| Close | Previous Close | Change | |

|---|---|---|---|

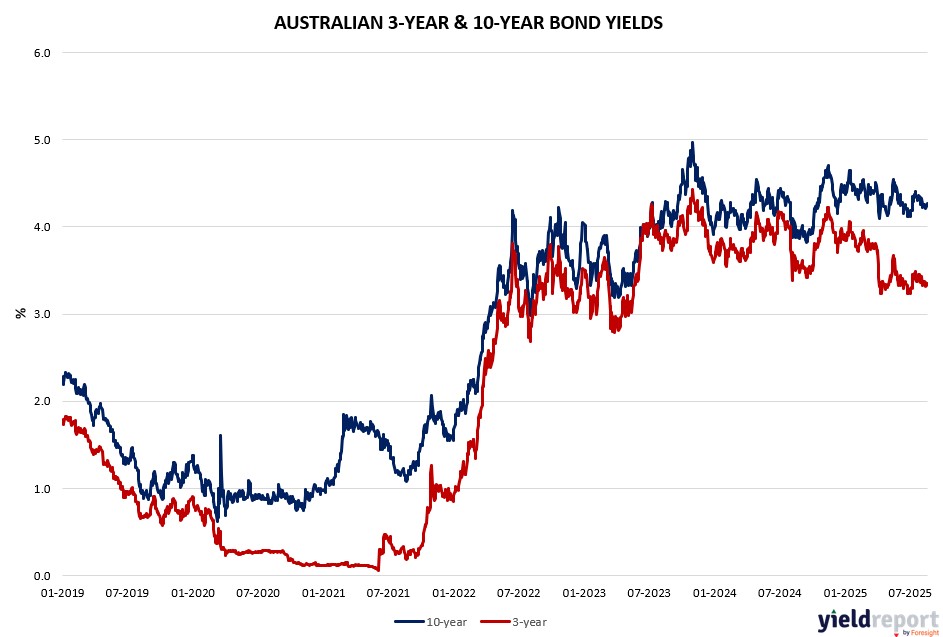

| Australian 3-year bond (%) | 3.398 | 3.347 | 0.051 |

| Australian 10-year bond (%) | 4.328 | 4.273 | 0.055 |

| Australian 30-year bond (%) | 5.074 | 5.016 | 0.058 |

| United States 2-year bond (%) | 3.761 | 3.742 | 0.019 |

| United States 10-year bond (%) | 4.328 | 4.297 | 0.031 |

| United States 30-year bond (%) | 4.9254 | 4.8979 | 0.0275 |

Overview of the Australian Bond Market

Australian yields rose sharply on August 19, 2025, as equity dip and earnings volatility spurred safe-haven outflows, though monthly gains limited amid dovish RBA path. 10-year up 8 basis points to 4.32% (+5 daily per data), 2-year +4 to 3.36%, 5-year +5 to 3.68%, 15-year +8 to 4.69%. Monthly up slightly (10-year -2 bp), reflecting caution despite resilience.

July labor/wages support gradual cuts post-3.60%, Bullock data-tied with trade surplus boost. Global, US housing beat (1.428M vs. poll), China extension, Ukraine summit promise (Trump-Putin call, potential trilateral) ease energy risks if de-escalation holds.

Traders added longs post-dip, Fed swaps ~60% September 25 bp from 4.25%-4.5%, pacts sustaining higher-rates, pressuring prices. Locally, yields firmed on bank rebounds, shorter focus. Tomorrow’s AU/US PMIs could sway if soft, aiding bonds as hedges, though vigor caps. Dealers stable auctions August-October per guidance, summit progress aiding diversification.

Overview of the US Bond Market

Bond traders trimmed Treasuries as yields dipped slightly on housing surge, bracing for PMIs amid media deregulation debates and truce extensions. The 10-year yield fell to 4.31% (down 1 basis point), 2-year to 3.75% (flat), 30-year to 4.91% (-1 bp). Shorter maturities steady as oil held, gold dipped amid Ukraine talks progress—Trump’s Putin call and potential Zelenskyy meeting raise de-escalation hopes, possibly easing energy volatility.

July housing 1.428 million (beat poll) counters industrial miss, bolstering growth view post-CPI/PPI. FCC’s TV cap abolition push, enabling mergers like Nexstar-Tegna, highlights deregulation under Trump, potentially impacting media bonds via consolidation.

JPMorgan survey net longs at low, caution persists, swaps ~60% September 25 bp cut, half-point year-end. Powell resists Trump easing amid dissent, yields down weekly. Trade war resilience via EU/Japan, China extension favors higher-rates-longer, though PMIs could affirm soft landing, bonds hedging volatility from stalled Ukraine summit if no quick resolution.

Cash surveys to August 18: fewer longs, more shorts, net low. CFTC August 15: asset managers added net longs $8 million per basis point in shorter, leveraged trimmed 10-year shorts $2 million.

Dealers unchanged auctions August-October per guidance, 10-year +$1 billion recent.