Summary:

The hybrid securities market remains a dynamic space for income-seeking investors, with issuer-specific trends offering valuable clues about risk appetite, pricing behavior, and regulatory impact.

Among bank-issued hybrids, Judo Capital continues to command attention with its high running yield of 9.52%, supported by strong demand and premium pricing. Its relatively short call horizon and elevated issue margin reflect both investor confidence and the need for yield in a low-volatility environment.

Latitude’s LFSPA, while offering a similarly high yield of 9.19%, trades at a discount and carries a substantial 12.12% trading margin—a signal that investors are pricing in higher risk or uncertainty around its credit profile. This divergence from major bank hybrids highlights the market’s nuanced view of issuer strength and structure.

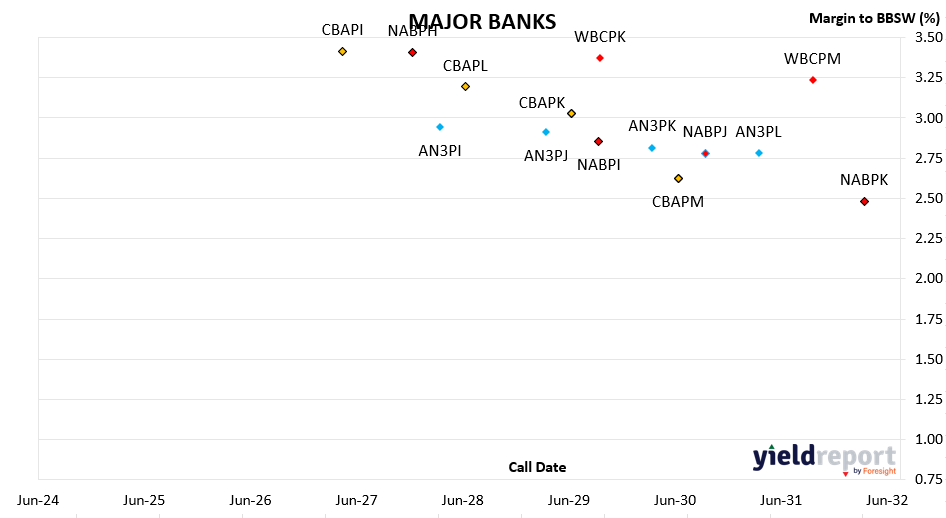

The big four banks—CBA, ANZ, NAB, and Westpac—continue to anchor the hybrid landscape with consistent yields around 6.4% to 7.3%, depending on call dates and franking benefits. These instruments are favored for their stability and liquidity, though recent data shows slight yield compression as longer-dated hybrids dominate new issuance.

Westpac’s WBCPH, with a trading margin nearing 30%, stands out due to its imminent call date in September 2025. This uplift reflects the typical yield spike seen as hybrids approach maturity, offering tactical opportunities for short-term investors.

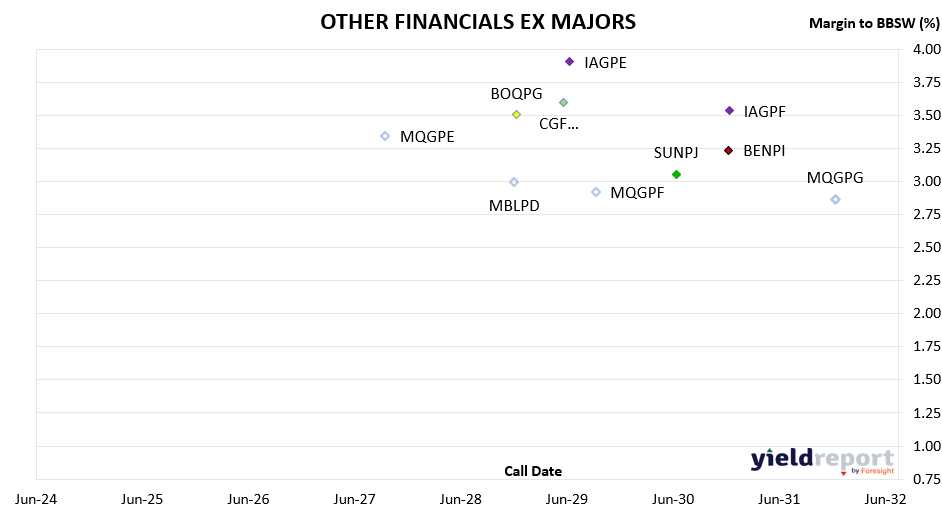

Outside the banking sector, corporate hybrids are gaining traction. Nufarm’s NFNG and Ramsay Health Care’s RHCPA, both perpetual instruments, offer running yields of 9.05% and 8.37% respectively. These securities appeal to investors seeking diversification, though their perpetual nature and structural complexity require careful consideration.

Looking ahead, APRA’s decision to phase out bank hybrids by 2032 is reshaping issuer behavior. Banks are expected to pivot toward Tier 2 capital instruments, such as subordinated debt, which offer lower yields but rank higher in the capital structure. This shift will gradually reduce the supply of traditional hybrids, prompting investors to reassess their income strategies.

For now, the hybrid market remains a fertile ground for yield, with issuer-specific analysis offering critical insights into pricing, risk, and opportunity. YieldReport will continue to track these developments, helping investors navigate the evolving landscape with clarity and confidence.

