| Close | Previous Close | Change | |

|---|---|---|---|

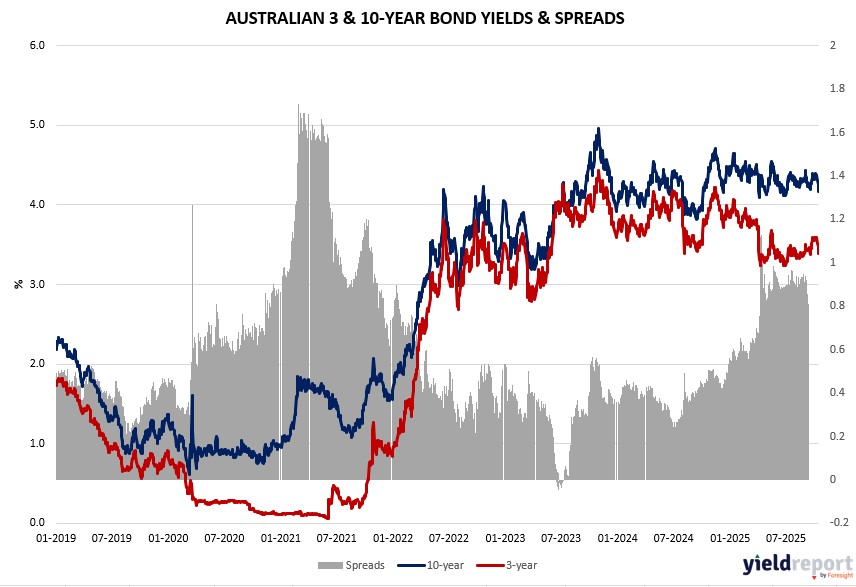

| Australian 3-year bond (%) | 3.314 | 3.393 | -0.079 |

| Australian 10-year bond (%) | 4.099 | 4.17 | -0.071 |

| Australian 30-year bond (%) | 4.837 | 4.866 | -0.029 |

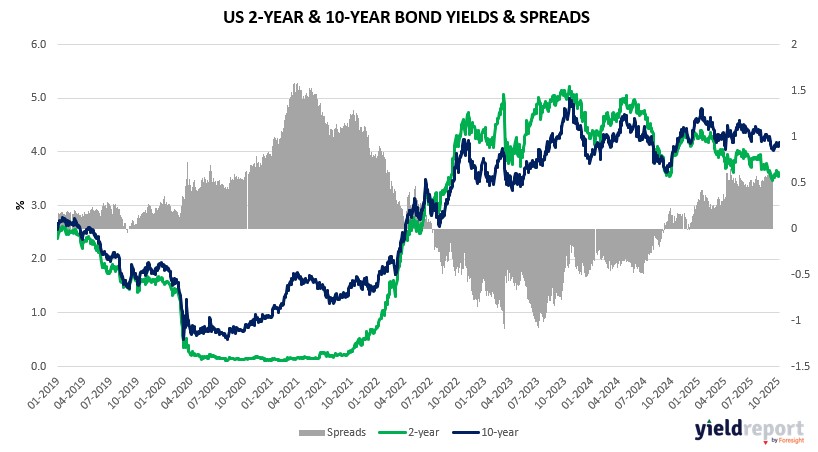

| United States 2-year bond (%) | 3.393 | 3.495 | -0.102 |

| United States 10-year bond (%) | 3.3957 | 4.022 | -0.6263 |

| United States 30-year bond (%) | 4.5768 | 3.6129 | 0.9639 |

Overview of the Australian Bond Market

Australian government bond yields eased slightly, with the two-year yield down six basis points to 3.28% and the 10-year slipping five basis points to 4.09%, as softer jobs data bolstered rate cut bets amid global volatility. The 5-year yield fell six basis points to 3.50%, and the 15-year dropped four basis points to 4.45%. The Aussie dollar weakened 0.13% to 0.6476 against the US dollar, influenced by trade war jitters despite Trump’s optimistic tone.

September employment growth disappointed at 14.9 thousand, with unemployment rising to 4.5%, heightening expectations for the RBA easing to support a cooling labour market. The composite leading index’s decline points to subdued growth, potentially offsetting tariff impacts from US-China talks.

Deal flows reflected caution, with energy and financials dragging amid US regional bank contagion fears, though gold’s safe-haven appeal supported related assets.

Overview of the US Bond Market

Bond prices fell as yields climbed across the curve, with the two-year Treasury yield rising three basis points to 3.46% from its lowest since 2022, reflecting reduced expectations for aggressive Fed easing amid trade optimism and resilient data. The 10-year yield advanced three basis points to 4.00%, while the 30-year edged up one basis point to 4.60%. The dollar held steady after its worst week since August, as Trump’s soothing trade comments diminished safe-haven demand for Treasuries.

The government shutdown continues to obscure economic visibility, but analyses of state-level data showed initial jobless claims dropping, underscoring labor market stability despite earlier weak non-farm payrolls of around 50,000 for September, below the 223,000 polled. Unemployment ticked up slightly to 4.5%, higher than the 4.3% forecast, adding to calls for Fed action. Fed’s Musalem emphasized meeting-by-meeting decisions, supporting another rate cut to aid a softening jobs picture, while Morgan Stanley sees a quarter-point move in October.

Housing starts and retail sales data from mid-week pointed to mixed consumer health, with starts below estimates at levels implying ongoing sector challenges. Import prices and trade balance figures later in the week could influence tariff discussions, as Treasury Secretary’s comments on extending the US-China truce—potentially by 90 days—eased global risk fears, pressuring yields higher.

Bond traders trimmed long positions ahead of key auctions, with JPMorgan’s survey showing net longs at two-month lows, suggesting caution amid high valuations and potential tariff passthrough in inflation data. Asset managers pared net longs in Treasury futures by $23.5 million per basis point, focused on shorter tenors, while leveraged funds reduced shorts in longer bonds.

Dealers anticipate steady coupon auction sizes for November-January, aligning with prior guidance, with the next 10-year reopening expected at $42 billion and 30-year at $25 billion.