Last week’s decision by Credit Suisse to write off its AT1 bonds came as a surprise. The Swiss regulator, FINMA, effectively ordered Credit Suisse to trigger the write-off clause of the securities as Switzerland’s second-largest bank found itself in financial difficulty. That in itself was not the surprising part; the surprising part was this was ordered just as the Swiss Government organised a deal for UBS to purchase the Credit Suisse’s CET1 equity for CHF3 billion (AUD$3.9 billion).

AT1 securities are meant to rank ahead of CET1 holders in the event of a company’s liquidation. (In the old days, CET1 securities would have been referred to as ordinary shares while AT1 securities would have been referred to as preference shares, converting preference shares or convertible notes.) And yet, under the Swiss arrangement, ordinary shareholders are set to receive CHF3 billion while holders of Credit Suisse AT1 securities have been advised their holdings are now literally worthless.

The implications of investors losing all their funds invested in assets which rank above ordinary equity before equity holders were totally wiped out led to a broad sell-off in Australian AT1 securities listed on the ASX. AT1 holders had thought their assets ranked higher than shares but lower than ordinary debt. That was not so clear anymore after FINMA’s actions.

However, the Swiss decision may be an anomaly.

The European Central Bank put out a statement on Monday night (AEDT) regarding the Credit Suisse situation. While the ECB welcomed “the comprehensive set of actions taken yesterday by the Swiss authorities”, it also stated “common equity instruments are the first ones to absorb losses, and only after their full use (YR italics) would Additional Tier 1 be required to be written down.”

A couple of days later, the Monetary Authority of Singapore stated “in exercising its powers to resolve a financial institution, it intends to abide by the hierarchy of claims in liquidation. This means that equity holders will absorb losses before holders of Additional Tier 1 (AT1) and Tier 2 capital instruments.”

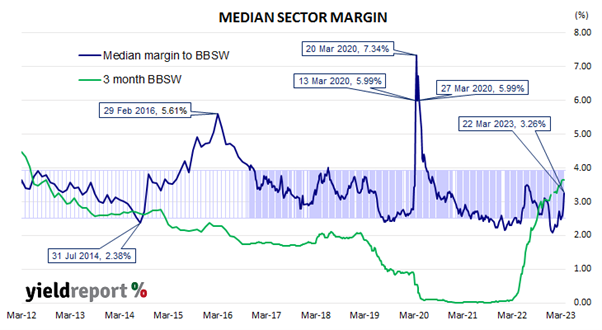

The median margin to BBSW of ASX-listed AT1 securities jumped about 45bps on Monday as prices fell. It then remained fairly stable over Tuesday and Wednesday.

When Banco Popular Espanol experienced difficulties in 2017, Spain’s banking authorities forced a sale to Banco Santander for a total of €1. In that case, all but secured bondholders were wiped out. Read more about what happens when your European bank goes bust here.