| Close | Previous Close | Change | |

|---|---|---|---|

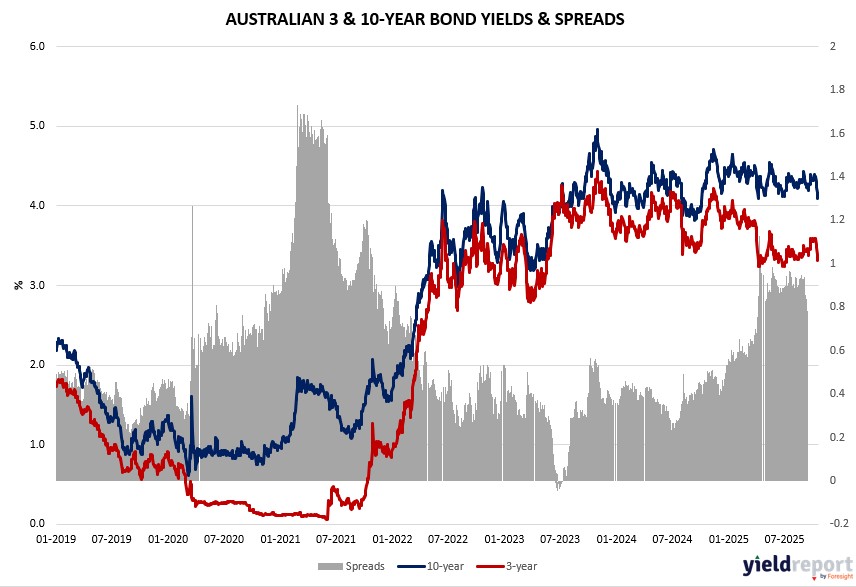

| Australian 3-year bond (%) | 3.348 | 3.375 | -0.027 |

| Australian 10-year bond (%) | 4.126 | 4.159 | -0.033 |

| Australian 30-year bond (%) | 4.824 | 4.869 | -0.045 |

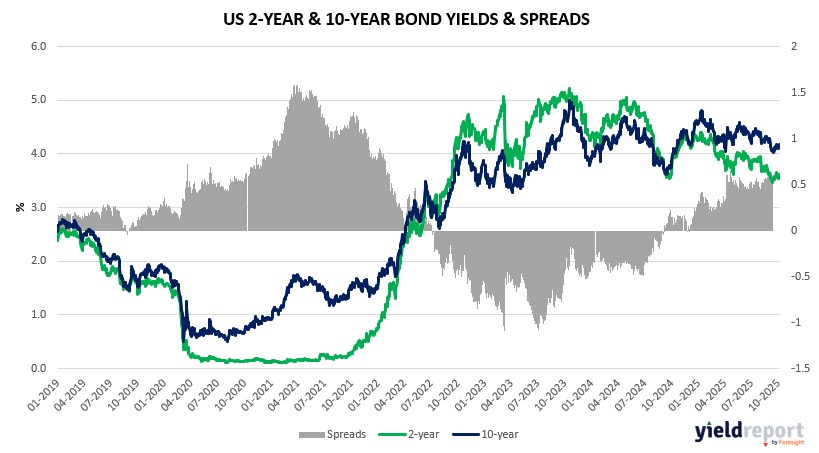

| United States 2-year bond (%) | 3.459 | 3.466 | -0.007 |

| United States 10-year bond (%) | 3.976 | 3.995 | -0.019 |

| United States 30-year bond (%) | 4.5664 | 4.5872 | -0.0208 |

Overview of the Australian Bond Market

Australian government bond yields rose modestly on October 21, 2025, with the 10-year up 3 basis points to 4.12%—wait, data shows +4.12% but that’s the yield level; intraday change was -3 basis points per table—tracking mixed global signals from US yield dips and commodity volatility, though a firmer AUD/USD down 0.3% limited upside. The 2-year yield eased 1 basis point to 3.32%, reflecting caution ahead of domestic PMI data, while longer ends like the 15-year climbed to 4.45% amid resource sector strength signaling economic resilience.

Macro blends included gold’s global tumble reducing haven flows, but persistent central bank buying and emerging market trends could support a rebound, per analysts, with local funds shifting toward resources at the expense of staples and tech. Positioning may face tests from upcoming October 23 PMIs, where manufacturing is eyed after 51.4 last period, potentially pressuring yields if softness emerges amid tariff talks and China’s influence on commodities.

With oil’s glut aiding inflation outlooks and consumer power, bonds could stabilize if CPI data on October 24 aligns with US polls for 0.3% core monthly gain, though Australia’s export ties to China add sensitivity to trade progress. Dealers anticipate steady auction sizes, aligning with global patterns, as the RBA monitors for easing signals.

Overview of the US Bond Market

Treasury yields edged lower on October 21, 2025, with the 10-year note down 2 basis points to 3.96%, as investors sought safety amid gold’s rout and mixed equity performance, though a stronger dollar capped declines. Longer-dated bonds outperformed, with 30-year yields falling 3 basis points to 4.54%, reflecting bets on cooling inflation from lower oil prices, which strategist Ed Yardeni suggested could push 10-year yields toward 3.75% if crude continues sliding and the Fed eases next week.

The bond market’s moves blended macro influences, including positive US-China trade developments reducing haven demand and the government shutdown adding uncertainty to investor positioning, potentially leading to oversized bets in commodities. PineBridge Investments boosted gold exposure at bonds’ expense, viewing Treasuries as less reliable in a “zig-zag” risk environment, while HSBC, Morgan Stanley, and UBS strategists maintained bullish equity outlooks but advised diversification amid high valuations and tariff risks.

Positioning data showed asset managers trimming net long Treasury futures for the week ended October 14, per delayed CFTC figures, with cuts concentrated in 5- and 30-year contracts, while leveraged funds reduced shorts in the classic bond. JPMorgan’s client survey indicated shrinking net longs ahead of this week’s data releases, including existing home sales on October 23 and core CPI on October 24, where economists poll for a 0.3% monthly rise that could reinforce steady Fed policy if met.

Dealers expect the Treasury to hold coupon auction sizes steady for November-January, aligning with prior guidance, as the department announces quarterly refunding details soon. With consumer confidence holding amid job concerns and oil’s glut boosting purchasing power, bonds could see further support if upcoming PMIs and CPI data signal softening, though resilience in equities and deals with trading partners like China may keep yields from dropping sharply.