| Close | Previous Close | Change | |

|---|---|---|---|

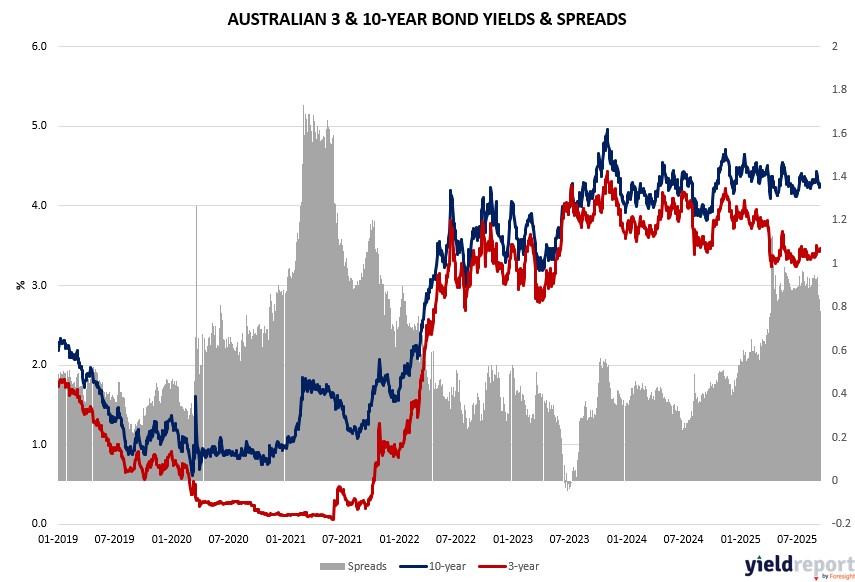

| Australian 3-year bond (%) | 3.464 | 3.45 | 0.014 |

| Australian 10-year bond (%) | 4.275 | 4.23 | 0.045 |

| Australian 30-year bond (%) | 4.983 | 4.94 | 0.043 |

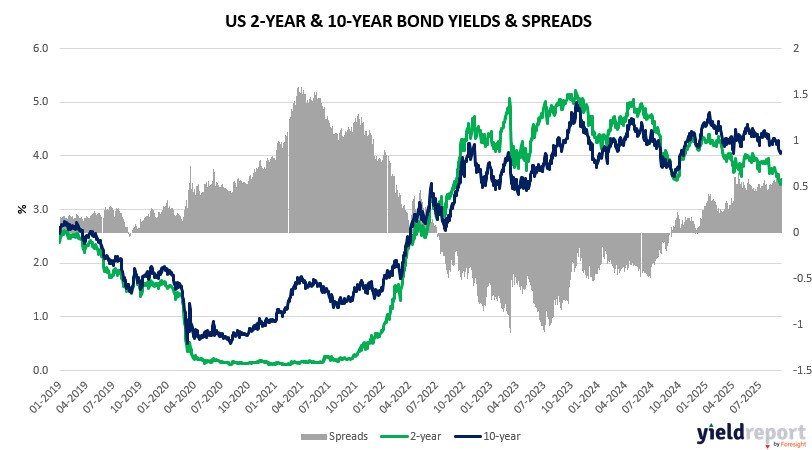

| United States 2-year bond (%) | 3.556 | 3.56 | -0.004 |

| United States 10-year bond (%) | 4.06 | 4.04 | 0.02 |

| United States 30-year bond (%) | 4.6834 | 4.66 | 0.0234 |

Overview of the Australian Bond Market

Government bond yields edged higher on September 15, 2025, with the 10-year up one basis point to 4.22%, 15-year and two-year also off one to 3.36% and 4.57%, five-year flat at 3.64%. The tick-up reflected consolidation in equities and caution ahead of pivotal data, though US futures gains hinted at Fed dovishness supporting rate-sensitive sectors like utilities.

China’s undershooting industrial production and retail sales added pressure on commodities, weighing materials, but lithium’s pop underscored supply chain shifts amid US efforts to counter China dominance—potentially filtering through to inflation via higher costs. With US import prices due Tuesday, retail sales forecast 0.2% monthly after 0.5% prior, industrial production -0.1%, then housing starts Wednesday and Fed funds target cut to 4.125% from 4.375% at 4pm GMT Thursday—median economists eye two 25 basis-point reductions by year-end, 40% betting three amid labor cracks like 263k claims last week.

RBA faces AU employment 22k forecast Thursday versus 24.5k prior, unemployment steady 4.2%, with composite leading index Wednesday potentially signaling slowdown if below 0.14%. If soft, aligns RBA with Fed easing, pressuring yields lower; hotter could cap moves. Upcoming claims for week ending 13 Sep at 240k, Philly Fed 2.5—any upside risks stagflation, but baseline favors cuts into re-acceleration per BofA’s Hartnett.

Positioning per outdated CFTC: trimmed longs, pared shorts signaling caution. Steady auctions expected. Gold unmoved near record, oil rebound aiding energy despite oversupply fears.

Overview of the US Bond Market

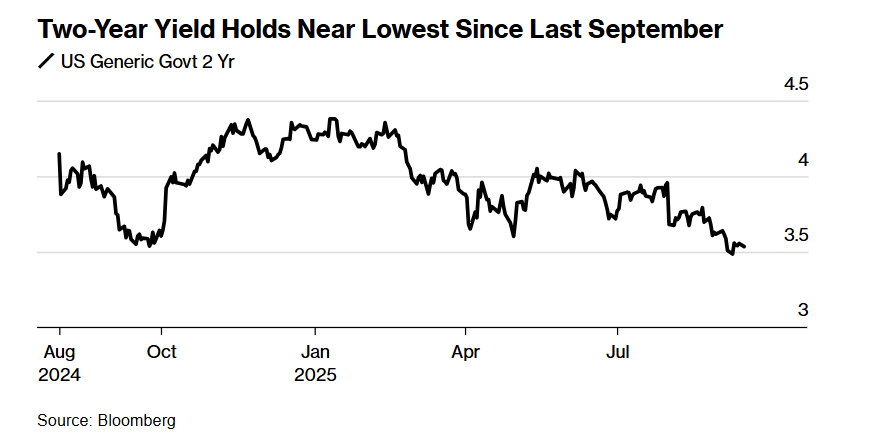

Bond markets echoed the dovish tilt. Two-year Treasury yields hovered near their lowest levels since last September, the 10-year yield fell to 4.04%, and the dollar softened. Gold rose to a record high, underscoring safe-haven demand. Investors widely expect a quarter-point cut, with markets now focused on the Fed’s pace of easing. Chair Jerome Powell’s press conference and the updated “dot plot” of rate forecasts will be key in shaping expectations. Analysts say any acknowledgment that inflation is “well anchored” or labor market conditions are “cooling” could extend dollar weakness and sustain the rally, though a cautious Fed tone may temper enthusiasm.

Trade developments added another layer. China accused Nvidia of antitrust violations linked to a 2020 deal, raising tensions during sensitive U.S.-China negotiations in Madrid. Separately, U.S. officials traveled to India for trade talks, signaling progress toward resolving outstanding disputes.

Bloomberg strategists noted that markets are unlikely to be rattled unless Tuesday’s U.S. retail sales report reveals a sharp consumer slowdown. For now, the soft-landing narrative remains intact.