| Close | Previous Close | Change | |

|---|---|---|---|

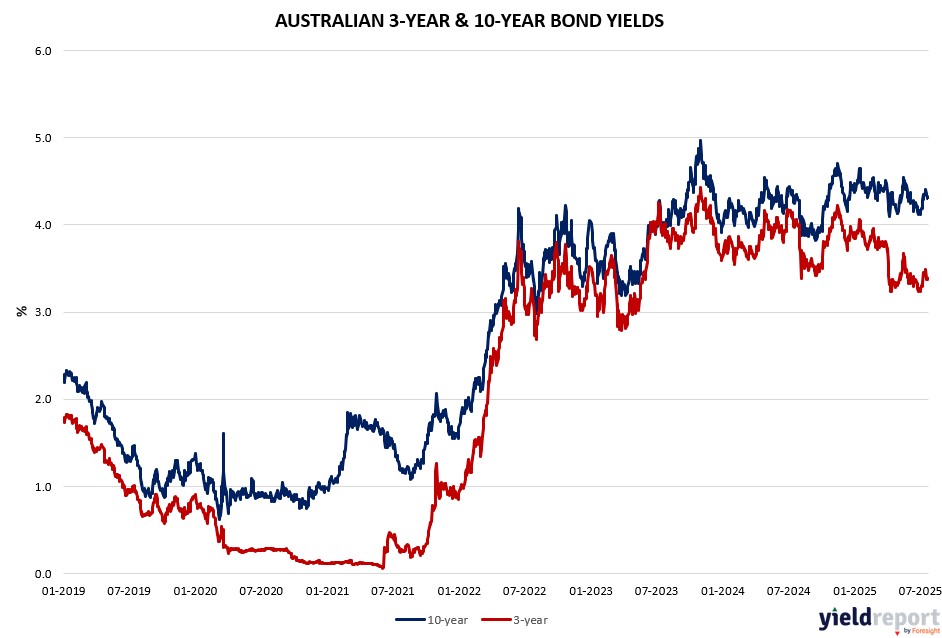

| Australian 3-year bond (%) | 3.384 | 3.369 | 0.015 |

| Australian 10-year bond (%) | 4.305 | 4.308 | -0.003 |

| Australian 30-year bond (%) | 5.027 | 5.006 | 0.021 |

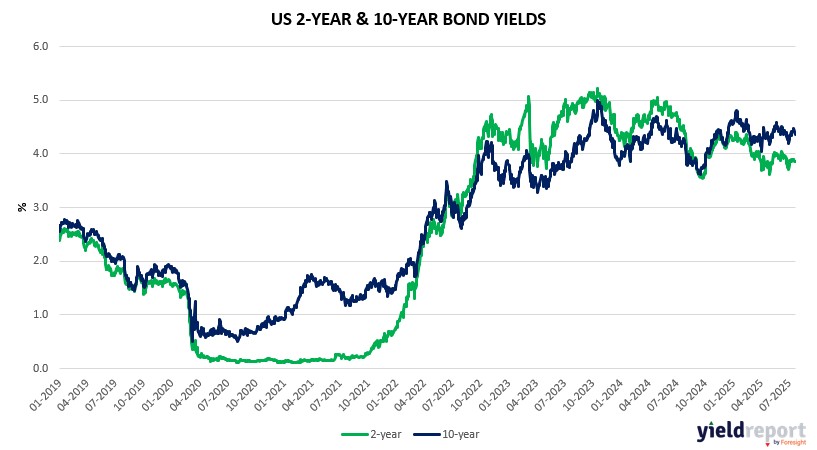

| United States 2-year bond (%) | 3.853 | 3.867 | -0.014 |

| United States 10-year bond (%) | 4.378 | 4.394 | -0.016 |

| United States 30-year bond (%) | 4.9512 | 4.9626 | -0.0114 |

Overview of the Australian Bond Market

Australian 10-year Treasuries rose for a third day as the market absorbed today’s ASX gains and awaited key data, with the yield ticking up 2 basis points to 4.32%. The 2-year yield climbed 4 basis points to 3.37%, reflecting short-term rate sensitivity, while the 5-year yield rose 3 basis points to 3.71%. The 15-year yield increased 3 basis points to 4.69%, supported by a steeper yield curve amid global trade developments.

Yields have edged higher over the past month, with the 10-year up 11 basis points, driven by optimism from China’s infrastructure push and softer domestic employment data (unemployment at 4.3%) reinforcing an 85-basis point rate cut expectation over the year, targeting 3.02% by mid-2026. The August cut to 3.68% holds at 94%. Yesterday’s composite leading index, down 0.03% and PMI flash data (manufacturing 51.6, services 53.8) signal modest growth, tempering aggressive easing bets.

Interest-rate swaps remain stable, with the 10-year yield’s rise blending domestic resilience with global caution ahead of US data. Today’s strong PMI flash for Jun could shift yields, especially with the Japan-US trade deal and potential EU progress reducing tariff fears. The AUD’s 0.15% gain to 0.6565 reflects this optimism, though focus remains on the August 1 deadline.

Overview of the US Bond Market

Treasury 10-year yields rose four basis points to 4.39%. Bonds remained lower even after a strong $13 billion sale of 20-year securities that tested the appetite for long-maturity debt. Japan’s 40-year government bond auction saw its weakest demand since 2011.

Bond traders are boosting bets that the Federal Reserve will cut interest rates more aggressively next year, as speculation mounts that an eventual change of leadership at the central bank will deliver the easier monetary policy that President Donald Trump is demanding.

The U.S.-Japan trade deal spurs risk appetite and Treasury sell off, putting yields on pace to snap a three-day decline. The U.S. will levy 15% tariffs on Japanese goods. President Trump says Japan will also invest $550 billion in America. Trade talks have been driving markets in the absence of major U.S. indicators. June existing home sales data are due at 10 a.m. ET and expected to contract, in a WSJ survey. Weekly jobless claims tomorrow are forecast to accelerate a little. The 10-year is at 4.376% and the two-year at 3.853%.

The shift shows how traders are increasingly convinced that a successor to Powell — whose term ends in May 2026 — will fall in line with the president’s demands for lower rates. While Trump last week quickly walked back threats to fire the Fed chief after they sparked a brief spasm in markets, investors appear to have latched onto the idea that he will succeed in bending the central bank to his will.

Powell has been under fire from Trump and his allies for holding back on rate reductions due to concern over the inflationary impact of the administration’s tariff hikes. A number of Republicans this month have also taken issue over a costly renovation of the central bank’s buildings.

Potential candidates to replace Powell, including Kevin Hassett and Kevin Warsh, have all voiced their support for lower rates. Two Republican-appointed Fed governors — Christopher Waller and Michelle Bowman — have also signaled their openness to cutting rates as early as at the July 29-30 policy meeting.

While traders see zero chance for a rate cut next week, futures tied to the fed funds rate are reflecting a 58% probability for a 25-basis point cut in September as of Wednesday.