| Close | Previous Close | Change | |

|---|---|---|---|

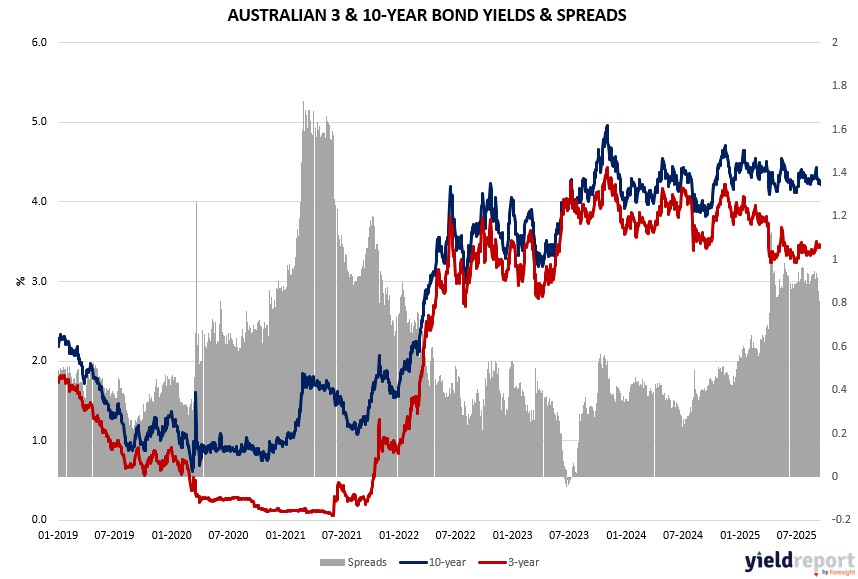

| Australian 3-year bond (%) | 3.427 | 3.43 | -0.003 |

| Australian 10-year bond (%) | 4.226 | 4.225 | 0.001 |

| Australian 30-year bond (%) | 4.943 | 4.938 | 0.005 |

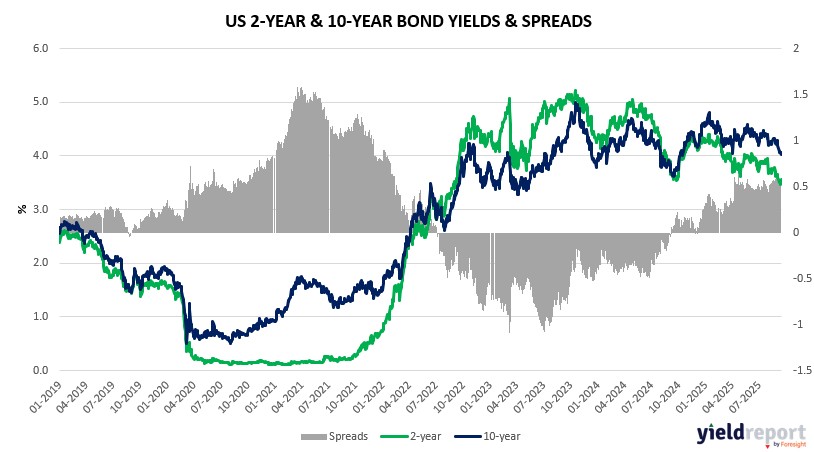

| United States 2-year bond (%) | 3.516 | 3.528 | -0.012 |

| United States 10-year bond (%) | 4.022 | 4.038 | -0.016 |

| United States 30-year bond (%) | 4.6256 | 4.6582 | -0.0326 |

Overview of the Australian Bond Market

Australian government bond yields ticked higher on September 17, 2025, as pre-Fed positioning and a stronger global tone pressured prices ahead of the central bank’s cut. The 2-year yield rose 1 basis point to 3.37%, the 5-year climbed 2 basis points to 3.65%, the 10-year advanced 3 basis points to 4.24%, and the 15-year edged up 2 basis points to 4.60%. The uptick reflected caution over Powell’s potential signals on easing pace, with the composite leading index’s 0.05% August drop underscoring domestic softening that could nudge the RBA toward cuts if Thursday’s jobs data disappoints at the expected 21.5 thousand addition and 4.2% unemployment.

Macro dynamics blended into trading suggest tariff uncertainties may keep inflation elevated, mirroring US concerns, while China’s equity strength and iron ore resilience support Australia’s relative appeal. The AUD’s dip to 0.667 highlighted dollar resilience despite the Fed move, as Pepperstone’s Chris Weston noted outperformance against peers tied to stable politics and growth. Dealers eye steady auction sizes through October per April guidance, with potential China tariff truce extensions offering 90-day buffers per Treasury Secretary Bessent, potentially easing import cost pass-throughs.

Overview of the US Bond Market

US Treasuries declined across the curve on September 17, 2025, as the Federal Reserve’s rate cut disappointed traders betting on deeper easing, pushing yields higher in a post-decision reassessment. The 2-year yield rose to 3.55% from prior levels, the 5-year to 3.65% up 6 basis points, the 10-year to 4.09% up 5 basis points, and the 30-year to 4.69%. Shorter maturities led losses after a solid 20-year auction, with the dollar index steady as Powell’s “insurance cut” framing tempered dovish bets.

Integrating macro insights, the 25 basis-point reduction to 4%-4.25% shifted focus to labor risks, with Powell noting job growth below break-even and unemployment edging to 4.3%, though immigration slowdowns suggest structural drags over cyclical woes. Housing starts’ miss at 1.307 million reinforced employment downside, while sticky goods inflation from tariffs—up in August per prior data—complicates the dual mandate, as Wolfe Research’s Stephanie Roth highlighted tougher trade-offs ahead. JPMorgan client surveys showed net longs at two-month lows pre-meeting, with asset managers trimming $23.5 million per basis point in futures, concentrated in 5- and 10-year contracts, amid Trump pressures on Powell and potential dissents. CFTC data indicated leveraged funds paring shorts by $5-6.5 million, but resilient consumer spending from Tuesday’s retail sales beat bolsters views for higher rates longer, with swap contracts now pricing under 50 basis points easing by year-end. Auction sizes are seen unchanged through Q4, aligning with Treasury guidance.