| Name | Daily Close | Daily Change | Daily Change (%) |

|---|---|---|---|

| Dow | 45,544.88 | -92.02 | -0.20% |

| S&P 500 | 6,460.26 | -41.6 | -0.64% |

| Nasdaq | 21,455.55 | -249.61 | -1.15% |

| VIX | 15.36 | 0.93 | 6.44% |

| Gold | 3,545.60 | 29.5 | 0.84% |

| Oil | 64.33 | 0.32 | 0.50% |

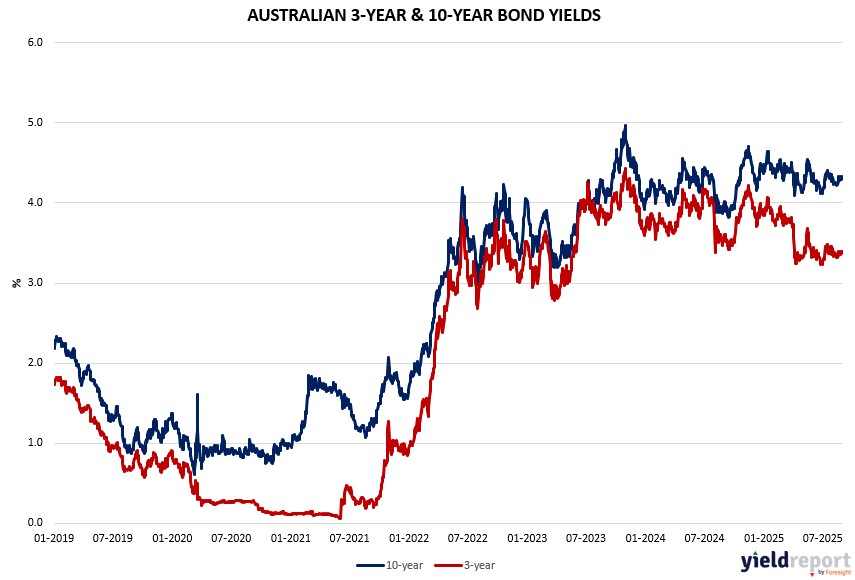

Overview of the Australian Bond Market

Australian government bonds sold off on September 1, 2025, with yields climbing as gold’s surge and global policy noise overshadowed soft data, kicking off September after August’s declines. The 10-year yield rose 7 basis points to 4.34%, the 2-year added 3 bps to 3.36%, the 5-year gained 5 bps to 3.69%, and the 15-year climbed 8 bps to 4.72%. In August, yields rose modestly—three-year up 16 bps to ~3.42%, 10-year higher amid fiscal concerns—reflecting RBA caution post-July CPI surprise, though real yields fell with global peers.

Trump’s inflation post, amid Fed pressure including Cook’s ouster attempt, risks politicized policy and higher long-term inflation, blending with tariff truce talks (90-day extension eyed) to unsettle global flows. Locally, July building approvals -8.2% (vs. -4% poll) signals construction weakness, but August PMI at 53 affirms manufacturing growth, tempering RBA cut bets. Bond moves track US resilience—PCE in-line at core YY 2.9%—bolstering higher-for-longer views, yet independence erosion could demand higher premiums, spilling to Aussie yields via commodity ties as gold hits $US3,552.

Upcoming Q2 current account (-16B expected) and net exports (0% contribution) may influence RBA, with swaps at ~60% September Fed cut chance. Asset positioning likely cautious per CFTC, eyeing diversified havens amid US debt and tariff bites.

Overview of the US Bond Market

U.S. markets were closed for Labor Day, with attention turning to Friday’s nonfarm payrolls report, a key factor for the Federal Reserve’s expected rate cut later this month. Additional labor data this week include the JOLTS survey, ADP payrolls, and speeches from Fed officials, including Lisa Cook, who is contesting her dismissal by President Trump. Trade policy remains a risk after an appeals court ruled most of Trump’s tariffs illegal.

In currency and crypto markets, the dollar fell to a five-week low on thin liquidity and caution ahead of jobs data, while bitcoin slid to a two-month low near $107,000. Gold futures hit fresh records above $3,550/oz, supported by safe-haven demand and expectations of monetary easing. Oil prices stayed range-bound, with Brent near $68 and WTI at $64.

European fixed income markets face diverging dynamics, with corporate bonds drawing stronger investor preference over sovereign debt. Edmond de Rothschild Asset Management noted corporate bond volatility has been just one-third that of government bonds this year, as political uncertainty and fiscal concerns keep sovereign yields unstable.

This is particularly evident in the U.K., where 10-year gilt yields remain the highest among G-10 nations at 4.74%, driven by persistent inflation and concerns over rising debt. Retail sales data later this week may provide further clues on consumer weakness.

In the eurozone, government bond supply is set to increase in September to €122 billion, the highest since May, with France, Germany, and Spain facing the largest net financing requirements. France remains a focal point for investors as fiscal consolidation efforts falter, pushing OAT yields higher and widening spreads with Bunds. JPMorgan highlighted that without reforms, markets act as a disciplinary force.

Nonetheless, Commerzbank suggested buying German Bunds when yields rise above 2.72%, while Goldman Sachs argued French risks are already priced in, with limited spillovers expected to Bunds or other sovereign spreads. Meanwhile, in the U.S., Goldman noted risk premia are building at the long end of Treasurys, steepening the yield curve despite front-end stability.