| Close | Previous Close | Change | |

|---|---|---|---|

| Australian 3-year bond (%) | 3.392 | 3.434 | -0.042 |

| Australian 10-year bond (%) | 4.313 | 4.391 | -0.078 |

| Australian 30-year bond (%) | 4.984 | 5.076 | -0.092 |

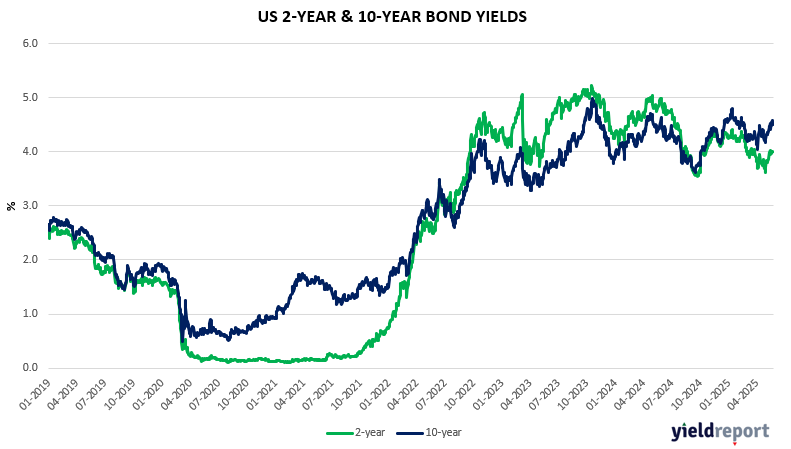

| United States 2-year bond (%) | 3.985 | 3.987 | -0.002 |

| United States 10-year bond (%) | 4.465 | 4.511 | -0.046 |

| United States 30-year bond (%) | 4.9696 | 5.037 | -0.0674 |

Overview of the Australian Bond Market

The yield on the Australian 10-year government bond yield fell to below 4.32% on Tuesday, its third consecutive session of decline and tracking bond yields from G10 economies amid signs that Japan may curb its bond issuance. Japanese authorities signaled they might lower their debt plan to halt the selloff in its bonds after poor auctions for long-dated JGBs drove the yield on the key 30-year bond to a record high.

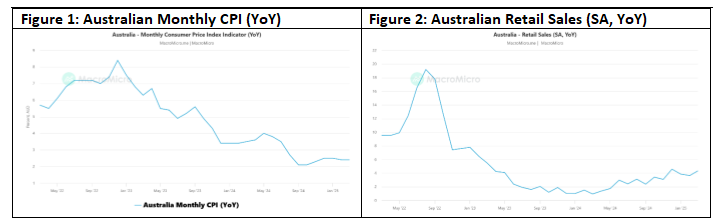

Domestic investors await domestic economic releases later this week. The upcoming data, including Wednesday’s monthly CPI indicator and Friday’s retail sales figures, are expected to provide crucial insights into inflation trends and consumer spending, as both are key factors in the Reserve Bank of Australia’s policy outlook.

Markets are now pricing in a 65% probability of another rate cut in July, with expectations of a total 75 bps of easing by the first quarter of 2026. Additionally, the country’s financial markets have a pretty firm view about where interest rates will go – down to 3.1% by the end of the year, where they will remain for at least six months. That’s three quarter-point rate cuts from the RBA.

As per a BondAdivisor report and as reported last week, the A$ Tier 2 market (all being floating rate notes) continued its hot streak last week with Macquarie Bank hitting the market with a dual-tranche FRN transaction last Thursday (22-May). Both legs were met with substantial demand, with the tranches pricing 20bps and 30bps inside IPG respectively. However, the latter of the 2 issues (a fixed to FRN) stole the show with a $4.4bn final orderbook – equating to coverage of almost 6x. This marks the second largest orderbook for an A$ Tier 2 instrument in the past 12 months, only outdone by ANZ’s transaction in July 2024 at $4.7bn (2.5x coverage on $1.9bn deal size). BondAdvisor noted that the instrument has since tightened ~20bps in

the grey market, with the cash price popping above $101. Unsurprisingly, Westpac has quickly followed suit, announcing its own Tier 2 issuance which was due for pricing yesterday.

