| Close | Previous Close | Change | |

|---|---|---|---|

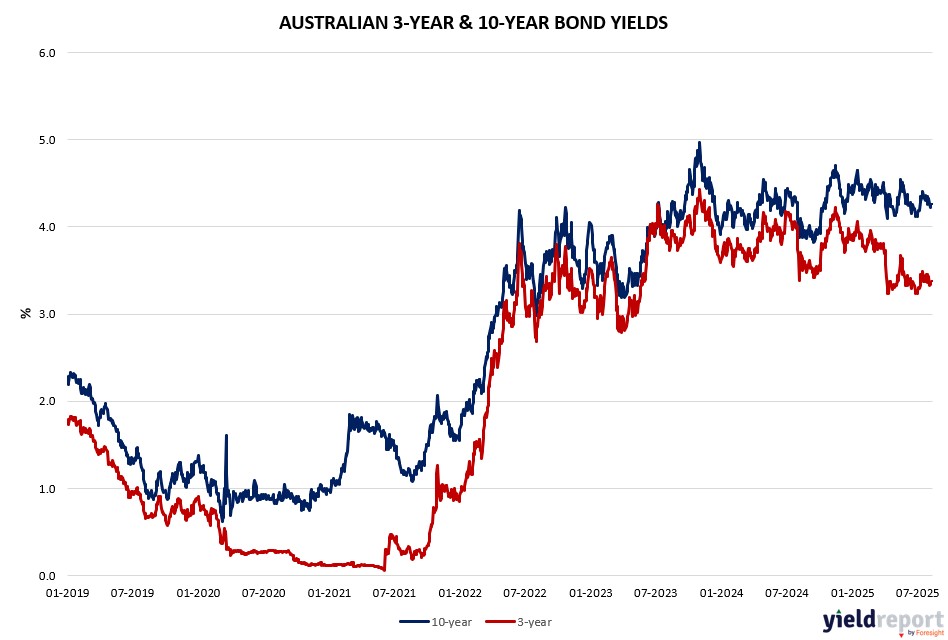

| Australian 3-year bond (%) | 3.358 | 3.372 | -0.014 |

| Australian 10-year bond (%) | 4.247 | 4.253 | -0.006 |

| Australian 30-year bond (%) | 4.955 | 4.965 | -0.01 |

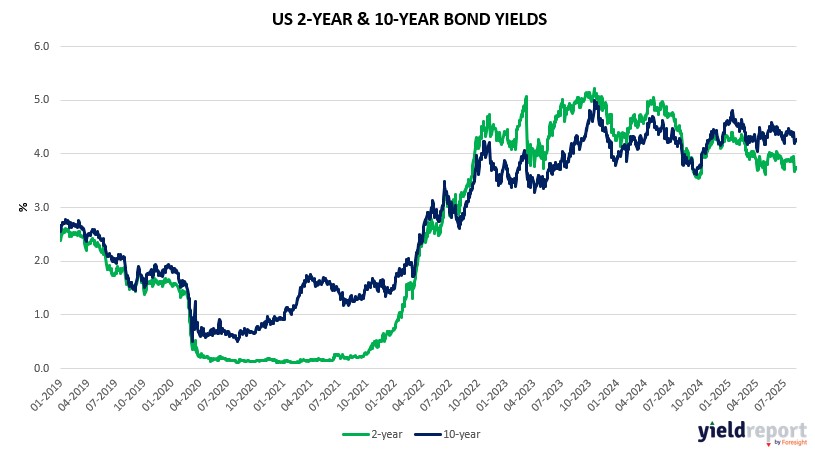

| United States 2-year bond (%) | 3.77 | 3.75 | 0.02 |

| United States 10-year bond (%) | 4.277 | 4.266 | 0.011 |

| United States 30-year bond (%) | 4.8454 | 4.8353 | 0.0101 |

Overview of the Australian Bond Market

Australian government bond yields showed a mixed response on August 12, 2025, following the RBA’s rate cut, with shorter maturities rallying on dovish signals while longer ends edged higher amid persistent inflation concerns. The 2-year yield fell 2 basis points to 3.32%, the 5-year dropped 2 basis points to 3.62%, the 10-year rose 1 basis point to 4.25%, and the 15-year increased 1 basis point to 4.61%. Over the past month, yields have trended lower (10-year down 7 basis points), reflecting building expectations for easing despite recent CPI stability.

The cut to 3.60%—the third this year—spurred immediate equity highs and a brief AUD dip to 0.6498 (-0.23%), but Bullock’s comments on uncertainty and potential for more reductions (forecasts imply “a couple” additional) tempered aggressive positioning. June’s robust trade data and July’s expanding services PMI at 54.1 highlight economic resilience, potentially capping further short-end declines, while global macro factors like US-China tariff truce extension talks (with a 90-day option floated) add layers of caution.

Bond traders are monitoring US developments, where inline CPI (core 3.1% yearly, slightly above poll) supports a 60% chance of a 25 basis-point Fed cut in September from the current 4.25%-4.5% range, though trade war durability and recent EU/Japan deals could keep rates higher longer, pressuring prices. Locally, steady demand for fixed-rate bonds persists amid equity rotations into banks and resources, but upcoming August 13 Wage Price Index (poll 3.3% yearly) could sway views if it underscores cooling labor costs.

In positioning, net long bets likely increased post-cut, per implied surveys, with swaps pricing in about half a point of further RBA easing by year-end. Asset managers may have added to shorter tenors, while leveraged funds trim longs in longer bonds. Dealers anticipate unchanged auction sizes for August-October, aligning with prior guidance, though tariff risks and soft-landing optimism may sustain elevated longer yields as diversification hedges against volatility.

Overview of the US Bond Market

While an initial rally in Treasuries faded, money markets priced in an about 90% chance of a Fed reduction next month. Two-year yields, more sensitive to imminent policy moves, slid four basis points to 3.73%.

Short-term Treasuries rallied following a mostly benign report on US inflation that prompted traders to boost expectations the Federal Reserve will cut interest rates next month.

The rally pushed yields on two-year notes which are more sensitive to changes in monetary policy, down by four basis points Tuesday afternoon to 3.73%. And swap traders priced in nearly 90% odds of a Fed rate cut on Sept. 17, up from about 80% before the data.

Underlying US inflation accelerated to the strongest since the start of the year, but a tepid rise in goods prices tempered concerns about tariff-driven pressures.

The core consumer price index, which excludes the often volatile food and energy categories, increased 0.3% from June, the strongest pace since the start of the year. That was in line with economists’ forecasts, as was the overall CPI on a monthly basis.

One of the key drivers of inflation in recent years has been housing costs, the largest category within services. Shelter prices rose 0.2% for a second month, reflecting steady housing costs and a continued decline in prices of hotel stays.

With risks to the labor market rising, the Fed would likely tolerate temporarily higher-than-expected inflation prints, provided that the risk of second-round effects remains contained and price expectations stay well-anchored.

US officials have kept rates unchanged this year in hopes of gaining clarity on whether tariffs will lead to sustained inflation. At the same time, the labor market, the other half of their dual policy mandate, is showing signs of losing momentum.

In a social media post, President Donald Trump resumed his criticism of Jerome Powell over the central bank’s decision to hold rates steady. Trump also said he is weighing a lawsuit against the Fed chief over the renovation of the central bank’s headquarters – a project whose cost overruns have drawn scrutiny.