| Close | Previous Close | Change | |

|---|---|---|---|

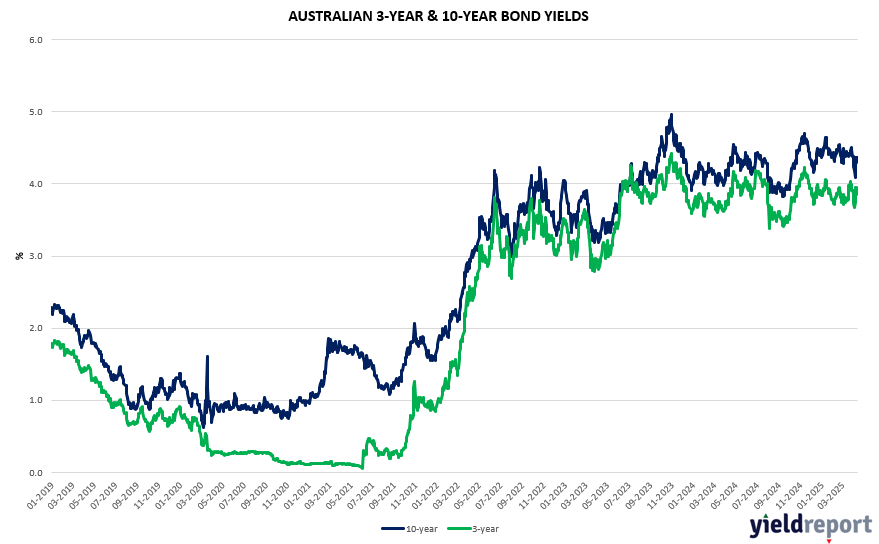

| Australian 3-year bond (%) | 3.356 | 3.288 | 0.068 |

| Australian 10-year bond (%) | 4.36 | 4.367 | -0.007 |

| Australian 30-year bond (%) | 5.073 | 5.111 | -0.038 |

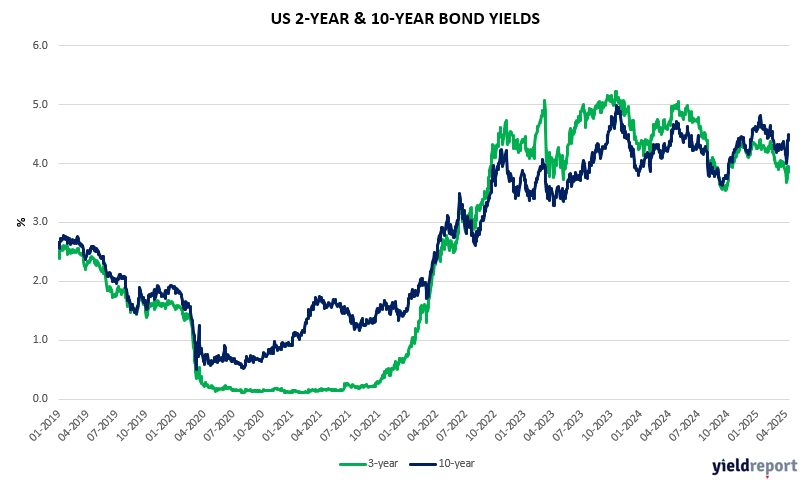

| United States 2-year bond (%) | 3.9265 | 3.954 | -0.028 |

| United States 10-year bond (%) | 4.4659 | 4.493 | -0.027 |

| United States 30-year bond (%) | 4.86 | 4.875 | -0.015 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield declined 10 pbs to 4.38% on Monday. Monday was always going to be an up day given it was comforting words from a Fed official on Friday that led to an up day, and an up day that by the very degree of the up was comforting. Friday was in complete contrast to what happened on Wednesday last week, which was nothing short of a fool’s paradise. Semblance restored? Well, let’s not get ahead of ourselves.

Notwithstanding Friday’s developments, where the Fed stated it will step in if required in relation to what was a creaking bond market, the equities market have two massive issues: 1) China isn’t going to play ball and both leaders have immense pride; 2) yes, the Fed may have reassured markets, but the US Government bond market is nuts currently. Just because the Fed said they may intervene, that doesn’t mean they won’t tolerate a high degree of yield widening before they do. US treasuries have gone from risk-free to not risk-free.

Foreign investors own 33% of US Treasuries, 27% of US corporate bonds and 18% of US stocks. And they are turning away – the USD moves last week were probably the give away. And it’s why volatility indices across bonds and stocks have not retreated. And it’s why the benchmark 10-year US Treasury yield remains stuck near 4.5%, up from 3.99% just 10 days ago. As they say, ‘Houston, we have a problem’.

As we noted in our Weekly note, believe the hype on selling the US. Despite President Trump’s pause on broad tariffs, investors are still looking to shun US assets in favour of Europe and other developed markets, according to the latest MLIV Pulse survey. Of the 203 respondents to a poll conducted April 9-11, after Trump announced a 90-day reprieve on levies for most countries, 81% plan to either keep their exposure to US assets the same or decrease it. More than a quarter of respondents said they’re curbing their investment more than they had anticipated before the president unveiled global tariffs of as much as 50% earlier this month. As per our last Thursday daily headline, from US exceptionalism to sell everything US. What’s the reflex trade – the Deutsche Bund, Swiss Franc, Japanese Yen, and gold.

US BOND MARKETS

The yield on the 10-year US Treasury note declined circa 13 bps to the 4.36% mark on Monday trimming last week’s surge topped at over 4.5% in the prior session as markets continued to assess the future of US trade policy and how it will impact growth and foreign demand for US debt securities. The Presidential administration momentarily waved consumer electronics and computers from the series of aggressive tariffs on China. This allowed from some respite in the Treasuries selloff on signs that President Trump has a pain threshold and will impose constraints on tariffs should financing conditions undergo periods of stress. Still, heightened uncertainty prevails as Trump also warned that future tariffs on electronics and semiconductors are still going to be passed.

What about the Fed put? In corporates, credit spreads have widened significantly this month but they remain far from levels that would compel the Federal Reserve to step in, according to UBS. UBS stated that current indicators suggest no immediate justification for intervention. UBS uses the New York Fed’s Credit Market Distress Index to model how wide the premium to Treasuries that corporate debt would need to reach before the Fed jumped in. It estimates US investment grade spreads would have to move about 200 basis points above Treasuries and high yield bonds 720 basis points over to get the central bank to move. That compares to 113 basis points and 419 basis points, respectively, as of Friday’s close. So, given the inflationary backdrop, unless the market seizes up, unemployment jumps, or spreads really blow up, we believe it is unlikely the Fed will step in.

What’s the flipside to the ratcheting up in corporate high yield spreads? Private debt steps in, and which is not atypical. Non-bank lenders tend not to pull back in bad times. But what we would expect to see is an increase in middle market private credit returns over the next year, assuming credit quality remains robust.