| Close | Previous Close | Change | |

|---|---|---|---|

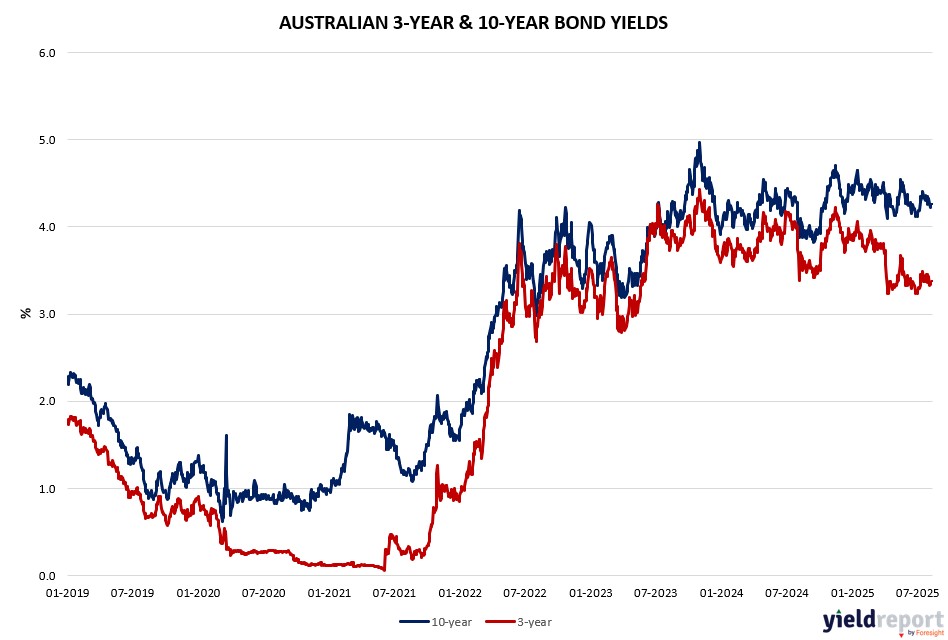

| Australian 3-year bond (%) | 3.322 | 3.339 | -0.017 |

| Australian 10-year bond (%) | 4.215 | 4.234 | -0.019 |

| Australian 30-year bond (%) | 4.951 | 4.946 | 0.005 |

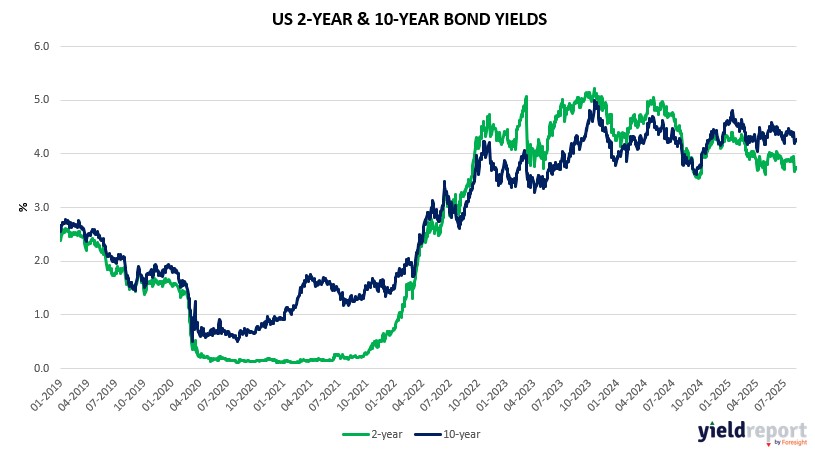

| United States 2-year bond (%) | 3.668 | 3.716 | -0.048 |

| United States 10-year bond (%) | 4.208 | 4.258 | -0.05 |

| United States 30-year bond (%) | 4.7984 | 4.8433 | -0.0449 |

Overview of the Australian Bond Market

Australian government bond yields rose on August 14, 2025, as solid jobs data tempered easing bets post-RBA cut, with longer maturities reflecting inflation vigilance. The 10-year yield climbed 2 basis points to 4.24%, 2-year up 2 basis points to 3.32%, 5-year +2 basis points to 3.62%, and 15-year +4 basis points to 4.61%. Monthly, yields declined (10-year -13 basis points), signaling dovish lean despite wage/employment alignment.

July’s 24.5k job gain (close to poll) and 4.2% unemployment (as expected) support RBA’s cautious stance, with Bullock noting data-driven “couple” more cuts possible amid June trade surplus strength. Global factors, like US-China truce extension and PPI surprise (up sharply), add caution, with US 10-year at 4.28%.

Traders monitor Fed path, swaps ~60% for September 25 basis-point cut from 4.25%-4.5%, as trade pacts ease uncertainty but sustain higher-rates view. Locally, net longs may have moderated on jobs resilience, focused on shorter ends amid bank rebounds. Tomorrow’s US retail sales (poll +0.5%) could influence if signaling consumer strength, bolstering bonds as hedges, though vigor caps falls. Dealers expect unchanged auctions August-October per guidance, with tariff clarity aiding diversification.

Overview of the US Bond Market

Bond traders boosted Treasury wagers amid inflation jitters, as yields climbed following hot PPI data, signaling caution on Fed cuts. The 10-year yield rose to 4.28% (up implied daily), the 2-year to 3.73% (-3 bp monthly adjustment), and the 30-year to 4.87% (+ implied). Shorter maturities saw buying on labor resilience, while longer ends reflected persistent pricing pressures.

A successful auction cycle supported sentiment, but yields firmed as oil steadied and gold held near $3,410/oz, amid US-Russia Ukraine tensions and Trump’s levy threats. On economics, July jobless claims at 224k (below poll) and PPI surge underscored inflation risks, countering CPI’s soft landing cues.

JPMorgan’s Treasury survey likely showed net longs expanding post-PPI, indicating hedging, with swaps at ~60% for September 25 basis-point cut and half-point easing by year-end. This amid Powell’s resistance to Trump easing pressure and potential dissent, as yields rose weekly. US trade war endurance, via EU/Japan pacts and China truce extension, bolsters higher-rates-longer, though services PMI strength aids bonds as growth buffers.

Cash surveys to August 13 revealed more longs and fewer shorts since mid-July, net longs at a high. CFTC through August 12 showed asset managers adding net longs by $12 million per basis point in shorter tenors, while leveraged funds increased shorts in 30-year by $2 million.

Dealers foresee steady coupon sizes for August-October per guidance, with 10-year up $1 billion from recent.