BOND_09.10.25.csv

| Close | Previous Close | Change | |

|---|---|---|---|

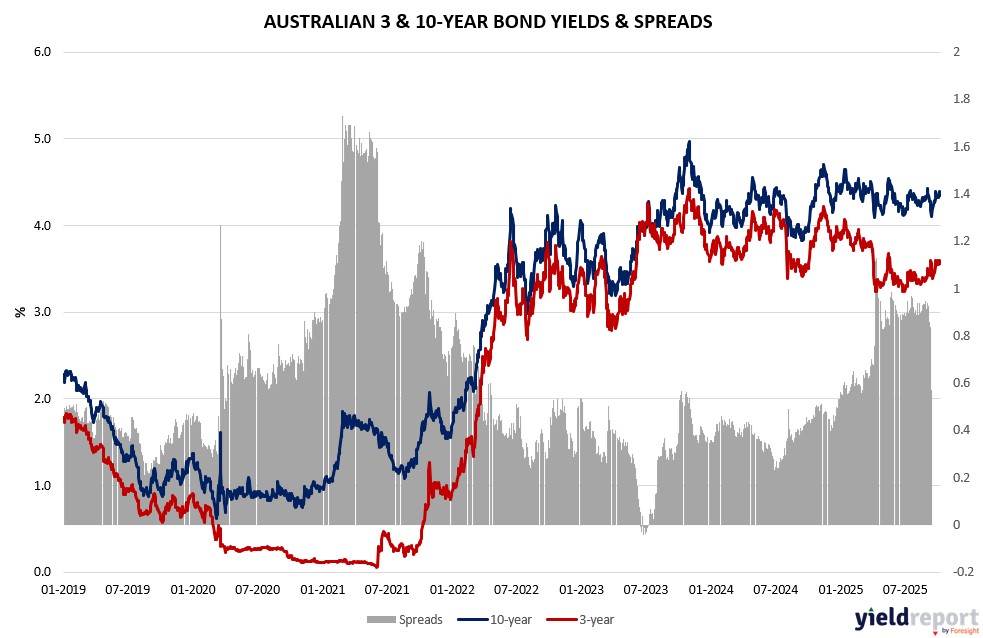

| Australian 3-year bond (%) | 3.566 | 3.565 | 0.001 |

| Australian 10-year bond (%) | 4.35 | 4.366 | -0.016 |

| Australian 30-year bond (%) | 5.002 | 5.035 | -0.033 |

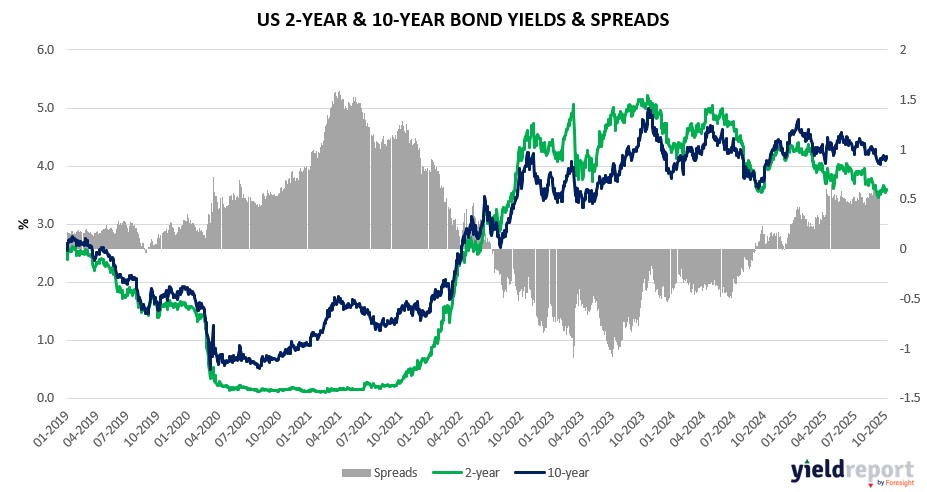

| United States 2-year bond (%) | 3.591 | 3.566 | 0.025 |

| United States 10-year bond (%) | 4.131 | 4.109 | 0.022 |

| United States 30-year bond (%) | 4.7182 | 4.7065 | 0.0117 |

Overview of the Australian Bond Market

Australian government bond yields mixed modestly on October 9, 2025, with the 10-year flat at 4.35%, as hotter 4.8% inflation expectations reinforced RBA hold amid global shutdown data voids. The 2-year rose two basis points to 3.52%, 15-year down one to 4.69%, 5-year up one to 3.76%, signaling curve stability.

Trump’s domestic military shifts, like Memphis task force and Portland federalization amid court blocks, could indirectly volatility commodities impacting Aussie exports, while Nobel pressures add geopolitical noise. Local inflation tick pressures rates higher-for-longer, ahead of Friday’s US payrolls forecast at 50,000 with 4.3% unemployment, potentially influencing cross flows.

Capital.com’s Rodda flags real economy lag versus AI, HSBC et al. maintain bull on earnings, AI despite stretches. Goldman urges diversification on narrow rallies.

Positioning data suggests trimmed longs per CFTC, prudent amid valuations. Dealers expect unchanged issuance, but Powell’s speech could reprice dovish odds.

Overview of the US Bond Market

Treasury yields climbed on October 9, 2025, with the 10-year up three basis points to 4.14% as dollar strength and oil declines reflected cooling geopolitics, amid shutdown data delays heightening earnings focus. The 2-year rose two basis points to 3.60%, and the 30-year advanced two to 4.73%. Shorter bills ticked higher, 3-month at 3.86%, as markets price Fed caution.

President Trump’s military deployments, including federalizing Guard troops in Portland and Chicago despite lawsuits citing Posse Comitatus violations, add fiscal uncertainty, potentially inflating borrowing amid Norway tensions over Nobel pressures. Economic prints like August trade deficit at -$78.3 billion wider than -$61 billion expected pressure growth, while factory orders miss fuels slowdown bets ahead of Friday’s payrolls at 50,000 forecast versus prior 22,000 actual, possibly swaying two more cuts this year per views.

Nuveen’s Saira Malik sees Q4 strength favoring rally continuation. City Index’s Razaqzada notes shallow retracements supporting dips, but pullback possible. JPMorgan data shows speculative futures near medians, not extended. CFTC reports asset managers trimmed longs by $23.5 million per basis point in 5-year and bonds, leveraged pared shorts.

Dealers anticipate steady auctions November-January, though shutdowns risk disruptions, with sentiment data potentially highlighting consumer tariff impacts.