| Close | Previous Close | Change | |

|---|---|---|---|

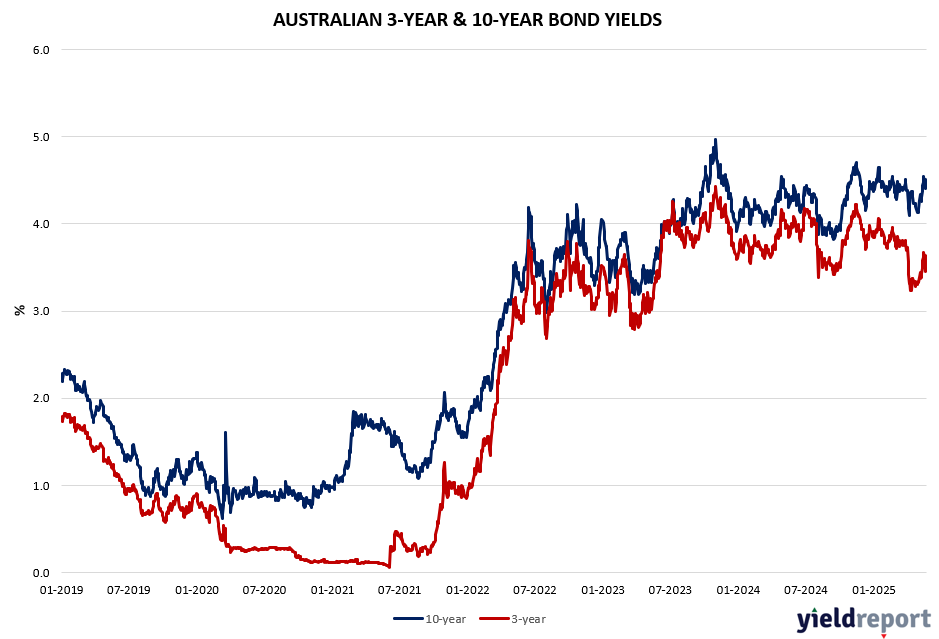

| Australian 3-year bond (%) | 3.492 | 3.456 | 0.036 |

| Australian 10-year bond (%) | 4.477 | 4.419 | 0.058 |

| Australian 30-year bond (%) | 5.171 | 5.083 | 0.088 |

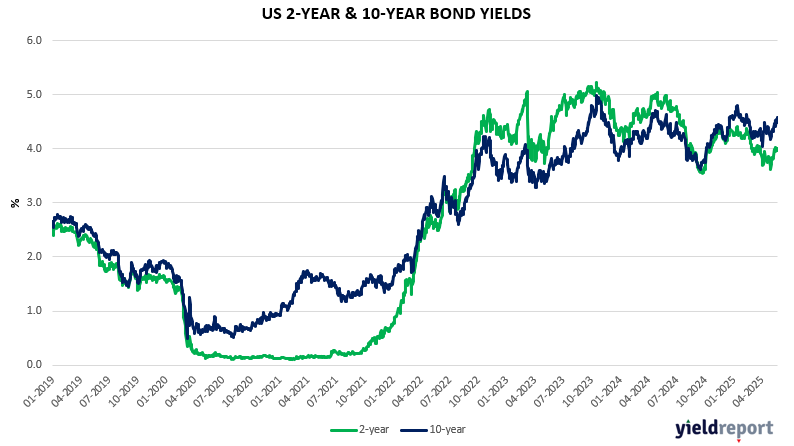

| United States 2-year bond (%) | 4.005 | 3.962 | 0.043 |

| United States 10-year bond (%) | 4.581 | 4.483 | 0.098 |

| United States 30-year bond (%) | 5.0827 | 4.9717 | 0.111 |

Overview of the Australian Bond Market

Australia’s 10-year government bond yield increased 2 bps to around 4.51% on Thursday. The Tuesday declines have now been offset, with the market taking its cues once again from the US treasuries market. While the RBA is guiding

the market down, the Australian bond market in terms of pricing does not operate in isolation to the world – and US yields at the long-end have increased significantly, particularly this week, with the long-end being absolutely hammered on ballooning budget deficit concerns. And that is bad news for Australian government debt servicing – spare a thought for Victorians, with the state currently paying $26m a day on interest.

Overview of the US Bond Market

US treasury markets calmed today after the significant ructions and upward moves in long-end yields yesterday. The US 10-year Treasury note fell 6 bps to 4.54%. The US 30-year Treasury note fell 4 bps to 5.05%.

President Donald Trump’s signature tax bill narrowly passed the House Thursday morning, advancing a sprawling multi-trillion dollar package that would avert a year-end tax increase at the expense of adding to the US debt burden.

The bill now heads to the Senate, where groups of Republicans are pressing for extensive change. Lawmakers plan to vote on approval by August. The bill includes a $4 trillion increase in the US debt ceiling, which the Treasury Department forecasts could otherwise force a default as soon as August or September, adding urgency to the timeline.

On the topic of the fiscal deficit, even if the inability to reduce the deficit in the US doesn’t lead to default, a large deficit still implies greater bond supply, and perhaps eventual inflation as the debt is monetized to avoid default. Either way, it makes nominal fixed-income instruments less attractive as long-term investments.

Which brings us to the Bond Vigilantes. If Trump is going to shepherd the signature legislative package of his second term through the Senate, he may have to reckon with an even more demanding constituency: customers for the ballooning amount of US debt. The moves yesterday were reminiscent of Trump’s wrangle with the bond markets last month, when he blinked. In the early morning hours of April 9, Treasury yields surged as Trump’s steep retaliatory tariffs — the highest in more than a century — went into effect. While a months-long slump in equities barely fazed him, the bond market got his attention. If Treasuries continue to stay queasy, the higher yields not only threaten to dampen economic growth — as they translate into higher borrowing costs for everything from homes to cars — but to accelerate the government’s fiscal deterioration. As rates rise, so does the Treasury’s interest bill. Let’s be honest, the bond market hates this tax bill.

On the economic front, Existing Homes Sales for April declined more than expected. The figure represents the slowest pace in seven months, restrained by affordability constraints and highlighting a lackluster start to the spring selling season. More significantly, it was the weakest April since 2009. Odds of a sustained pickup in the resale market are limited as mortgage rates march higher and prices stay elevated, despite more listings coming on the market. What’s more, consumer sentiment is near the lowest level on record, and the share who say now is a good time to buy a home is also close to an all-time low, according to the University of Michigan. Mortgage rates rebounded last week to a three-month high of 6.92%, and are continuing to move up even more as Treasury yields climb. It is the 30-year that sets mortgage rates – where the rubber hits the road regarding Main Street. New Home Sales out on Friday.

Other data Thursday pointed to a stable labor market and improved business activity after a slump in April. Initial jobless claims were little changed last week, the period when the government surveys for the May employment report. The S&P Global flash May composite index of business output rose as anxiety on tariffs eased.

Weigh all the above up – just reinforces the Fed’s ‘wait-and-see’ approach.