Summary: Leading index growth rate down a touch in December; points to below-trend growth in first half of 2023; reading implies annual GDP growth of around 1.75%; ACGB yields higher; rate-rise expectations firm; consumer sector to be main driver of any upcoming slowdown.

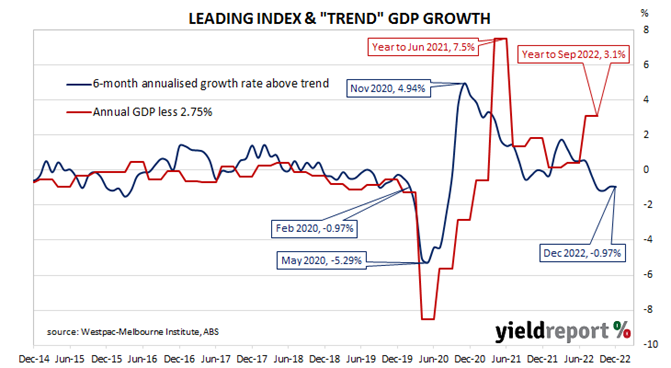

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings spiked towards the end of 2020 but then trended lower through 2021 and 2022.

The December reading of the six month annualised growth rate of the indicator registered -0.97%, down a touch from November’s figure of -0.97% after it was revised from -0.92%.

“The Index continues to point to below-trend growth in the first half of 2023,” said Westpac Chief Economist Bill Evans. “Westpac concurs with that view although we expect the slowdown in the Australian economy in 2023 to be more apparent in the second half of the year when growth is forecast to stagnate after running at a 2% annual pace in the first half.”

Index figures represent rates relative to “trend” GDP growth, which is generally thought to be around 2.75% per annum in Australia. The index is said to lead GDP by “three to nine months into the future” but the highest correlation between the index and actual GDP figures occurs with a three-month lead. The current reading thus represents an annual GDP growth rate of around 1.75%.

This latest reading came out on the same day as the December quarter’s CPI report and domestic Treasury bond yields moved higher on the day despite moderate falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had gained 9bps to 3.15%, the 10-year yield had added 4bps to 3.51% while the 20-year yield finished 2bps higher at 3.89%.

In the cash futures market, expectations regarding future rate rises firmed. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.07% to average 3.24% in February and then increase to an average of 3.625% in May. August contracts implied a 3.74% average cash while November contracts implied 3.72%.

Evans expects consumer spending to be the main driver of any upcoming slowdown “as elevated interest rates and negative real wages growth take their toll on spending.” However, he also expects households which built up their savings during the pandemic to be somewhat insulated.