| Close | Previous Close | Change | |

|---|---|---|---|

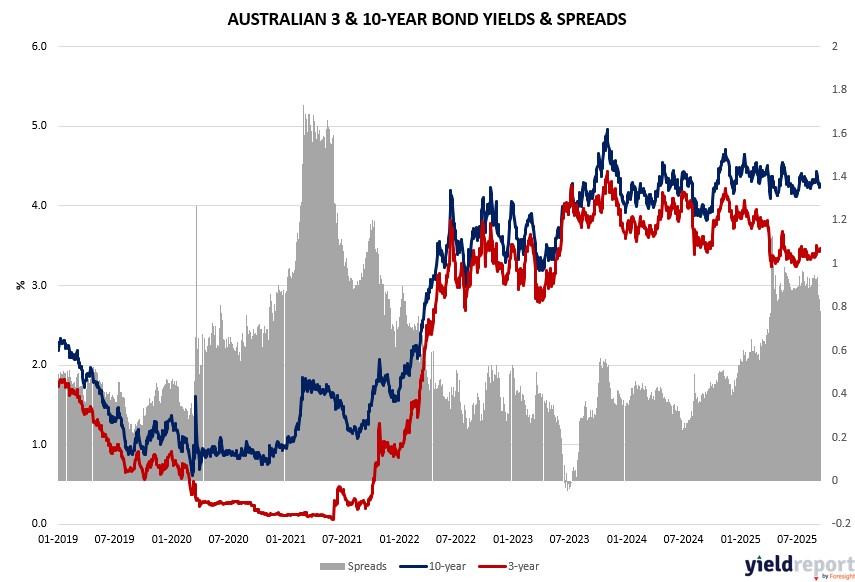

| Australian 3-year bond (%) | 3.43 | 3.464 | -0.034 |

| Australian 10-year bond (%) | 4.225 | 4.275 | -0.05 |

| Australian 30-year bond (%) | 4.938 | 4.983 | -0.045 |

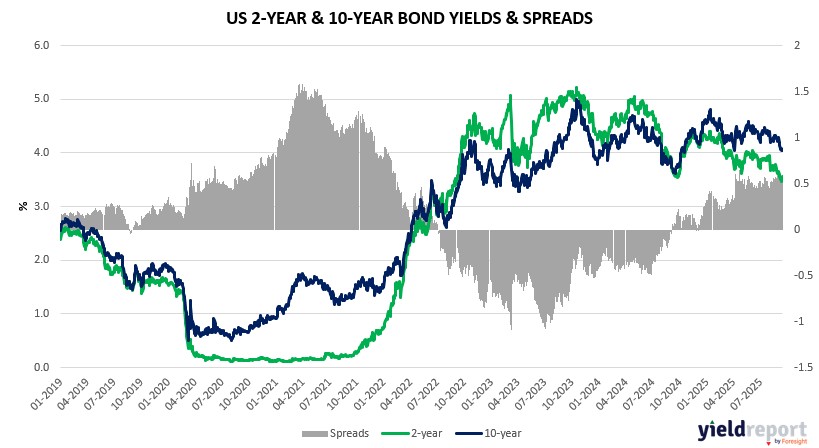

| United States 2-year bond (%) | 3.528 | 3.556 | -0.028 |

| United States 10-year bond (%) | 4.038 | 4.06 | -0.022 |

| United States 30-year bond (%) | 4.6582 | 4.6834 | -0.0252 |

Overview of the Australian Bond Market

Australian government bonds saw yields decline modestly on September 16, 2025, as traders positioned ahead of the Federal Reserve’s decision and local data. The 2-year yield fell 4 basis points to 3.36%, the 5-year dropped 4 basis points to 3.64%, the 10-year slid 5 basis points to 4.22%, and the 15-year eased 4 basis points to 4.58%. The moves reflected caution amid global rate cut expectations, with the composite leading index for August due Tuesday potentially signaling economic momentum.

Macro views blended with bond trading suggest resilience in consumer sectors, as US retail sales topped forecasts, supporting a soft-landing narrative that could cap aggressive easing. Yet, with Australian employment data Thursday eyed for 21,000 job gains and steady 4.2% unemployment, any labor weakness might pressure the RBA toward cuts later in the year. Dealers anticipate steady auction sizes in coming months, aligning with April guidance, as tariff truce talks with China offer one option for a 90-day extension per Bessent.

Overview of the US Bond Market

Bond traders trimmed bets on aggressive Federal Reserve easing following strong retail sales on September 16, 2025, with Treasuries edging higher in a solid 20-year sale. The 2-year yield fell 3 basis points to 3.51%, the 10-year held steady at 4.03%, and the 30-year was little changed at 4.65%. Gains were led by shorter maturities as markets fully priced a quarter-point Fed cut on September 17, with projections for six cuts over the next year hinging on labor data.

Blending macro commentary, the 0.6% retail sales advance indicates consumer health not yet impacted by job softness, per TradeStation, reducing longer-term dovish hopes. Initial jobless claims Thursday are forecast at 240,000, while Philly Fed index at 2.5 could affirm industrial stability. JPMorgan surveys showed net long positions shrink to two-month lows, reflecting less bullishness amid Trump pressure on Powell and potential dissents. Asset managers pared longs by $23.5 million per basis point, concentrated in 5-year and bond contracts, as deals with Europe and Japan ease uncertainty, bolstering views for higher rates longer.