By Chris Owens, analyst, Atchison Consultants

Australian real estate investment trusts (AREITs), as represented by the S&P/ASX 200 AREIT Index, returned -3.5% in the month ending 31 August 2022. AREITs underperformed the S&P/ASX 200 return of 1.2% over the month.

Over the 12 months to August 2022, AREITs posted a total return of -11.1%, underperforming the S&P/ASX 200 return of -3.4%.

Sector Performance

Table 1 below shows the performance of AREITs for various periods ending 31 August 2022.

source: S&P/ASX 200 AREIT Accumulation Index (2022)

Over the 3 years and 5 years to the end of August, the sector produced total returns of -1.5% and 5.8% per annum respectively.

Sector returns were led by Retail AREITs returning -0.9%, Diversified AREITs returning -3.0%, with Industrial AREITs returning -4.8% and Office AREITs returning -7.9%.

source: S&P/ASX 200 AREIT Accumulation Index (2022)

The income component of the total return was 3.8% for the 12-month period to August. Annual volatility of income returns was 1.6%, which is low when compared with other asset classes.

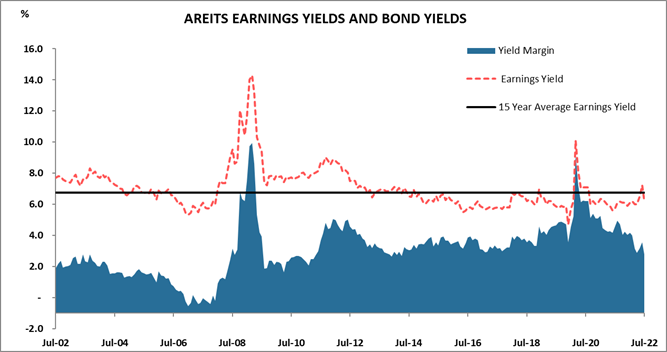

AREITs were trading at an earnings yield of approximately 6.5% at the end of the month, higher than yields of both cash and Commonwealth Government bonds. However, the spread of the earnings yield over the 10-year government bond yield remained steady at 2.9%.

Changes over time of the spread between the earnings yield of AREITs and the 10-year government bond yield are shown in Chart 1.

source: RBA, UBS (2022)

Market Review

A valuation gap between AREIT investors and asset owners is having an impact on deal making in the sector, with investors betting on listed property valuations to fall, while asset owners (landlords) are not. According to Credit Suisse, the drop in 10 of the largest AREITs share prices implies asset prices have dropped 15%, or nearly $20 billion.

The drop in AREIT stock prices has had an impact on deal making and transactions. The average annual figure for transactions is usually around $6 billion. For the YTD this figure sits at just $2 billion, as investors anticipate more rate rises as the RBA attempts to reduce inflationary pressures, which generally lead to lower valuations for most property.

According to the Resolution Capital Global Securities June report, Australian REITs are more exposed to rising rates than global REITs, which hedge up to 90% of their debt and for periods of six years or more. In comparison, 37% of AREITs have non-hedged debt, while the average hedge term is for less than four years.