Summary: RBA cuts GDP forecast to June 2022, raises June 2023 forecast; underlying inflation forecasts noticeably higher; jobless rate expected to fall to 3.75% by June; headline inflation forecasts increase noticeably again; further rate increases over the months ahead.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In February’s SoMP, the opening sentence of the “Outlook” section stated, “Global economic growth picked up in the second half of 2021 following the lifting of mobility restrictions and is forecast to remain above trend in 2022.”

As far as Australia was concerned, “The Australian economy had established solid momentum prior to the Omicron outbreak at the end of 2021. Domestic economic activity bounced back strongly in the December quarter, driven by a surge in household spending as restrictions relating to the Delta outbreak were eased.”

May’s Outlook opened with “Global economic growth is forecast to be slower and inflation higher than forecast a few months ago. Inflation has been persistently high because many advanced economies are at or close to full employment, commodity prices have risen sharply and there are ongoing supply disruptions.”

On domestic matters, it stated, “A strong expansion in the Australian economy is underway. This is expected to continue over the forecast period, despite the slowdown in global growth.”

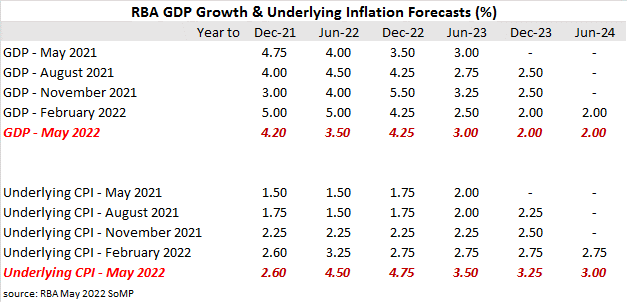

Even so, there has been some significant changes made. The RBA’s GDP growth forecast for the year to June 2023 (see table below) has been reduced by 1.50 percentage points while the forecast for the year to June 2023 has been raised by 0.50 percentage points.

The RBA’s underlying inflation forecast have also been noticeably raised. The forecast for the year to June 2022 was raised by 1.25 percentage points while forecasts for the years to December 2022 and June 2023 were raised by 2.00 percentage points and 0.75 percentage points respectively. The forecast for the year to December 2023 was raised by 0.50 percentage points.

“As some of the current cost pressures reflect supply bottlenecks domestically and abroad and are likely to moderate over time, headline and underlying inflation are forecast to return to the top of the 2% to 3% target range by the end of the forecast period. Higher labour costs in response to a tight labour market are expected to become the primary driver of inflation outcomes later in the forecast period.”

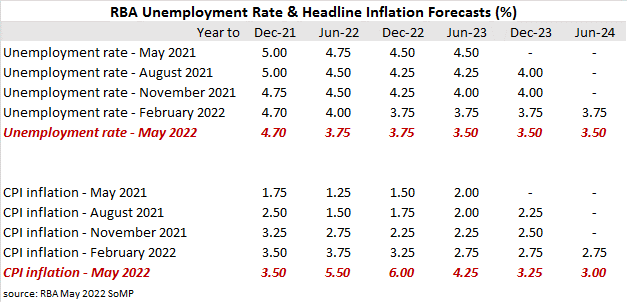

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate has fallen to 4.0% at the end of March. The RBA now expects it to decline to 3.75% by the end of June and then to 3.50% in June 2023. The forecasts then remain unchanged over the remainder of the forecast periods.

“Employment is forecast to grow strongly during 2022, consistent with the ongoing strength in leading indicators of labour demand, before moderating thereafter in line with activity.”

Headline inflation forecasts again have been increased noticeably. The years to June 2022 and December 2022 have had their respective forecasts raised by 1.75% and 2.75%. The forecast for the year to June 2023 has now been also raised considerably, increasing from 2.75% to 4.25%.

The RBA has added new dwelling costs to fuel prices as the major factors driving headline inflation. “Headline inflation is forecast to be well above trimmed mean inflation in the near term, mainly due to the prices of fuel and new dwellings, but to be broadly in line with underlying inflation thereafter.”

Commonwealth bond yields moved significantly higher on the day of the Statement’s release, generally in line with the movements of their US Treasury bond yields overnight. By the end of the day, the 3-year ACGB yield had gained 7bps to 3.17%, the 10-year yield had increased by 8bps to 3.51% while the 20-year yield finished 7bps higher at 3.81%.

“The RBA’s May SoMP was broadly in line with the messaging from Governor Lowe on Tuesday of “further increases in interest rates will be necessary over the months ahead” and of the cash rate lifting to around 2.5% over the next few years,” said NAB economist Taylor Nugent.