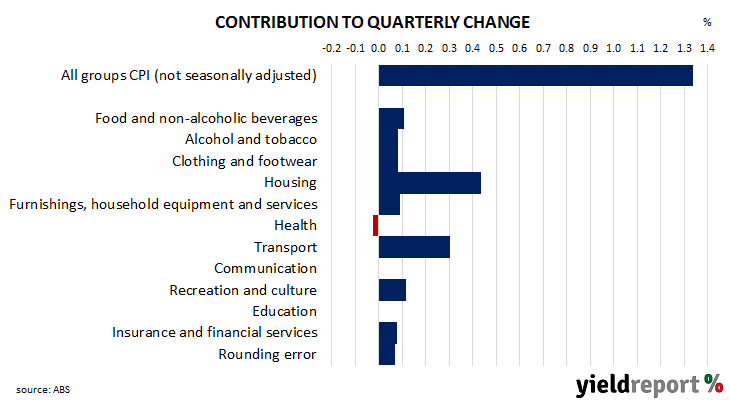

The main driver of the headline inflation figure in the quarter again was a 1.8% rise in housing costs, contributing 0.43 percentage points of the 0.76% (unadjusted) increase over the quarter. Likewise, transport prices also had a significant influence on the quarter, rising by 2.8% and contributing 0.30% percentage points to the quarterly total.

Here’s what a few economists thought about the figures:

Justin Smirk, Westpac

The big surprise was the 1.0% rise in the trimmed mean, well exceeding the market expectation of 0.7%, highlighting the broad spread of this inflation surprise. The 1.0% was the largest quarterly rise in the trimmed mean since 1.2% in September 2008, taking the annual pace to 2.6%, the fastest pace of core inflation since June 2014.

We will process all this data and review of near-term CPI forecasts based on this new information. While we don’t know what the overall impact will be it is clear that, at 3.5%, the current pace of inflation is running ahead of where we thought it would be at the end of 2021, pointing to upside risk to our June 2022 forecasts of 3.3% of the CPI, 2.9% for the trimmed mean.

Hayden Dimes, ANZ

Even before today’s print we had highlighted the RBA would need to revise its outlook for inflation and shift its forward guidance. Some of the inflation being observed is likely to subside, namely on the tradeable goods side where the friction in global supply chains is clearly having an impact. But the much higher starting point for inflation means the RBA will almost certainly need to adjust its forward guidance to acknowledge a rate hike is possible this year. We suspect the RBA won’t shift to a 2022 rate hike as being its central case, likely wanting to see wages growth clearly accelerate. But earlier than expected evidence of this is also possible.

Taylor Nugent, NAB

Following today’s data, the RBA will need to revise up their inflation track to show underlying inflation at or above the top of their band by mid-year. The RBA’s tolerance for inflation at the top of the 2%-3% band, or above for a time will be key to understanding how patient the RBA is prepared to be as it waits to until wages growth is closer to 3% plus. After six years of missing its inflation target, the RBA has said it wants to make sure inflation will be sustained at target with wages growth a key input in judging sustainability.

Governor Lowe noted back in November 2021 though “the trajectory for inflation is also important, with a slow drift up in underlying inflation having different policy implications to a sharp rise.” With underlying inflation already higher than the RBA was forecasting at any point over their forecasts to end 2023, that tolerance will be tested during 2022.

Looking to the RBA next week, the RBA’s upside scenario for the economy is probably now consistent with a rate hike in late 2022, while the central scenario is now likely to sit in early 2023 based on the RBA’s likely wages outlook. This is vastly different to the RBA’s previous characterisation of being in 2024, with 2023 only then described as plausible and 2022 being classed as implausible. As for QE, today’s data further support our expectation that the RBA will end QE purchases at its February meeting.