| Close | Previous Close | Change | |

|---|---|---|---|

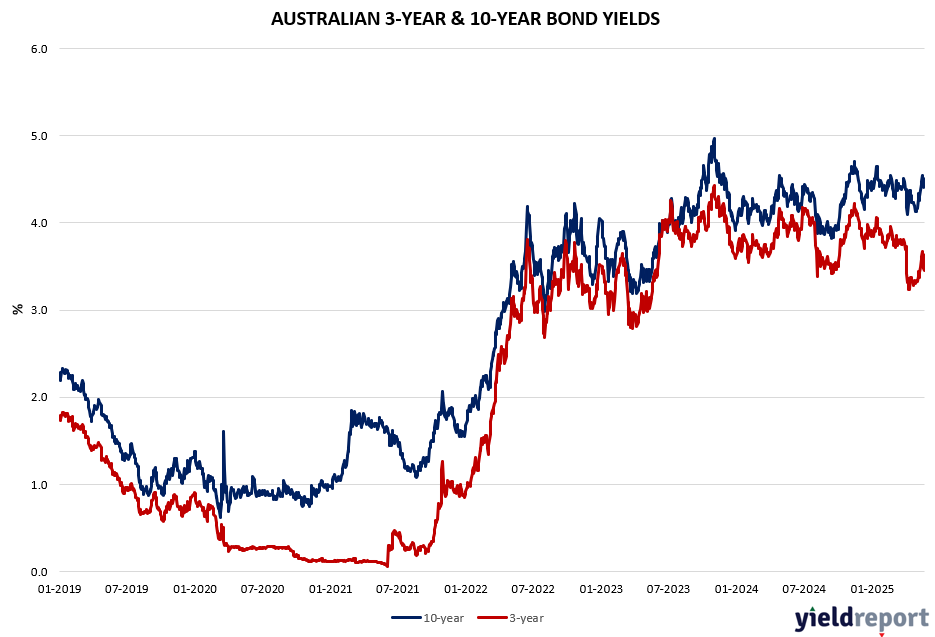

| Australian 3-year bond (%) | 3.456 | 3.476 | -0.02 |

| Australian 10-year bond (%) | 4.419 | 4.41 | 0.009 |

| Australian 30-year bond (%) | 5.083 | 5.054 | 0.029 |

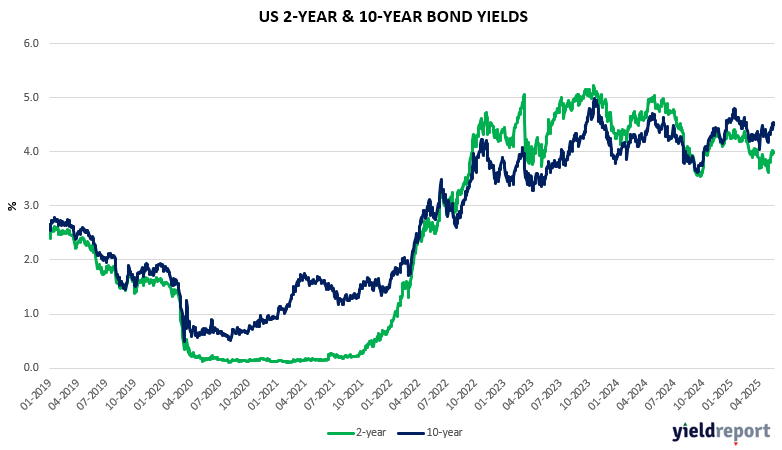

| United States 2-year bond (%) | 3.962 | 3.97 | -0.008 |

| United States 10-year bond (%) | 4.483 | 4.481 | 0.002 |

| United States 30-year bond (%) | 4.9717 | 4.967 | 0.0047 |

Overview of the Australian Bond Market

Australia’s 10-year government bond yield rose to around 4.49% on Wednesday after a 5 bps decline in the previous session with the RBA cutting rates as expected. The 5bps rise on Wednesday offset the Tuesday move. The more interest rate sensitive 2-year increased 4 bps after a very large 15 bps decline on Tuesday post the RBA decision. The increase in Australian yields also mirrored a broader rise in US Treasury yields amid rising concerns about the US economic and fiscal outlook. There is significant trouble becoming manifest in the long end of curve, and it is coming from the US market. While the RBA is guiding the market down, the Australian bond market in terms of pricing does not operate in isolation to the world – and US yields at the long-end have increased significantly, particularly this week, with the long-end being absolutely hammered on ballooning budget deficit concerns. And that is bad news for Australian government debt servicing – spare a thought for Victorians, with the state currently paying $26m a day on interest.

The RBA governor’s dovish tone on Tuesday prompted CBA to bring forward its expectations for future rate cuts to August and September and said the RBA’s shift in tone on inflation was the “catalyst”. CBA stated that the risk now lies with a quicker easing and July cannot be ruled out… if the global situation deteriorates, there is the risk the RBA might have to take the cash rate into slightly stimulatory territory. It added that risks were “building to the downside”, pointing to a tepid recovery in consumer demand and uncertainty in the international environment owing to trade tariffs. CBA stated that the risk lies with additional easing and a quicker easing and July cannot be ruled out, but the RBA would have to see hard data for this to materialize.

Overview of the US Bond Market

Pay attention to today’s trade – it way very significant regarding US Treasuries ‘safe haven’ status and it likely portends troubles ahead for bond markets at the long-end of the curve. US fiscal matters have dominated again over the last 24 hours, as investors continue to grapple with what the long-term unsustainable nature of US debt means in the near term. A 20-year bond auction was met with very tepid demand and ended up being priced slightly higher than expected despite the high yields. Why? The tax bill in front of the House Rules Committee (the ‘Big Beautiful Bill’) which would only further add to the US deficit. A day in which Wall Street’s worries about a ballooning deficit that threatens America’s status as a safe haven became manifest. Watch this space about the tax bill. Will Trump blink again on account of the bond markets???

As news on the weak auction rolled out circa mid-day, treasuries got hammered. Not surprisingly, given we are talking about budget deficits, long-term debt bore the brunt of the selling, with 30-year yields jumping 10 bps to 5.08% and toward the highest since October 2023. The 20-year bonds jumped 12 bps to 5.11%. The 10-year jumped 10 bps to 4.60%. The two-day moves on all the above have been universally significant at the circa 15-20 bps level. Safe haven???? These developments this week only reinforce investor concerns about just how ‘safe’ US Treasuries are. Keep in mind that is the long-end of the curve that US main street. For example, housing mortgages are based on the 30-year.

Long-term Treasury yields have already been moving higher as the tax-cut plan adds to investor concerns about the surging debt load, with Moody’s Ratings on Friday lowering the nation’s credit score below the top triple-A level. Trump said his tax package is close to being finalized, having notched a deal over the state and local tax deduction, but the White House has yet to win over a faction of conservatives who want more austere spending cuts. Former US Treasury Secretary Steven Mnuchin said he’s more alarmed by the country’s growing budget deficit than its trade imbalances, and urged Washington to prioritize fiscal repair.

And encapsulating all the issues in the US and impacts on the bond markets, the giants of corporate America from Pfizer Inc. to Alphabet Inc. are borrowing in euros like never before as the anxiety triggered by President Donald Trump’s tariff threats pushes them to hunt for alternative funding avenues in case their home market freezes up. A record number of these so-called reverse Yankee deals have been sold this year. The shift is driven by anxiety over President Donald Trump’s tariff threats, dollar volatility, and fears about the US debt burden, making the European market a more attractive funding avenue.