| Close | Previous Close | Change | ||

|---|---|---|---|---|

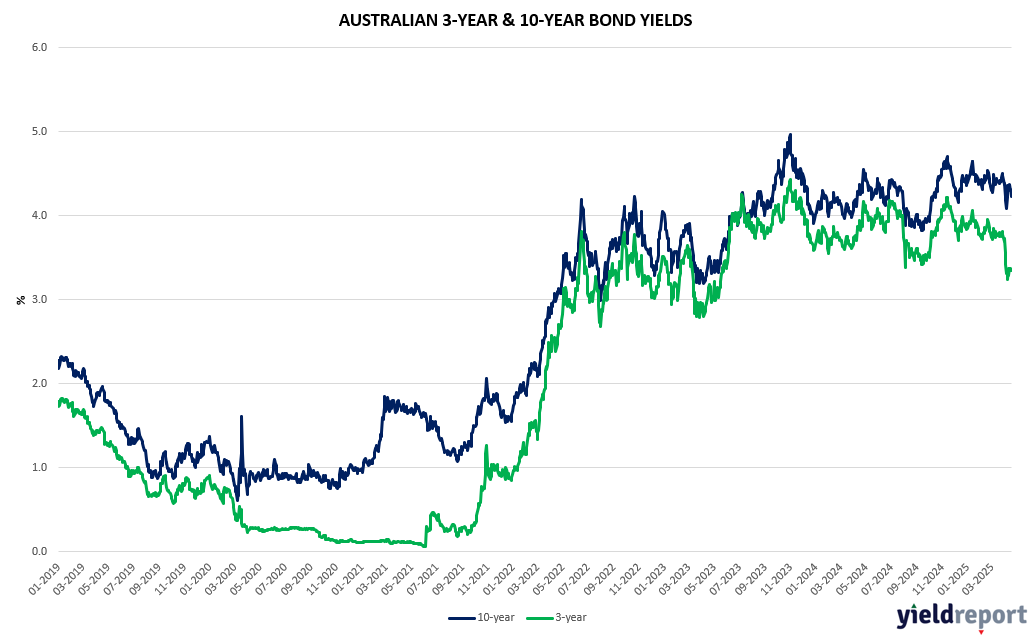

| Australian 3-year bond (%) | 3.308 | 3.339 | -0.031 | |

| Australian 10-year bond (%) | 4.135 | 4.2 | -0.065 | |

| Australian 30-year bond (%) | 4.863 | 4.935 | -0.072 | |

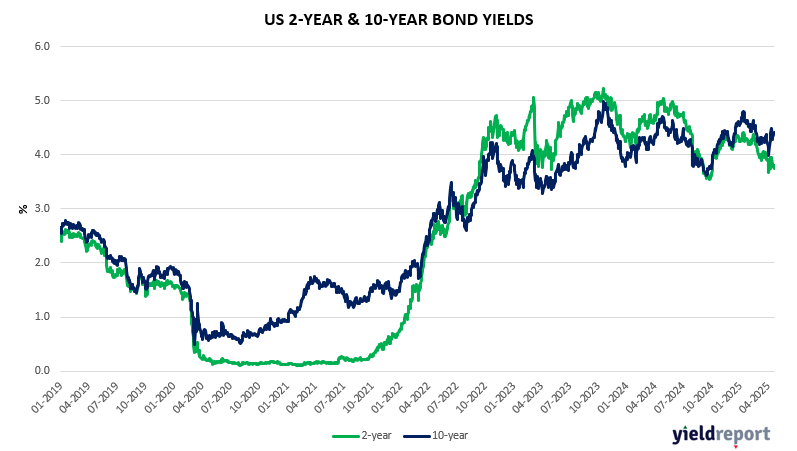

| United States 2-year bond (%) | 3.685 | 3.762 | -0.077 | |

| United States 10-year bond (%) | 4.216 | 4.266 | -0.050 | |

| United States 30-year bond (%) | 4.693 | 4.738 | -0.045 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield fell to around 4.15%, approaching a three-week low, as investors braced for key economic releases this week that could provide insights into future monetary policy.

Investors are now awaiting Australia’s upcoming CPI and PMI data for further insight into the domestic economic outlook. Both equities and bond markets will be particularly focused on the quarterly CPI figure on Wednesday. The markets are expecting the RBA to cut in May. But next month’s cut is predicated on official consumer price data to be released this week, highlighting the importance of Wednesday’s report. The market consensus is for inflation to tick up 0.8% in the three months to March 31, pushing the annual pace from 2.4% to 2.3%. More crucial is the core inflation measure, which strips out the most extreme moves. That is expected to increase 0.7%, taking the annual inflation rate watched by the RBA from 3.2% to 2.9%.

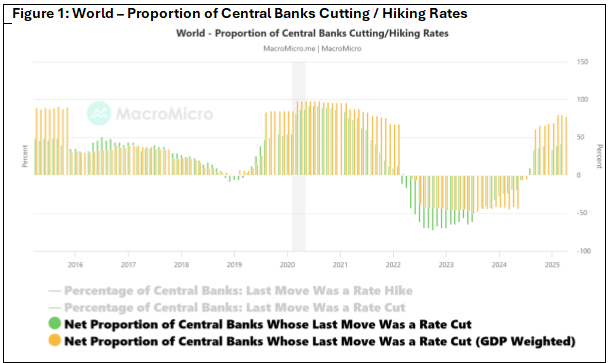

Should the RBA cut in May, the chart below simply shows it will play catch up with the vast majority of the world central banks. But we all know the dynamics that has led to the RBA beginning ‘late’ in starting with rate cuts.

US BOND MARKETS

The yield on the US 10-year Treasury note held steady around 4.24% on Monday, as investors braced for key economic reports this week that could provide insight into the early effects of President Donald Trump’s tariffs.

It is a big week on the macro data front. Markets are focused on Friday’s April jobs report, along with first-quarter GDP figures and the Fed-preferred PCE inflation gauge on Wednesday. Weaker-than-expected data could bolster expectations for earlier interest rate cuts by the Federal Reserve, with markets currently pricing in a 25-basis-point cut in June and anticipating a total of three cuts by year-end.

We note that several houses are bullish on US Treasuries and/or high yield corporate bonds. Pimco says Treasuries are starting to look attractive after the recent rout. Pimco have stated markets have foucsed on the risk that foreigners might reduce allocation to US holdings but not assigning as much probability to a scenario that growth will be weak, i.e likely pending rate cuts. Pimco stated that treasuries start to look quite attractive in the five to 10-year point.

Meanwhile, JP Morgan is bullish on high yield corporate bonds, note the significant increase in spreads recently (lower valuations) as well as the fact that the high yield market has increased in quality over the past 10-15 years. It notes that High yield has matured over the past 10 – 15 years into a market with a larger proportion of BB-rated bonds, increased secured debt issuance, lower duration (roughly 1.4 years lower since 2007) and far more conservative use of proceeds.