| Close | Previous Close | Change | |

|---|---|---|---|

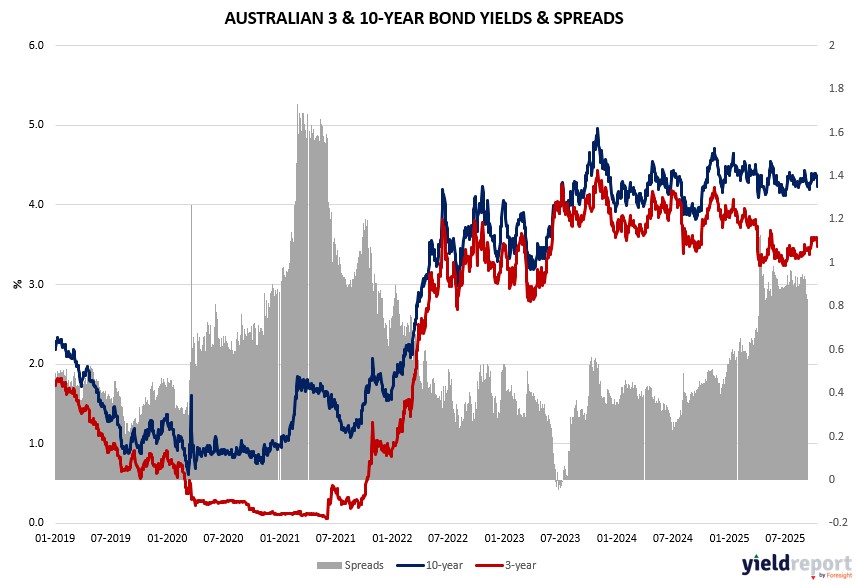

| Australian 3-year bond (%) | 3.475 | 3.474 | 0.001 |

| Australian 10-year bond (%) | 4.229 | 4.259 | -0.03 |

| Australian 30-year bond (%) | 4.907 | 4.933 | -0.026 |

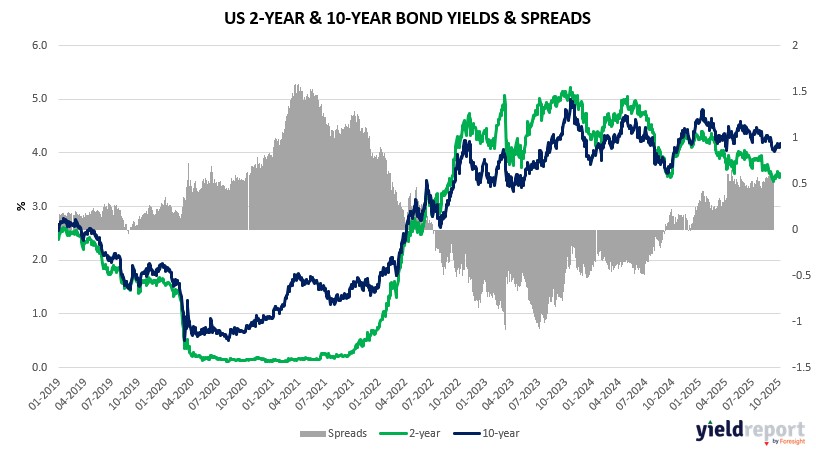

| United States 2-year bond (%) | 3.474 | 3.47 | 0.004 |

| United States 10-year bond (%) | 4.013 | 4.001 | 0.012 |

| United States 30-year bond (%) | 4.6101 | 4.592 | 0.0181 |

Overview of the Australian Bond Market

Australian government bond yields were little changed on October 15, 2025, with the 10-year steady at 4.23% and two-year up to 3.46%, as resource gains offset global trade noise. The 15-year held at 4.56%.

Leading index’s -0.03 signals tempered growth but supports RBA patience amid commodity tailwinds, per Sycamore’s view of hard-asset demand. US-China war risks could spur inflation, but Bessent’s truce proposal and ally coordination at IMF may de-risk, aligning with de-coupling avoidance. AUD rose 0.49% to 0.6518 on Fed dovishness.

Thursday’s employment data (20,000 jobs forecast, 4.3% unemployment) and RBA Governor Bullock speech could sway November cut odds, with strategists eyeing resilient lending and earnings for dip-buying. Funds rotate to defensives like health care and banks, though trade volatility may cap gains if AI guidance disappoints.

.

Overview of the US Bond Market

Treasury yields were mixed on October 15, 2025, with the 10-year steady at 4.03% after a two-year rally paused, the two-year up two basis points to 3.50% from 2022 lows, and the 30-year unchanged at 4.63%. Gold’s breach of $4200 reflected safe-haven bids amid trade war rhetoric.

Bessent’s truce extension float for rare-earth concessions, potentially beyond 90 days, tempered escalation fears, with coordinated ally responses eyed at IMF meetings involving Europe, Australia, Canada, India, and Asia. Trade Representative Greer’s skepticism on China’s curbs’ feasibility adds to negotiation hopes, though Trump’s war declaration introduces tail risks per Miran, prompting quicker Fed easing. Two-year yields rose from lows on resilient fundamentals, with HSBC’s Kettner forecasting beatable growth supporting risk assets.

JPMorgan surveys show net longs at lows, with asset managers trimming tenors by $23.5 million per basis point in CFTC data, signaling caution on trade-induced inflation. Dealers anticipate steady auction sizes for August-October per April guidance, with five- and ten-year up $1 billion. This week’s Philly Fed Thursday (8.5 forecast), retail sales (0.4% MM), and non-farm payrolls Sunday (50,000 jobs, 4.3% unemployment) could affirm consumer strength, influencing October cuts amid AI-driven earnings guidance watched by Bankrate’s Stephen Kates.