Summary: Australia’s GDP up 0.6% in September quarter, slightly less than expected; rates’ effects apparent; inflationary pressures escalating through Q3; higher household consumption, exports, imports major influences on result; growth private-sector driven.

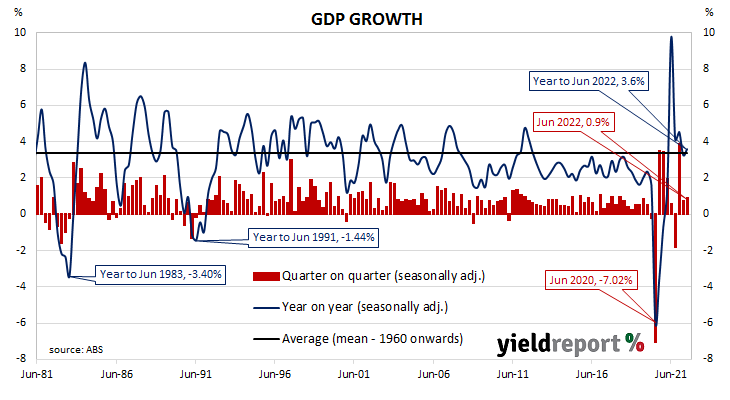

Since the “recession we had to have” as the recession of 1990/91 became known, Australia’s GDP growth has been consistently positive, with only the odd negative quarter here and there. However, Australia’s first recession in nearly thirty years was inevitable in 2020 once governments introduced restrictions which shut businesses and limited people’s movements for an extended period of time. Positive growth rates resumed in the September 2020 quarter until restrictions were reintroduced in eastern states in the September 2021 quarter.

The latest figures released by the ABS indicate GDP rose by 0.6% in the September quarter. The increase was slightly less than the 0.7% rise which had been generally expected as well as lower than the June quarter’s 0.9%. On an annual basis, GDP expanded by 5.9%, up from 3.2% after revisions in the June quarter.

“The effect of higher rates is apparent in the accounts, in housing and property turnover as well as in some components of consumption,” said Westpac chief Economist Bill Evans. “Food, household furnishings and equipment and recreation all contracted in the quarter.”

Commonwealth Government bond yields fell on the day, somewhat in line with movements of their US Treasury counterparts overnight. By the close of business, the 3-year ACGB yield had lost 2bps to 3.08%, the 10-year yield had shed 4bps to 3.36% while the 20-year yield finished 2bps lower at 3.71%.

In the cash futures market, expectations regarding future rate rises firmed a touch. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.06% to average 3.18% in February and then increase to an average of 3.46% in May. August 2023 contracts implied a 3.635% average cash rate while November 2023 contracts implied 3.655%.

“While these data are now a little dated and don’t fully reflect the impact of the 300bps of cash rate increases over the past eight months, they show that inflationary pressures were escalating through Q3, “said ANZ senior economist Felicity Emmett.” She expects further rate rises from the RBA with “any pause in the tightening cycle remains some way off.”

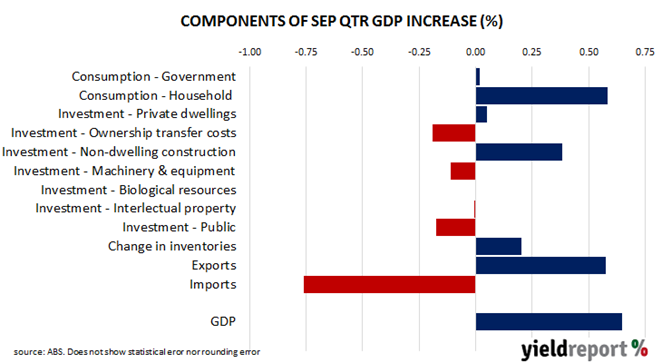

Household consumption spending increased by $3.2 billion, contributing 0.6 percentage points to the quarter’s overall result, while a $3.1 billion rise in exports also contributed around 0.6 percentage points. Imports were $4.2 billion higher than in the previous quarter, subtracting around 0.8 percentage points.

“Growth was private-sector driven, with no contribution from government spending in the quarter, while an acceleration in inventory accumulation, particularly in mining and retail, was offset by a drag from trade as import growth outpaced exports,” said Morgan Stanley Australia economist Chris Read.