| Close | Previous Close | Change | |

|---|---|---|---|

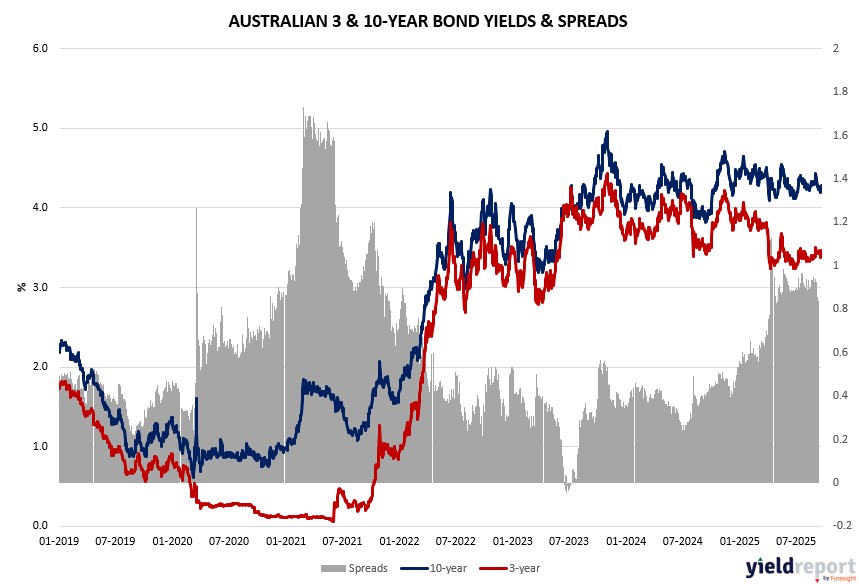

| Australian 3-year bond (%) | 3.46 | 3.436 | 0.024 |

| Australian 10-year bond (%) | 4.284 | 4.248 | 0.036 |

| Australian 30-year bond (%) | 5.027 | 4.992 | 0.035 |

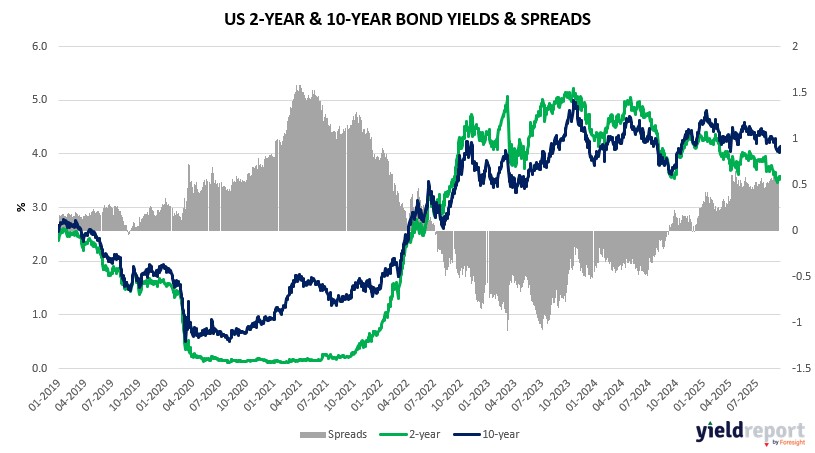

| United States 2-year bond (%) | 3.576 | 3.576 | 0 |

| United States 10-year bond (%) | 4.131 | 4.129 | 0.002 |

| United States 30-year bond (%) | 4.7507 | 4.7507 | 0 |

Overview of the Australian Bond Market

Australian government bond yields climbed on September 22, 2025, amid commodity-driven equity strength and global firming, as traders eye Wednesday’s CPI for RBA cues post-labor miss. The 2-year yield rose 4 basis points to 3.40%, the 5-year 4 basis points to 3.69%, the 10-year 4 basis points to 4.28%, and the 15-year 4 basis points to 4.65%. The uptick blended resource resilience with offshore Treasury pressure, as August’s 5.4 thousand job loss—versus 21.5 thousand expected—held 4.2% unemployment but signaled softening, amplifying November cut odds at 80% despite potential 2.9% CPI YY rise from 2.8%.

Macro ties include tariff pass-through risks mirroring FedEx’s $1 billion hit, per import prices at 0% YY, complicating RBA amid middling growth per BI models yielding tepid equity returns. The AUD’s 0.04% slip to 0.6591 reflects dollar rebound, though gold’s $3,747 record bolsters miners.

Overview of the US Bond Market

US Treasuries dipped on September 22, 2025, with yields edging higher amid tech-led equity highs and tariff jitters, ahead of Friday’s PCE eyed for easing room as volatility nears yearly lows despite geopolitics. The 2-year yield rose 3 basis points to 3.60%, the 5-year 6 basis points to 3.70%, the 10-year 11 basis points to 4.15%, and the 30-year 11 basis points to 4.76%. Pressure mounted pre-auctions and inflation gauge, forecast at 0.2% core MM—down from 0.3%—per TD’s Munoz on tariff goods creep and services moderation.

Weaving macro, FedEx’s $1 billion volatility warning underscores trade war earnings drags, echoing resilient yet middling BI growth at 0.5—historically 4% S&P returns versus recessionary 13%. Prior jobless drop and Philly surge affirm labor stability, but Miran’s tight policy risk contrasts Musalem’s limited cuts on 2.9% core YY hold. Hammack’s caution ties to overheating fears amid Trump’s “run it hot.” JPM surveys show longs low, asset managers trimming $23.5 million per basis point in 5-10 year futures, CFTC leveraged shorts pared $5-6.5 million; swaps under 50 basis points year-end. BofA elevates geopolitics—Russia, Gaza, Taiwan—yet markets unfazed unless oil or bonds spike, per BlackRock’s Jewell on earnings quantification. Auctions unchanged Q4 per Treasury, EU/Japan deals easing uncertainty for higher rates under Trump-Powell.