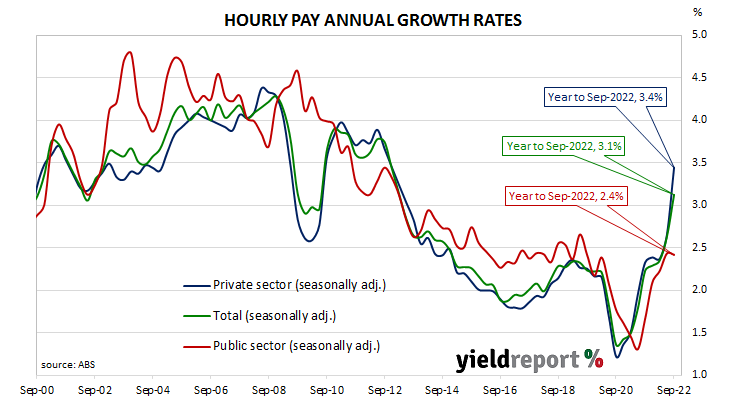

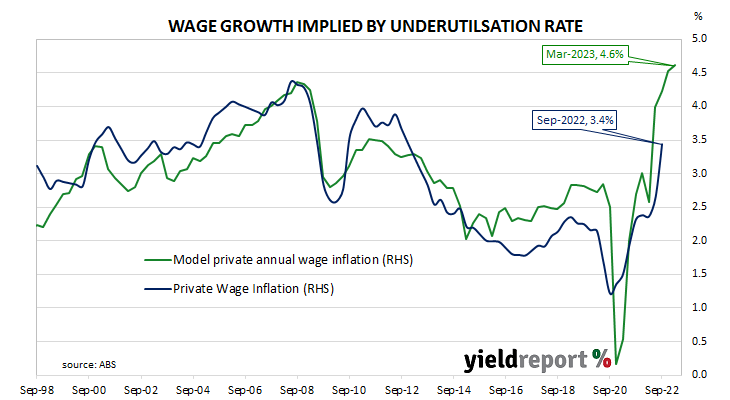

Summary: September quarter wages up 1.0%, slightly above expectations; annual growth rate speeds up from 2.6% to 3.1%; reflects larger increase to minimum and award wages; private sector wages up 3.4% over year, public sector up 2.4%; underutilisation rate implies higher wage growth.

After unemployment increased and wage growth slowed during the GFC, a resources investment boom prompted a temporary recovery back to nearly 4% per annum. However, from mid-2013 through to the September quarter of 2016, the pace of wage increases slowed, until mid-2017 when it began to slowly creep upwards. After remaining fairly stable at around 2.2% per annum from September 2018 to March 2020, the growth rate slowed significantly in the June and September quarters of 2020 before speeding up in 2021 and 2022.

According to the latest Wage Price Index (WPI) figures published by the Australian Bureau of Statistics (ABS), hourly wages grew by 1.0% in the September quarter. The increase was slightly above expectations of a 0.9% rise as well as the June quarter’s 0.8%. On an annual basis, the growth rate sped up from 2.6% to 3.1%.

“The solid report reflected the larger increase to minimum and award wages, which had flow-on effects to some enterprise bargaining agreements and individual arrangements,” said ANZ economist Madeline Dunk. “Affected sectors, like retail trade and administrative services, were strong. While the magnitude of the increase is unlikely to be repeated, minimum wage rises for hospitality will come through in Q4.”

Domestic Treasury bond yields mostly moved lower on the day following noticeable falls of US Treasury yields overnight. By the close of business, 3-year and 10-year ACGB yields had both lost 4bps to 3.29% and 3.73% respectively while the 20-year yield finished 1bp higher at 4.20%.

In the cash futures market, expectations regarding future rate rises firmed. At the end of the day, contracts implied the cash rate would rise from the current rate of 2.81% to average 2.97% in December and then increase to an average of 3.185% in February. May 2023 contracts implied a 3.62% average cash rate while August 2023 contracts implied 3.79%.

Wages in the private and public sectors grew by 1.2% and 0.6% respectively in the quarter. Over the past 12 months, wages in the private sector increased by 3.4% while public sector wages grew by 2.4%. Annual wage growth in the two sectors had been at 2.6% and 2.4% respectively in the June quarter.

The “underutilisation rate” is simply the sum of the unemployment and underemployment rates as per ABS monthly statistics. It has a good correlation with private wage growth two quarters in the future and thus it is useful as a leading indicator. However, differences can open up from time to time. September’s underutilisation rate suggests private wage growth is likely to continue accelerating.

Each quarter the ABS surveys around 3,000 private and public enterprises regarding a sample of jobs in each workplace to measure changes in the price of labour across 18,000 jobs. The results are used to construct the Wage Price Index in a manner similar to the construction of the Consumer Price Index (CPI). Changes in the WPI over time provide a measure of changes in wages and salaries, independently of the type or quantity of work.