| Close | Previous Close | Change | |

|---|---|---|---|

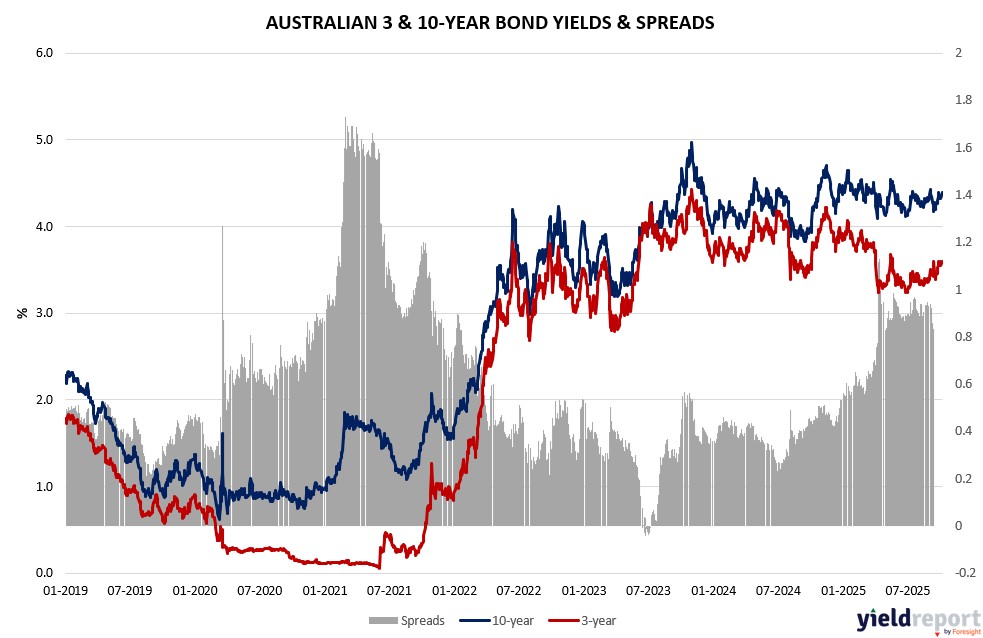

| Australian 3-year bond (%) | 3.565 | 3.582 | -0.017 |

| Australian 10-year bond (%) | 4.366 | 4.396 | -0.03 |

| Australian 30-year bond (%) | 5.035 | 5.069 | -0.034 |

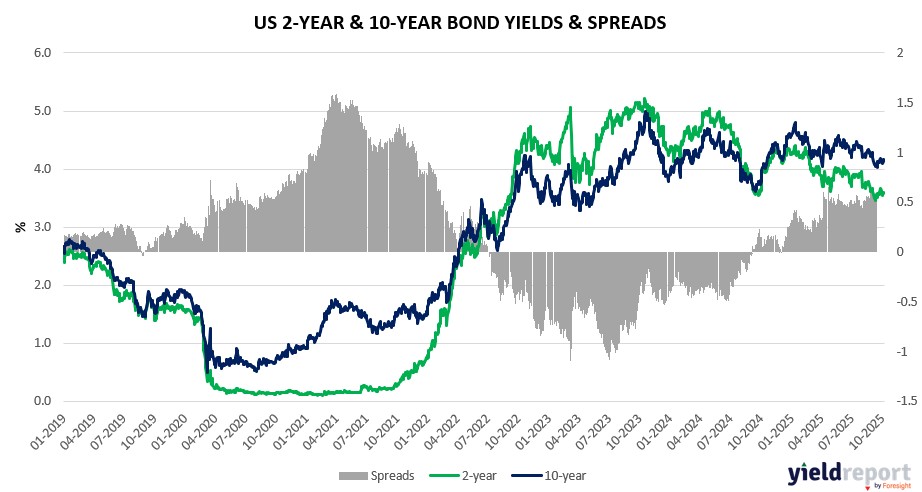

| United States 2-year bond (%) | 3.566 | 3.599 | -0.033 |

| United States 10-year bond (%) | 4.109 | 4.17 | -0.061 |

| United States 30-year bond (%) | 4.7065 | 4.7664 | -0.0599 |

Overview of the Australian Bond Market

Australian government bond yields fell on October 8, 2025, as global haven flows amid US shutdown politics and soft data supported prices, with the 10-year down six basis points to 4.32%, the 2-year off three to 3.48%, and the 15-year declining seven to 4.65%. The 5-year eased five basis points to 3.73%, flattening the curve slightly as markets price steady RBA policy.

Trump’s threats of mass firings and blue-state funding cuts, plus tariff extensions with China, could spill into commodity volatility affecting Aussie exports, though Fed minutes’ AI labor notes add growth uncertainty. Domestically, weakening sentiment and ads data dim cut prospects ahead of Friday’s tentative US payrolls, now reported at 22,000 for September versus 50,000 poll, potentially swaying sentiment.

Pepperstone’s Chris Weston sees salvation in US earnings for higher pushes, while UBS maintains bull views on earnings and AI tailwinds despite valuations. Positioning trims suggest caution, with Goldman urging diversification amid narrow rallies.

Futures data indicates reduced longs, aligning with prudent stances on high US valuations impacting Aussie flows. Dealers anticipate unchanged issuance, but global events like Powell’s speech could reprice if signaling dovish shifts.

Overview of the US Bond Market

Treasury yields were mixed on October 8, 2025, with the 10-year little changed at 4.13% after a $39 billion sale saw slightly soft demand, as investors weighed Fed minutes signaling further easing but inflation caution against shutdown fiscal risks. The 2-year yield rose two basis points to 3.58%, while the 30-year held at 4.72%. Shorter bills edged higher, with the 3-month at 3.84%, reflecting bets on data-dependent policy amid tariff talks noted in minutes as a potential price driver.

President Trump’s selective back pay threats for furloughed workers, amid OMB memos challenging 2019 law guarantees, heighten shutdown stakes that could disrupt issuance and boost borrowing costs. Economic data like weak September payrolls at 22,000 and August trade gap at -$78.3 billion underscore slowdown risks, potentially supporting lower rates, though AI’s labor impacts flagged by Fed add nuance. Initial claims fell to 218,000 for the week ended September 27 versus 223,000 expected, easing some labor fears.

Wells Fargo’s Luis Alvarado sees no preset Fed path, expecting two more quarter-point cuts this year and two in 2026, while LPL’s Roach highlights tariff focus in minutes. Nationwide’s Mark Hackett notes market calm despite risks, with no 1% S&P moves since August. JPMorgan’s Treasury survey showed shrinking net longs ahead of the meeting, per CFTC data asset managers trimmed positions across tenors by $23.5 million per basis point, concentrated in 5-year and bonds, as leveraged funds pared shorts.

Dealers expect steady coupon sizes for November-January, though shutdown delays may alter plans, with Friday’s sentiment data potentially influencing if it signals consumer strain from expiring ACA subsidies.