| Close | Previous Close | Change | |

|---|---|---|---|

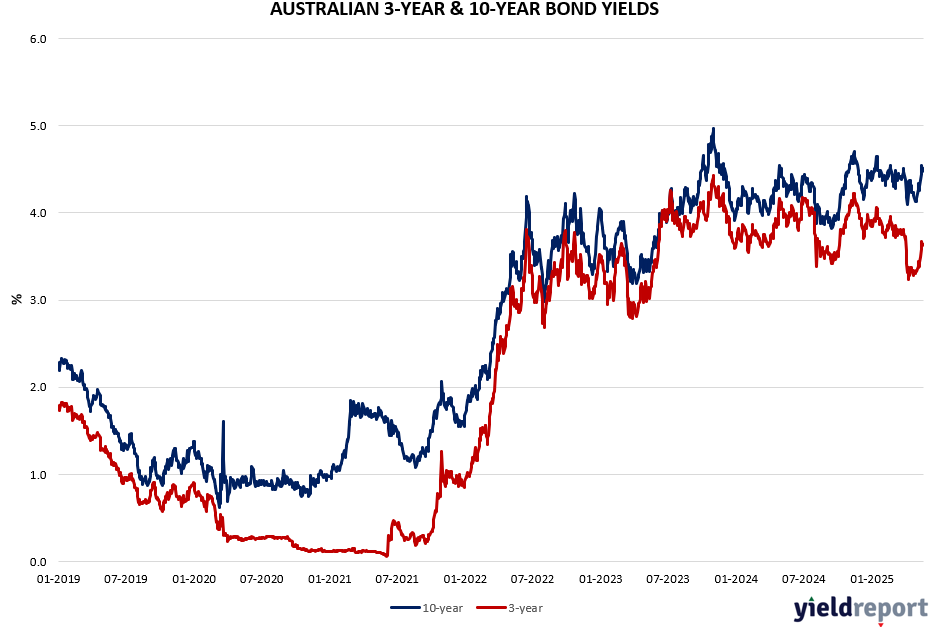

| Australian 3-year bond (%) | 3.476 | 3.636 | -0.16 |

| Australian 10-year bond (%) | 4.41 | 4.515 | -0.105 |

| Australian 30-year bond (%) | 5.054 | 5.154 | -0.1 |

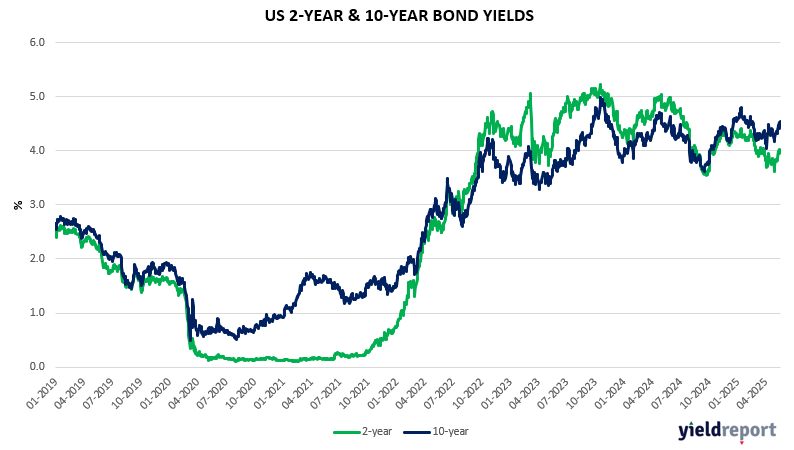

| United States 2-year bond (%) | 3.97 | 3.983 | -0.013 |

| United States 10-year bond (%) | 4.481 | 4.475 | 0.006 |

| United States 30-year bond (%) | 4.967 | 4.941 | 0.026 |

Overview of the Australian Bond Market

Post the RBA decision, the 3-year government bond yield fell a very large 15 bps to 3.50% and the 10-year return lost 5 bps to 4.44%. Yields fell as the tone of the RBA’s statement appeared more dovish than the market had anticipated. Which is why the more interest rate sensitive part of the curve fell so significantly. Additionally, feeding into to those yield moves, the RBA reduced its inflation projections reflecting a view that risks have subsided to a degree and indicating that headline inflation will likely remain near the midpoint of the 2–3% target range throughout much of the forecast period. All up, both the market and economists will likely increase the number or degree of expected interest rate cuts.

In money markets, bond traders rapidly dialled up rate cut expectations and now expect the cash rate to end the year at 3.17%. That compares to 3.3% before the policy meeting and implies between two and three additional rate cuts by Christmas. Over 1H2026, the implied rate is slightly above 3.0% – call it the terminal rate.

Meanwhile, BondAdviser has noted that last week demonstrated that demand for Tier 2 paper, or floating rate note (FRN) subordinated debt (largely issued by Australian banks) remains stronger than ever. BondAdviser noted that the 5-year marker for Big Four FRNs ended Friday at +158bps, marking ~13bps of compression for the week and almost 50bps since April’s peak. This compares to the Feb-24 tights of +144bps and closer to +150bps at the beginning of the year when both ANZ and WBC priced 10NC5 deals at +152bps (on 8-Jan and 6-Feb respectively).

For domestic retail investors, there are several managed funds and ETFs provide exposure to Australian FRN subordinated debt, with Coolabah the largest domestic fund manager in the segment.

Overview of the US Bond Market

The yield on the US 10-year Treasury rose up to 7bps to 4.52% on Tuesday, after a volatile session on Monday during which the benchmark briefly touched a one-month high. Investors continued to evaluate the US fiscal and economic outlook amid growing concerns. Fiscal worries were further intensified by the approval of President Trump’s tax-cut legislation by a key congressional committee. The interest rate sensitive 2-year declined 2bps to 3.98%. That is, further steepen in the curve, call it the ‘fiscal term premium’. And all of this feeds into the narrative of being invested in the short-end and medium-end of the curve.

Meanwhile, Fed officials continue to strike a cautious tone. New York Fed President Williams and Atlanta Fed President Bostic indicated that policymakers are unlikely to consider interest rate cuts in the near term. Markets are currently pricing in two 25-basis-point rate cuts by the end of the year, possibly in September and December.

Meanwhile KKR & Co., have published a note stating that US government bonds are no longer working as an effective hedge against risky assets, creating a challenge for global investors and spurring a search for asset diversification. Bigger fiscal deficits and stickier inflation suggest that bonds will not always rally when stocks sell off, breaking down the traditional relationship between the two assets, Henry McVey, KKR’s head of global macro and asset allocation, said in a research note. “During risk off days, government bonds are no longer fulfilling their role as the ‘shock-absorbers’ in a traditional portfolio,” McVey wrote