| Close | Previous Close | Change | |

|---|---|---|---|

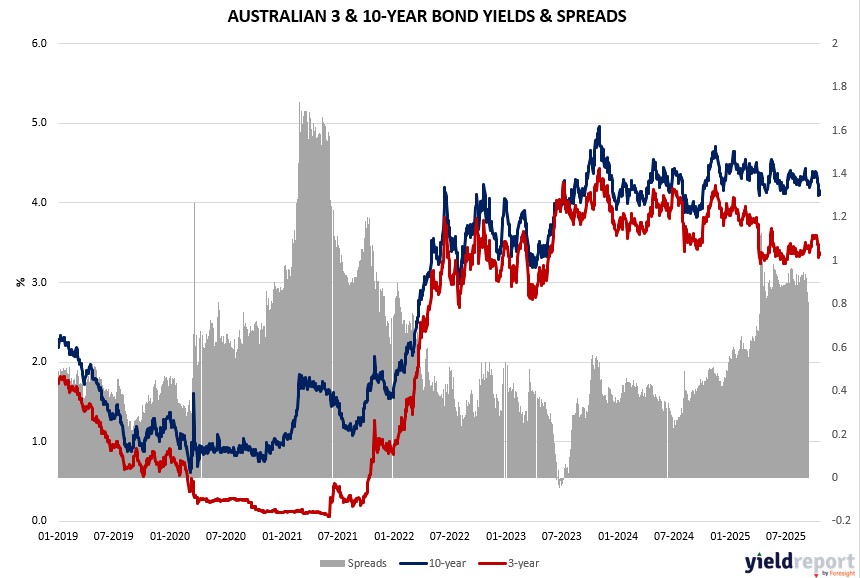

| Australian 3-year bond (%) | 3.367 | 3.35 | 0.017 |

| Australian 10-year bond (%) | 4.129 | 4.112 | 0.017 |

| Australian 30-year bond (%) | 4.811 | 4.795 | 0.016 |

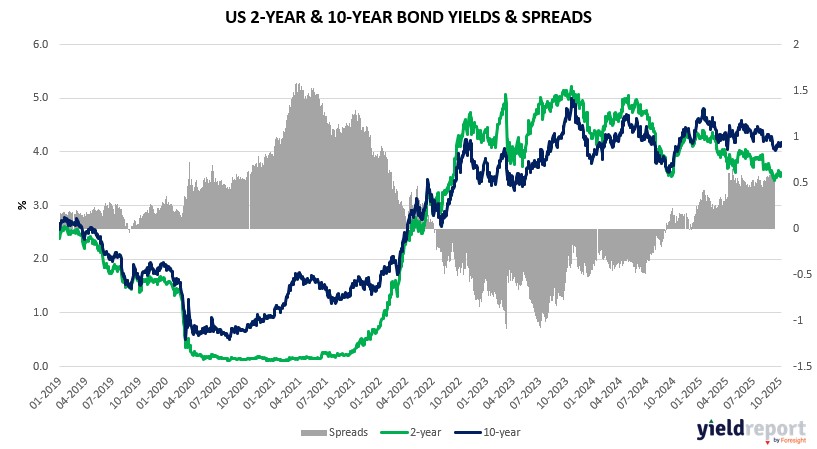

| United States 2-year bond (%) | 3.463 | 3.455 | 0.008 |

| United States 10-year bond (%) | 3.989 | 3.957 | 0.032 |

| United States 30-year bond (%) | 4.5749 | 4.5391 | 0.0358 |

Overview of the Australian Bond Market

Australian government bond yields rose on October 23, 2025, with the 10-year up 5 basis points to 4.15%, tracking US climbs on oil’s inflation implications, though AUD/USD little changed at 0.6487 capped upside. Shorter 2-year added 5 basis points to 3.36%, reflecting PMI softness, while 15-year gained 5 basis points to 4.49% amid global risk-on from trade thaws.

Macro blends included manufacturing PMI dip to 49.7—contraction after expansion—offset by services rise to 53.1, keeping composite at 52.6, highlighting uneven recovery per S&P Global. Positioning sensitive to US CPI poll 0.3% core monthly tomorrow, where hotter print risks yield pressure amid tariff passthrough, as Principal notes temporary cushions like inventory frontloading may wane. Dealers anticipate steady auctions, with RBA eyeing Fed dovishness spillover.

Oil gluts aiding disinflation could support bonds if PMIs signal broader slowdown, blending with NAB’s consumer stress return and China stimulus hopes lifting metals.

Overview of the US Bond Market

Treasury yields climbed on October 23, 2025, with the 10-year up 6 basis points to 4.00%, as oil’s surge on Russia sanctions spurred inflation bets ahead of CPI, though equity gains and trade thaw limited rises. Shorter ends like the 2-year rose 5 basis points to 3.49%, reflecting caution on sticky prices, with 30-year yields adding 5 basis points to 4.58% amid macro uncertainties from the shutdown’s data gaps.

Blended factors included existing home sales at 4.06 million—hitting poll and a seven-month high—signaling housing resilience, yet labor fragility per Goldman Sachs’ low payroll trends underscores Fed’s easing bias despite core CPI stuck above 3% for years. Positioning via delayed CFTC showed asset managers trimming longs, concentrated in shorter tenors, while JPMorgan’s scenarios peg 65% chance of S&P advance post-CPI, viewing tail risks needed to sideline October 29 cut. Dealers expect steady auction sizes November-January, as BMO’s Ian Lyngen notes murky oil sanction fallout, with kneejerk crude spikes dominating attention.

Upcoming October 24 core CPI poll at 0.3% monthly could greenlight easing if not hotter, per Bloomberg preview, though Seema Shah flags tariff passthrough risks persisting into 2026, potentially forcing cautious Fed amid inventory depletion and margin squeezes. With oil gluts possibly hitting $55 by year-end per Eurasia, aiding disinflation, bonds may stabilize if data aligns with fragile jobs narrative.