| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.474 | 3.519 | -0.045 |

| Australian 10-year bond (%) | 4.259 | 4.293 | -0.034 |

| Australian 30-year bond (%) | 4.933 | 4.966 | -0.033 |

| United States 2-year bond (%) | 3.47 | 3.522 | -0.052 |

| United States 10-year bond (%) | 4.001 | 4.051 | -0.05 |

| United States 30-year bond (%) | 4.592 | 4.634 | -0.042 |

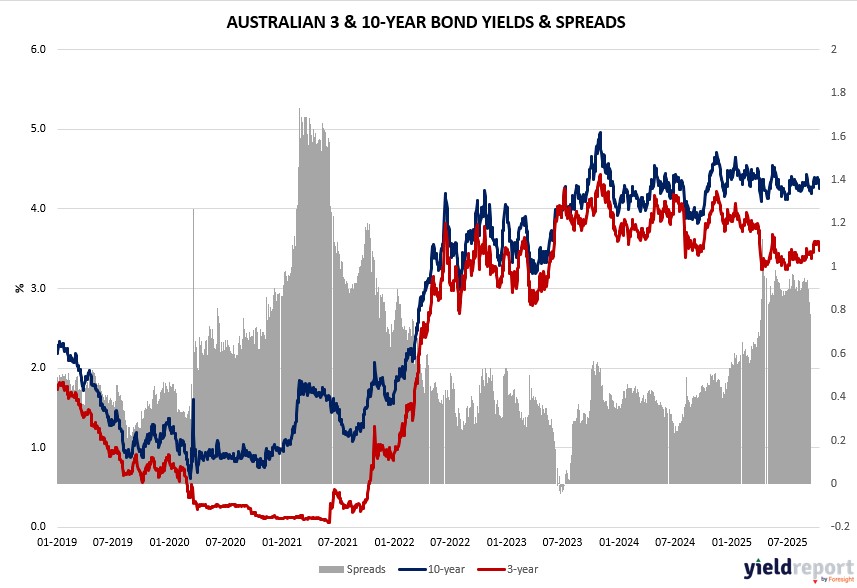

Overview of the Australian Bond Market

Australian government bond yields eased on October 14, 2025, with the 10-year down four basis points to 4.24% and the two-year slipping three to 3.43%, as equity gains in resources tempered risk-off flows from US trade noise. The 15-year fell to 4.58%, tracking global haven demand amid gold’s surge.

NAB’s confidence uptick to +7 underscores business steadiness despite hiring softness, aligning with RBA’s pause and easing cost pressures that favor steady policy. China’s looming CPI (-0.2% forecast) and PPI (-2.3%) Thursday could pressure commodity exporters if deflation persists, while US brinkmanship risks inflation via tariffs—though Trump’s TACO pattern suggests dip-buying opportunities, per Nomura’s Charlie McElligott, who pegs 12% returns from shorting S&P futures on escalations.

The AUD’s drop to 0.6468 reflects caution ahead of Thursday’s employment data (20,000 jobs forecast, 4.3% unemployment), which may test cut bets if labor softens. Strategists see funds rotating from discretionary and tech to resources, with pullbacks as entry points if fundamentals endure, though volatility from AI froth and trade could cap upside.

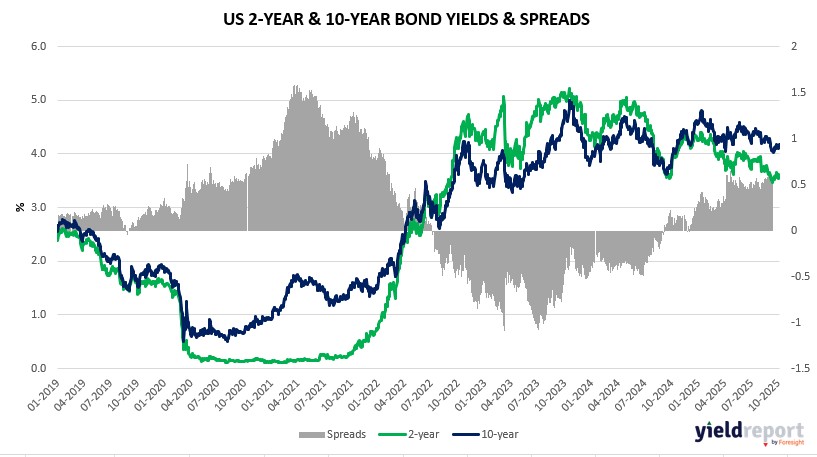

Overview of the US Bond Market

Treasury yields ticked lower on October 14, 2025, with the 10-year dipping one basis point to 4.03% and the two-year falling three to 3.48%, reflecting haven bids amid trade jitters and Powell’s dovish tilt on liquidity measures. The 30-year held steady at 4.63%, as two-year notes hit lows not seen since 2022 on expectations of Fed easing to counter job-market softening.

Powell’s remarks confirmed an October rate cut trajectory, per JPMorgan’s Michael Feroli, while TD Securities anticipates QT’s end at the FOMC meeting, easing term premiums and funding strains—potentially via 2026 bill purchases if year-end pressures mount. Trade Representative Jamieson’s optimism on senior-level US-China discussions, including a potential Trump-Xi meeting, tempered escalation fears, though Trump’s cooking oil threat highlighted farmer aid delays from the shutdown. The Bloomberg Dollar Spot Index eased 0.1%, with the euro up 0.3% to $1.1606, as global funds eye tariff truces’ fading market lift.

JPMorgan’s client survey showed net longs at two-month lows ahead of this week’s data, with asset managers trimming positions across tenors by $23.5 million per basis point in recent CFTC figures, signaling caution on inflation risks from tariffs. Dealers expect unchanged August-October auction sizes per April guidance, with 10- and five-year issuances up $1 billion. Upcoming releases include international trade Tuesday (forecast -61 billion deficit), Philly Fed Thursday (8.5 index), retail sales (0.4% MM), and non-farm payrolls Sunday (50,000 jobs, 4.3% unemployment), which could sway cut odds if consumer resilience holds amid trade whiplash.