Summary: RBA raises GDP forecasts; underlying inflation forecasts raised; jobless rise deferred until next year; headline inflation forecasts raised; Westpac: bar to further hikes clearly lower now.

The Statement on Monetary Policy (SoMP) is released each quarter and it is closely watched for updates to the RBA’s own forecasts.

In August’s SoMP, the opening sentence of the “Outlook” section essentially restated what had been said in the previous two SoMPs. “Global growth is forecast to remain well below its historical average over the next two years, as the lagged effects of monetary policy tightening continue to weigh on demand.”

As far as Australia was concerned, “Growth in economic activity…is forecast to remain subdued over the rest of the year as cost-of-living pressures and the rise in interest rates continue to weigh on domestic demand.”

November’s Outlook opened with a statement which is very similar to August’s Outlook. “Global growth is forecast to slow and remain well below its historical average in the year ahead. This reflects the ongoing effects of tighter monetary policy on demand in advanced economies, as well as a soft outlook for the Chinese economy.”

On domestic matters, it stated, “Growth in the Australian economy is expected to remain below trend over 2023 and 2024…But the economy has proved to be more resilient in recent quarters than previously expected, which is supporting demand conditions for Australian businesses.”

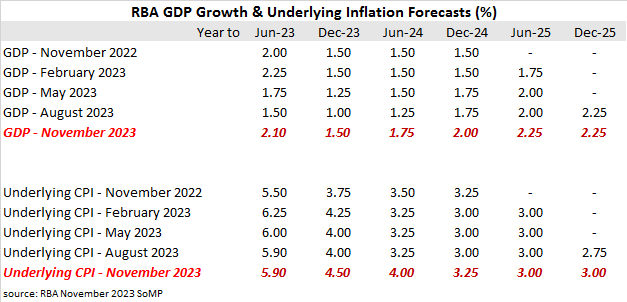

Accordingly, the RBA’s GDP growth forecasts have been raised by 0.50 percentage points for the periods out to June 2024 and by 0.25 percentage points for later periods.

“The outlook for growth in the near-term has been revised up compared with three months ago; stronger-than-expected growth in private and public investment and further upgrades to services exports have more than offset a weaker outlook for household consumption.”

The RBA’s underlying inflation forecasts have also been raised. The RBA’s target band for underlying inflation is 2%-3%, so underlying inflation is now not expected by the RBA to be back to the top of this target range until 2025.

“Consumer price inflation is forecast to continue to decline across the forecast period. However, the expected decline will be more gradual than anticipated at the time of the August forecasts because domestic inflationary pressures are dissipating more slowly than previously thought.”

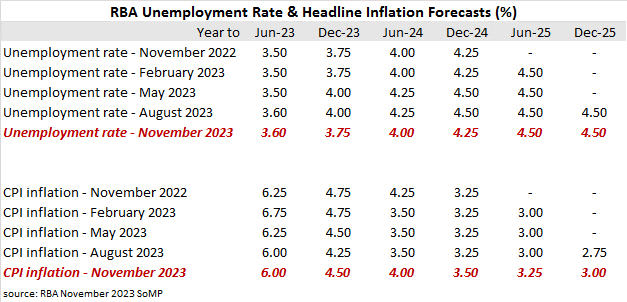

The RBA’s view of the unemployment rate typically follows from its forecasts of GDP growth. The unemployment rate has been fluctuating between 3.50% and 3.70% in the first nine months of 2023 but the RBA now expects it to rise to 4.00% by June 2024, six months later than expected in August. Forecasts from August have all been essentially deferred by six months.

“Employment growth is expected to remain positive throughout the forecast period, but it is expected to be below growth in the working-age population for a time, resulting in a gradual increase in the unemployment rate. Because of the more resilient outlook for economic activity, the unemployment rate is now forecast to rise more gradually than at the August Statement, to be around 4.25% from late 2024 to 2025.”

Headline inflation forecasts have been raised by 0.25 percentage points for all periods with the exception of the year to June 2024 where the forecast has been raised by 0.50 percentage points.

“Goods prices have accounted for almost all of the decline in inflation so far; goods inflation is expected to continue falling in the near term as the resolution of supply disruptions flows through to prices paid by consumers. By contrast, services inflation remains high. Services inflation is expected to ease but to remain above its inflation-targeting average throughout the forecast period in an environment of elevated domestic cost pressures and still-robust levels of demand.”

Commonwealth Government bond yields rose noticeably on the day, following large increases of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had gained 8bps to 4.25% while 10-year and 20-year yields both finished 9bps higher at 4.63% and 4.95% respectively.

In the cash futures market, expectations regarding further rate rises firmed. At the end of the day, contracts implied the cash rate would increase from the current rate of 4.32% and average 4.335% through December and 4.395% in February. May 2024 contracts implied a 4.46% average cash rate while August 2024 contracts implied 4.44%, 12bps more than the current rate.

“Risks to the inflation forecast are also skewed to the upside,” said Westpac Chief Economist Luci Ellis. “If things turn out in line with the RBA’s revised forecasts, they might not need to raise rates again. But the bar to further hikes is clearly lower now; the RBA has almost no margin for further upside surprises.”