ASX-Listed Hybrids

COMPANY CODE HYBRID TYPE MATURITY/

CALL

DATEMARGIN

INCL. CREDITSTRADING

MARGINDAY

CHANGEDAY

CLOSERUNNING

YIELD**Westpac WBCPH Capital Notes 5 22/09/2025 3.20% 29.87% 1.62% 99.97 7.24% AMP Group AMPPB Capital Notes 2 16/12/2025 4.50% 8.84% 0.25% 101 8.36% Macquarie Bank MBLPC Capital Notes 2 22/12/2025 4.70% 8.13% 0.21% 101.049 8.54% Challenger CGFPC Capital Notes 3 25/05/2026 4.60% 6.03% 0.10% 102.47 8.41% Nat Aust Bank NABPF Capital Notes 3 17/06/2026 4.00% 4.85% 0.08% 102.099 7.77% Suncorp SUNPH Capital Notes 3 17/06/2026 3.00% 4.87% 0.08% 100.88 6.83% Macquarie Group MQGPD Capital Notes 4 10/09/2026 4.15% 4.30% 0.06% 102.5 7.87% CBA CBAPJ PERLS 13 20/10/2026 2.75% 3.94% 0.06% 101.05 6.56% Latitude LFSPA Capital Notes 27/10/2026 4.75% 12.12% 0.12% 96.5 9.19% Westpac WBCPJ Capital Notes 7 22/03/2027 3.40% 5.06% 0.05% 102.197 7.29% CBA CBAPI PERLS 12 20/04/2027 3.00% 3.41% 0.04% 101.91 6.76% Bank of Queensland BOQPF Capital Notes 2 14/05/2027 3.80% 4.57% 0.05% 102.58 7.60% Bendigo Bank BENPH Capital Notes 15/06/2027 3.80% 4.04% 0.04% 102.5 7.54% Macquarie Group MQGPE Capital Notes 5 20/09/2027 2.90% 3.35% 0.03% 101.39 6.67% Nat Aust Bank NABPH Capital Notes 5 17/12/2027 3.50% 3.41% 0.03% 103 7.19% ANZ Bank AN3PI Capital Notes 6 20/03/2028 3.00% 2.95% 0.02% 102.16 6.70% CBA CBAPL PERLS 15 15/06/2028 2.85% 3.19% 0.02% 101.76 6.61% Suncorp SUNPI Capital Notes 4 17/06/2028 2.90% 3.55% 0.03% 101.05 6.71% Westpac WBCPL Capital Notes 9 22/09/2028 3.40% 3.83% 0.03% 103.68 7.18% Macquarie Bank MBLPD Capital Notes 3 7/12/2028 2.90% 2.99% 0.02% 102.2 6.62% Bank of Queensland BOQPG Capital Notes 3 15/12/2028 3.40% 3.50% 0.02% 102.601 7.12% Judo Capital JDOPA Capital Notes 16/02/2029 6.50% 4.06% 0.03% 112 9.52% ANZ Bank AN3PJ Capital Notes 7 20/03/2029 2.70% 2.91% 0.01% 101.39 6.45% Challenger CGFPD Capital Notes 4 25/05/2029 3.60% 3.59% 0.02% 103.5 7.29% CBA CBAPK PERLS 14 15/06/2029 2.75% 3.03% 0.02% 101.77 6.51% IAG IAGPE Capital Notes 2 15/06/2029 3.50% 3.91% 0.02% 103 7.29% Macquarie Group MQGPF Capital Notes 6 12/09/2029 3.70% 2.92% 0.02% 105.3 7.21% Nat Aust Bank NABPI Capital Notes 6 17/09/2029 3.15% 2.86% 0.02% 103.77 6.78% Westpac WBCPK Capital Notes 8 21/09/2029 2.90% 3.37% 0.02% 103.04 6.70% ANZ Bank AN3PK Capital Notes 8 20/03/2030 2.75% 2.82% 0.01% 101.86 6.47% CBA CBAPM PERLS 16 17/06/2030 3.00% 2.63% 0.02% 104.19 6.61% Suncorp SUNPJ Capital Notes 5 17/06/2030 2.80% 3.05% 0.02% 101.76 6.56% Nat Aust Bank NABPJ Capital Notes 7 17/09/2030 2.80% 2.78% 0.01% 102.801 6.49% Bendigo Bank BENPi Capital Notes 2 13/12/2030 3.20% 3.24% 0.02% 102.85 6.90% Insurance Australia IAGPF Capital Notes 3 15/12/2030 3.20% 3.53% 0.01% 102.7 6.98% ANZ Bank AN3PL Capital Notes 9 20/03/2031 2.90% 2.78% 0.01% 102.69 6.56% Westpac WBCPM Capital Notes 10 22/09/2031 3.10% 3.23% 0.01% 104.21 6.83% Macquarie Group MQGPG Capital Notes 7 15/12/2031 2.65% 2.86% 0.01% 101.5 6.41% Nat Aust Bank NABPK Capital Notes 8 17/03/2032 2.60% 2.48% 0.01% 103.26 6.26% ASX-Listed Hybrids (Non-standard)

COMPANY CODE BOND TYPE CALL DATE ISSUE MARGIN (inc frank) TRADING MARGIN DAY CLOSING PRICE RUNNING YIELD Nufarm NFNG Step Up Perpetual 3.90% 5.33% -0.01% 87.2 9.05% Ramsay Health Care RHCPA Preference Share Perpetual 4.85% 4.64% 0.00% 105.6 8.37%