Overview of the US Bond Market

Global bonds rallied, with US Treasuries leading gains, on signs that Japanese authorities may adjust debt sales following a rout in the market. Long-dated debt led the move, with the 30-year US yield falling as much as 9 bps to 4.95% as the market reopened after a holiday. In Japan, similar yields fell more than a

massive 20 bps. European bonds also rallied. Japanese authorities signaled they are considering adjusting their debt plan after a selloff that drove the nation’s long-term borrowing costs to the highest levels in decades. Worries about the ability of governments to cover massive budget deficits weighed on developed-market debt in recent days, pushing long-dated US yields toward levels last seen in 2007. The US 10-year Treasury note fell by nearly 7 bps to 4.44%.

That potential lower issuance is supporting Treasuries. For those seeking to buy long-term debt, lower Japanese government bond supply could force such investors into the Treasury complex. Japan’s finance ministry sent a questionnaire to market participants on Monday evening asking for their views on issuance and the current market situation. It was an unusual move and traders took it as a sign that authorities are seeking to stabilize rout in long-dated bonds. Some other governments have already shifted issuance toward shorter-dated tenors. The UK has been steering away from longer bonds given falling investor demand.

On the topic of shorter-dated tenor, the moves in the US extended after a $69 billion auction sale of two-year Treasuries was met with solid bidding metrics. But the shorter-end of the curve certainly isn’t the issue. Quite the contrary.

The chance that Japan’s government will reduce its bond supply goes at least some way to addressing the worries over demand. But it doesn’t address wider concerns about government finances globally, raising the possibility that Tuesday’s bond rally is only a brief pause in the tumult. Japan’s bond market has also been squeezed by signs that the central bank may attempt to taper its huge holdings of government bonds further. Long-end yields are experiencing some relief, but US yields may find it particularly difficult to shake off a bearish taint over the coming weeks and months as fiscal trajectory still matters.

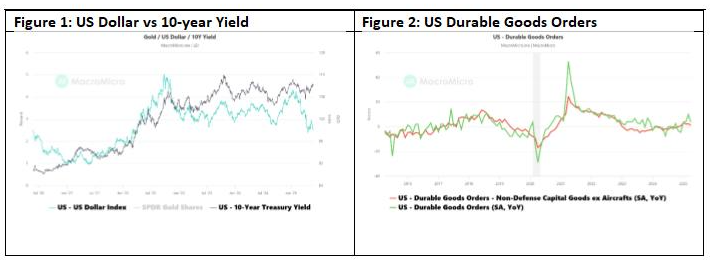

Meanwhile on the murky world of US economic data currently and what to make of it. Bookings for all durable goods — items meant to last at least three years — fell 6.3%, on a pullback in orders for commercial aircraft. The report underscores caution among businesses as they assess the outlook for demand and focus on cost-cutting in the wake of Trump‘s trade policy. The value of core capital goods orders, a less-volatile proxy for investment in equipment that excludes aircraft and military hardware, decreased 1.3% last month – substantially worse than expected.

Conversely, US consumer confidence rebounded sharply in May from a near five-year low as the outlook for the economy and labor market improved amid a truce on tariffs. The Conference Board’s gauge of confidence increased by 12.3 points to 98, marking the biggest monthly gain in four years. The figure exceeded all estimates of economists. The cutoff for the survey was May 19, after the US and China agreed to temporarily reduce high levies on each other’s goods while they negotiate a trade deal. About half the responses were collected after the agreement was reached on May 12.

The gauge’s improvement may be an indication that worries about tariffs — a key source of anxiety in the previous surveys — abated in recent weeks. This is likely a slightly confused survey result given timing issues noted above. Friday’s personal consumption expenditures (Core PCE) price index will provide greater clarity on what consumers are actually doing rather than simply saying what they think.

Views of the present job market were more mixed, however. While more respondents said jobs were plentiful in May, there was also a larger share that said jobs were currently hard to get. The difference between these two — a metric closely followed by economists to gauge the job market — narrowed for a fifth month.

US bond investors are now looking ahead to auctions of two-, five- and seven-year debt this week, as well as the release of the Federal Reserve meeting minutes, economic growth and inflation data.

Regarding Figure 1, if there is one chart that portrays de-dollarisation and repatriation of capital out of the US it is this one. Note the marked break between US 10-year treasury yields and the US Dollar index over the last few months.