By Chris Owens, analyst, Atchison Consultants

Australian real estate investment trusts (AREITs), as represented by the S&P/ASX 200 AREIT Index, returned +0.6% in the month ending 30 April 2022. AREITs underperformed the S&P/ASX 200 return of +1.4% over the month.

Over the 12 months to April 2022, AREITs posted a strong total return of 15.1%, outperforming the S&P/ASX 200 return of 10.2%

Sector Performance

Table 1 below shows the performance of AREITs for various periods ending 30 April 2022.

Over the 3 years and 5 years to the end of April, the sector produced total returns of 6.3% and 7.4% per annum respectively.

Sector returns were led by Industrial AREITs at +4.6%, followed by Office AREITs at +2.0%, Retail AREITs at +0.2% and Diversified AREITs at -2.4%.

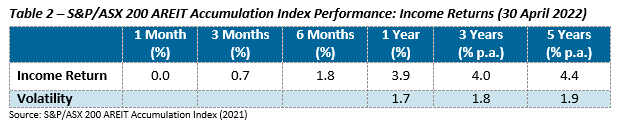

Table 2 below shows the income performance of AREITs for various periods ending 30 April 2022.

The income component of the total return was 3.9% for the 12-month period to April. Annual volatility of income returns was 1.8%, which is low when compared with other asset classes.

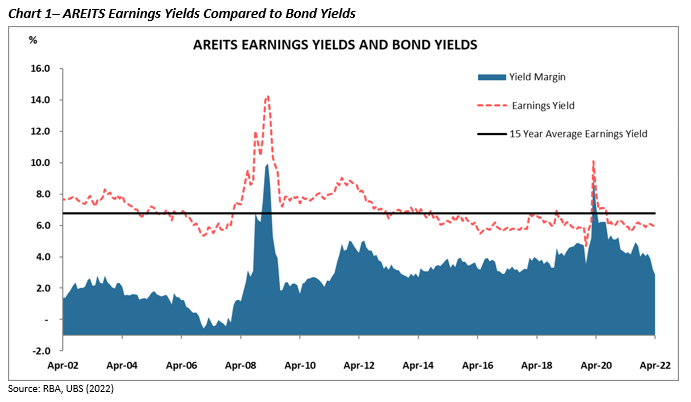

AREITs were trading at an earnings yield of approximately 6.0% at the end of the month, higher than yields of both cash and Commonwealth Government bonds. However, the spread of the earnings yield over the 10-year government bond yield fell from 3.2% to 2.9% as bond yields rose substantially.

Changes over time of the spread between the earnings yield of AREITs and the 10-year government bond yield are shown in Chart 1.

Market Review

For the year to date, the ASX 200 AREIT index has fallen 6.6%, while the ASX 200 Accumulation index rose +1.4%. The underperformance of AREITs can be attributed to increased bond yields and the prospect of higher interest rates.

The spread between AREIT earnings yields and 10-year Government Bond yields has tightened as bond yields hit 3.1% in April. As real estate offers a long duration and steady income stream, AREITs have long been seen as a bond proxy. Therefore, any increase in the risk free rate will see the attractiveness of AREITs fall. When conducting a valuation on a property stock, the risk free rate is considered when applying the discount rate to future cash flows, leaving property analysts to de-value stocks. According to UBS, for every 0.5% increase in the 10-year Government Bond rate, AREITs will fall by 6%.

For the 12 months to March 2022, the Australian inflation rate rose to 5.1%, well outside the RBA’s 2-3% inflation target. This had led the market to anticipate numerous cash rate increases. Many AREITs have taken advantage of falling interest rates in recent years and have taken on variable-rate debt, making AREITs vulnerable to increased debt expenses. According to the UBS, 36% of the AREIT sector carries variable-rate debt, compared with just 20% 3 years ago. UBS estimates that for every 1% increase in the cash rate, AREIT earnings will fall by 4%.

AREITs, such as Scentre Group for example, may be able to hedge against inflation with CPI-linked rental increases. However, they will not be able to escape the impact inflation will have on increased borrowing costs.