Summary: Non-farm payrolls up 263,000 in September, slightly more than expected; previous two months’ figures revised up by 11,000; jobless rate falls to 3.5%, participation rate slips to 62.3%; too solid to support a ‘pivot’ narrative; jobs-to-population ratio steady at 60.1%; underutilisation rate falls from 7.0% to 6.7%; annual hourly pay growth slows from 5.2% to 5.0%.

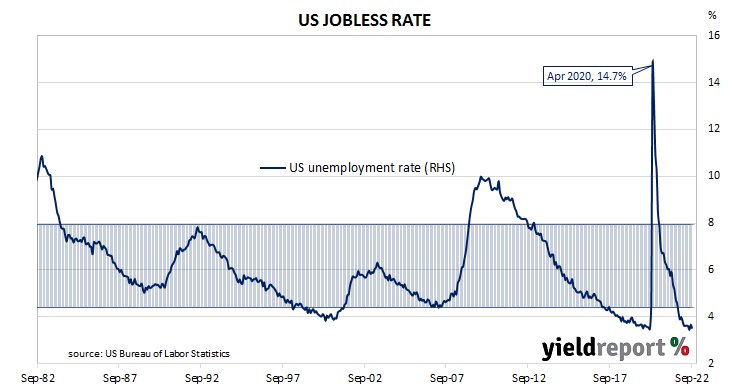

The US economy ceased producing jobs in net terms as infection controls began to be implemented in March 2020. The unemployment rate had been around 3.5% but that changed as job losses began to surge through March and April of 2020. The May 2020 non-farm employment report represented a turning point and subsequent months provided substantial employment gains. Changes in recent months have been generally more modest but still above the average of the last decade.

According to the US Bureau of Labor Statistics, the US economy created an additional 263,000 jobs in the non-farm sector in September. The increase slightly more than the 250,000 which had been generally expected but less than the 315,000 jobs which had been added in August after revisions. Employment figures for July and August were revised up by a total of 11,000.

The total number of unemployed decreased by 261,000 to 5.753 million while the total number of people who are either employed or looking for work decreased by 57,000 to 164.689 million. These changes led to the US unemployment rate falling from 3.7% to 3.5% as the participation rate slipped from August’s rate of 62.4% to 62.3%.

“It was ‘good news is bad news’ for US Payrolls which were a touch better than expected and seen as too solid to support a ‘pivot’ narrative,” said NAB senior economist Tapas Strickland.

US Treasury yields rose noticeably on the day. By the close of business, the 2-year yield had gained 12bps to 4.48%, the 10-year yield had added 7bps to 3.85% while the 30-year yield finished 4bps higher at 3.81%.

In terms of US Fed policy, expectations of a steeper path for the federal funds rate over the next 12 months hardened. At the close of business, November contracts implied an effective federal funds rate of 3.76%, 68bps higher than the current spot rate, while December contracts implied 4.145%. September 2023 futures contracts implied an effective federal funds rate of 4.48%, 140bps above the spot rate.

“The drop in job openings in August does suggest labour demand may be easing from the unprecedented levels seen recently, but there’s a long way to go before the labour market will be in a better, that is, less inflationary, balance,” said ANZ Head of Australian Economic David Plank.

One figure which is indicative of the “spare capacity” of the US employment market is the employment-to-population ratio. This ratio is simply the number of people in work divided by the total US population. It hit a cyclical-low of 58.2 in October 2010 before slowly recovering to just above 61% in late-2019. September’s reading remained unchanged at 60.1%, still some way from the April 2000 peak reading of 64.7%.

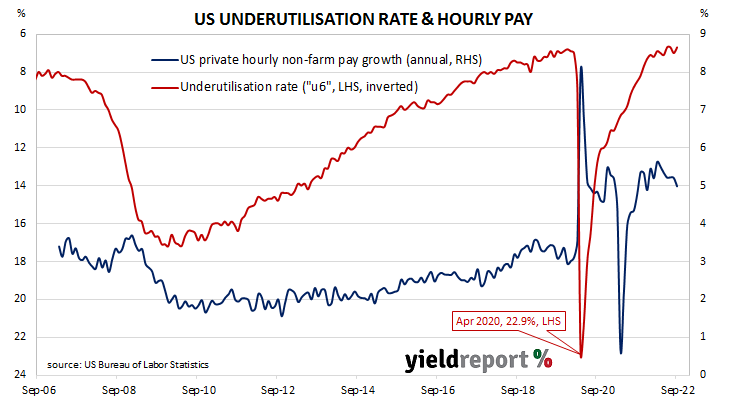

Apart from the unemployment rate, another measure of tightness in the labour market is the underutilisation rate and the latest reading of it registered 6.7%, down from 7.0% in August. Wage inflation and the underutilisation rate usually have an inverse relationship; however, hourly pay growth in the year to September still declined from 5.2% to 5.0%.