BOND_23.05.25.csv

| Close | Previous Close | Change | |

|---|---|---|---|

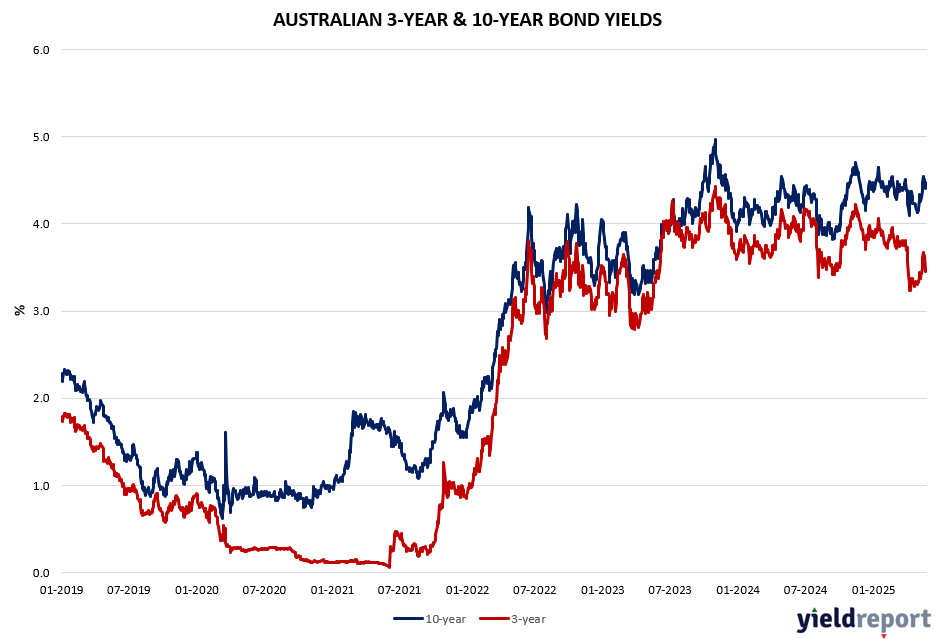

| Australian 3-year bond (%) | 3.489 | 3.492 | -0.003 |

| Australian 10-year bond (%) | 4.453 | 4.477 | -0.024 |

| Australian 30-year bond (%) | 5.159 | 5.171 | -0.012 |

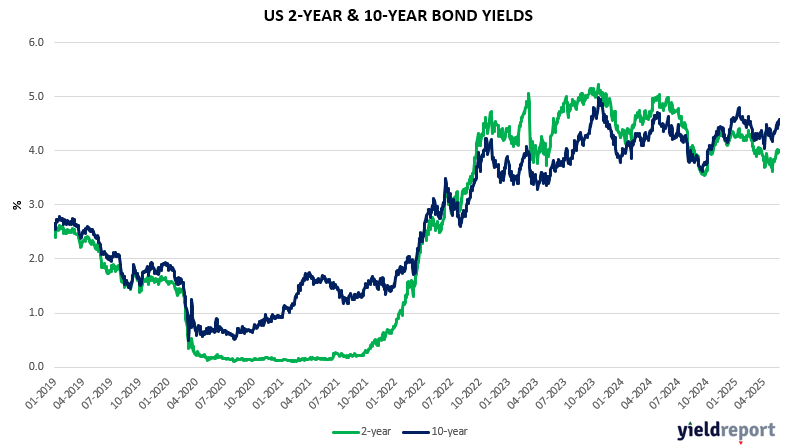

| United States 2-year bond (%) | 3.985 | 4.005 | -0.02 |

| United States 10-year bond (%) | 4.531 | 4.581 | -0.05 |

| United States 30-year bond (%) | 5.0395 | 5.0827 | -0.0432 |

Overview of the Australian Bond Market

Australia’s 10-year government bond yield held its recent decline to around 4.41% on Friday amid growing expectations of more policy easing by the RBA in addition to a return to relative calm in the US Treasuries market after the ructions on Wednesday.

Obviously on Tuesday, the RBA cut its cash rate by 25bps to a two-year low of 3.85%, but the RBA also indicated a willingness to cut rates again if the economic outlook deteriorates sharply. Currently, markets are implying a better than 50% chance that the RBA will lower rates again at its next meeting in July, up from less than 20% a week ago, with rates now seen to bottom at 3.1% rather than 3.35%.

On the economic data front this week, the monthly CPI for April (Wednesday) and Retail Sales (Friday)will be the most important releases for the local bond market.

Overview of the US Bond Market

US government debt held onto slight gains after Treasury Secretary Scott Bessent said that plans for deregulation were gaining momentum. The advance on Friday pushed yields down by one to two basis points across maturities after Bessent said that an easing of bank capital rules on Treasuries could happen this summer. US Treasury Secretary Scott Bessent says a shift in the supplementary leverage ratio could bring yields down by tens of basis points. The US 10-year Treasury note eased 2 bps to 4.53%. The US 30-year Treasury note was largely unchanged at 5.04%.

Friday’s move caps a week in which long-dated yields globally soared on investor concern about widening fiscal deficits in the US and abroad. The 30-year yield is trading near 5.03%, compared to the 4.9% seen before Moody’s Ratings stripped the US of its last top credit score a week ago. Whether he succeeds in calming the bond market, however, will come down to the fundamentals of demand and supply for long-end Treasuries – which is an open question — and the economic outlook.

Meanwhile, the US economic / budget deficit outlook is fueling hedging activity in longer end Treasury options. Plays favoring the 10-year yield testing 5% are among some of the bigger positions. Given trade and monetary policy uncertainty amid a structural shift in the demand landscape, the risks are skewed toward bearish steepening over the near term. Premiums to protect against bigger losses on the long-end of the Treasury curve are now at their highest level since April. The current move in options skew means that traders are driving up the price of puts that hedge against the risk of a yield spike, relative to call options that would profit from the opposite.

The markets are closed on Monday for the Memorial Day holiday but otherwise it will be a relatively busy week on the economic data front. Last week was a particularly quiet week in the US regarding economic data, which may partly explain the very high focus on all things related to the budget deficit. This week is different. On Tuesday Consumer Confidence and Durable Goods is released. On Wednesday the FOMC Minutes will be released. On Thursday and Friday, GDP data will be released, Jobless Claims, and the all-important PCE inflation print