Summary: Annual Inflation rate accelerates to 7.8% in December quarter, above expectations; RBA preferred measure rises from 6.1% to 6.9%; recreation prices main drivers of result.

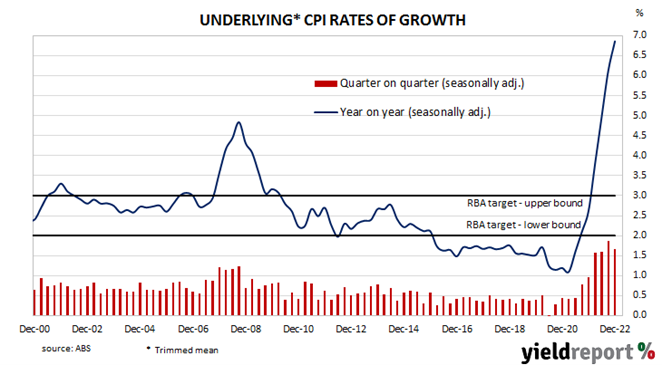

In the early 1990s, high rates of inflation in Australia were reined in by the “recession we had to have” as it became known. Since then, underlying consumer price inflation has averaged around 2.5%, in line with the midpoint of the RBA’s target range. However, the various measures of consumer inflation trended lower during the decade after the GFC and hit a multi-decade low in 2020 before rising significantly in the quarters following September 2021.

Consumer price indices for the December quarter have now been released by the ABS and the seasonally-adjusted inflation rate posted a 1.8% rise. The increase was above consensus expectations of a 1.6% rise but slightly less than the September quarter’s 1.9%. On a 12-month basis, the seasonally-adjusted rate accelerated from 7.3% to 7.8%.

The RBA’s preferred measure of underlying inflation, the “trimmed mean”, increased by 1.7% over the quarter, more than the 1.5% increase which had been generally expected as well as the September quarter’s revised 1.9% rise. The 12-month inflation rate rose from 6.1% to 6.9%.

Domestic Treasury bond yields moved higher on the day despite moderate falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had gained 9bps to 3.15%, the 10-year yield had added 4bps to 3.51% while the 20-year yield finished 2bps higher at 3.89%.

In the cash futures market, expectations regarding future rate rises firmed. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.07% to average 3.24% in February and then increase to an average of 3.625% in May. August contracts implied a 3.74% average cash while November contracts implied 3.72%.

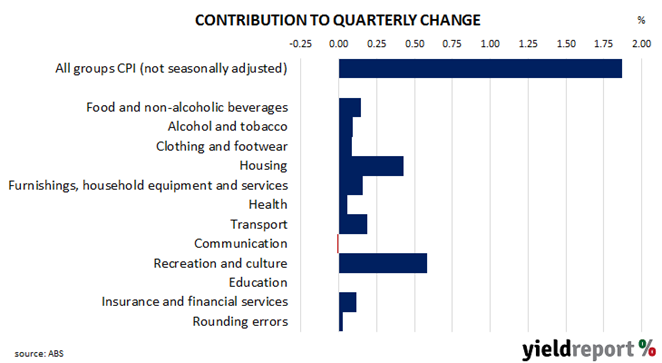

The main driver of the headline inflation figure in the quarter was a 5.4% rise in recreation/culture costs, contributing just under 0.60 percentage points of the 1.87% (unadjusted) increase. Housing costs also had a significant influence on the quarter, rising by 1.9% and contributing slightly under 0.45% percentage points to the quarterly total.

Here’s what a few economists thought about the figures:

Catherine Birch, ANZ

Australia’s CPI data showed momentum continued to build in domestically-driven inflation pressures in Q4. This cements a 25bps cash rate hike in February and supports our view of another 25bps hike in March, especially if we see a solid print for Q4 wages in mid-February as expected.

Non-tradables and services inflation accelerated, both annualising around 8.5%. These measures better reflect underlying and domestically driven inflationary pressures and are more relevant for the RBA’s policy settings than the headline measure.

George Tharenou, UBS

Overall, Q4 inflation was above UBS and consensus [expectations] for both headline and trimmed-mean and the December monthly indicator was extremely strong, indicating the underlying momentum of inflation is still

picking up. At face value this is hawkish. However, with the Q1-2022 headline print of 2.1% dropping

out ahead, inflation has likely now peaked. Indeed, the Q4-2022 outcome of 7.8% was still below the

RBA’s forecast of 8.0%. Furthermore, the outlook for inflation is also still likely lower than the RBA’s

already hawkish forecasts.

Today’s CPI raises the risk the RBA is not as dovish as we expect. Hence, the risk around our view on rates remains to the upside; i.e. another 25bps in March; or if the minimum wage decision in June 2023 is linked (again) to CPI. This could eventually force the RBA to hike in mid-2023, despite a sharp slowing in GDP seeing a rising unemployment rate.

Justin Smirk, Westpac

The large upsize surprise in the December quarter, compared to our 1.5% forecast, was the 5.4% rise in recreation on the back of a 10.9% increase in holiday travel and accommodation costs. Housing was slightly stronger than expected with slightly stronger gains in dwelling prices and utilities. However, it only contributed 0.06 percentage points to our 0.5 percentage point error confirming that housing is no longer the inflationary story but pressures are shifting more towards services and, in particular, tourism and hospitality services.