| Close | Previous Close | Change | |

|---|---|---|---|

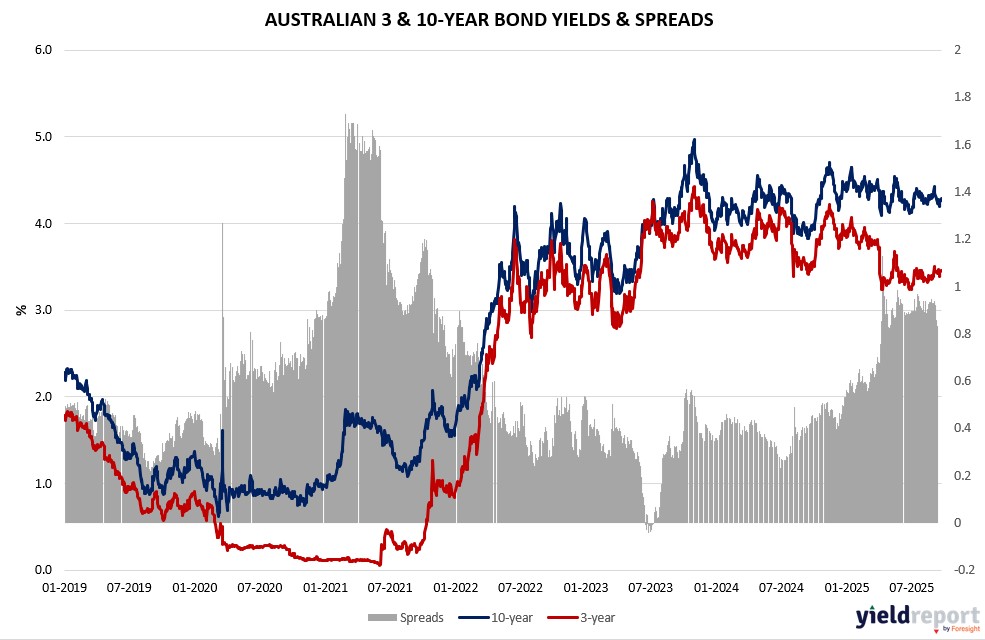

| Australian 3-year bond (%) | 3.459 | 3.46 | -0.001 |

| Australian 10-year bond (%) | 4.271 | 4.284 | -0.013 |

| Australian 30-year bond (%) | 4.999 | 5.027 | -0.028 |

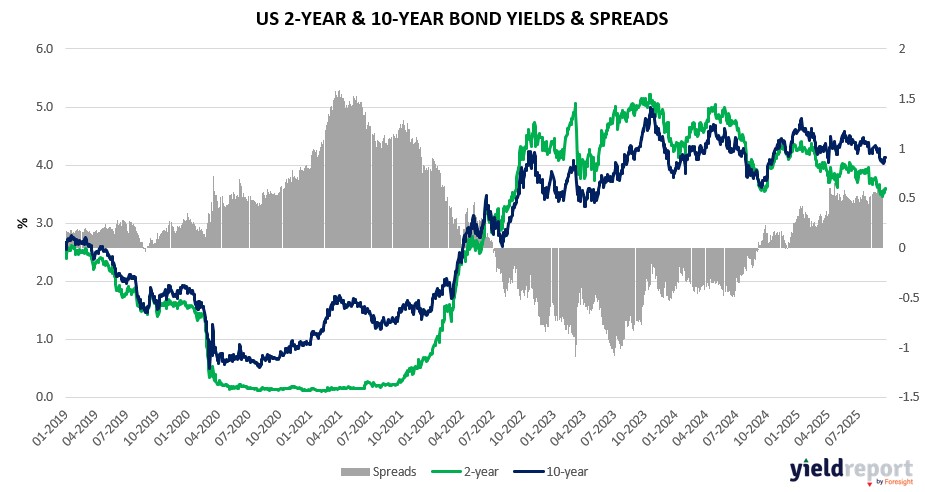

| United States 2-year bond (%) | 3.599 | 3.576 | 0.023 |

| United States 10-year bond (%) | 4.131 | 4.131 | 0 |

| United States 30-year bond (%) | 4.7507 | 4.7507 | 0 |

Overview of the Australian Bond Market

Australian government bond yields held steady to slightly lower on September 23, 2025, as markets braced for Wednesday’s CPI, expected at 2.9% YY, amid commodity strength and global yield dynamics. The 2-year yield was flat at 3.38%, the 5-year unchanged at 3.67%, the 10-year steady at 4.26%, and the 15-year down 1 basis point to 4.63%. Stability reflects caution post-PMI slowdown—manufacturing at 51.6, services 52—versus prior 53 and 55.8, with August’s labor miss of 5.4 thousand jobs fueling RBA easing bets.

Macro blends include tariff risks mirroring US warnings, with import prices at 0% YY complicating RBA’s stance amid middling growth, per BI models. Gold’s $3,764 record supports miners, while the AUD’s 0.14% dip to 0.6591 tracks dollar resilience. CPI upside could temper November cut odds.

Overview of the US Bond Market

US Treasuries gained slightly on September 23, 2025, with yields dipping after a four-day climb, as markets await Friday’s PCE data and parse Powell’s neutral stance on cuts amid tariff and labor concerns. The 2-year yield fell 1 basis point to 3.59%, the 5-year 3 basis points to 3.67%, the 10-year 4 basis points to 4.11%, and the 30-year 4 basis points to 4.72%. The pullback reflects caution before PCE, forecast at 0.2% core MM—easing from 0.3%—offering Fed room to address labor softening, per TD Securities’ Oscar Munoz on tariff pass-through and services moderation.

Macro factors include FedEx’s $1 billion tariff hit warning, echoing 0% import price YY, with resilient growth per Bloomberg Intelligence’s 0.5 reading signaling tepid 4% S&P returns versus 13% in recessions. Powell’s labor focus, per Dutta, contrasts Bostic’s inflation concerns, while Bowman pushes aggressive cuts. JPMorgan’s survey shows net longs at two-month lows, with asset managers trimming $23.5 million per basis point in 5-10 year futures, CFTC data indicating leveraged shorts cut by $5-6.5 million. Swap contracts hold under 50 basis points of year-end easing. Geopolitical risks—Russia, Gaza, Trump’s policies—remain muted unless oil spikes, per BlackRock’s Helen Jewell, with EU/Japan deals reducing uncertainty. Treasury auctions stay steady per April guidance, supporting higher rates under Trump-Powell dynamics.