| Close | Previous Close | Change | |

|---|---|---|---|

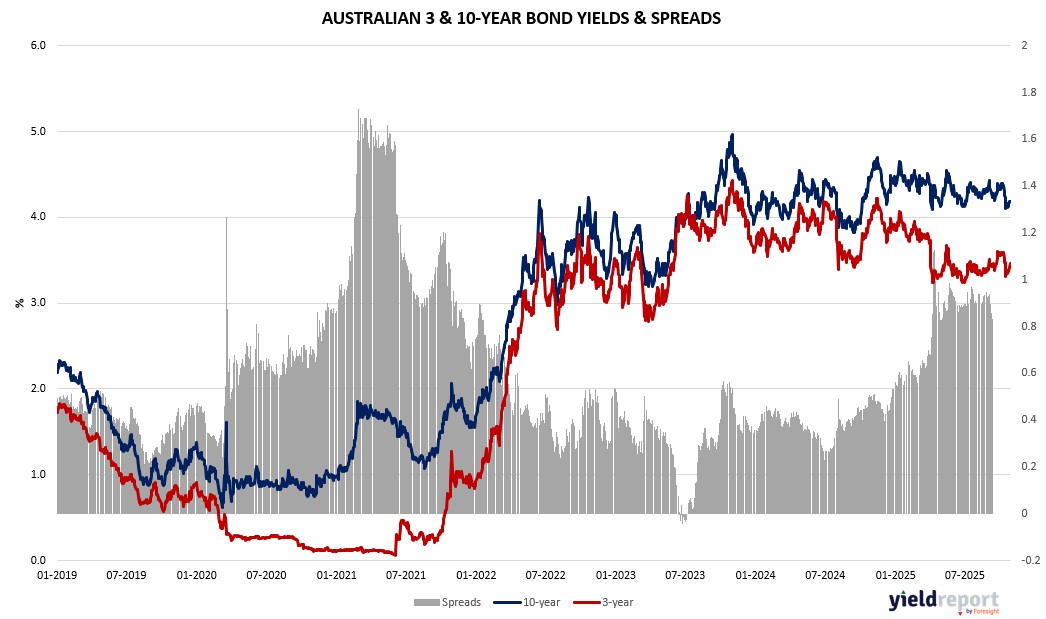

| Australian 3-year bond (%) | 3.458 | 3.416 | 0.042 |

| Australian 10-year bond (%) | 4.179 | 4.189 | -0.01 |

| Australian 30-year bond (%) | 4.856 | 4.882 | -0.026 |

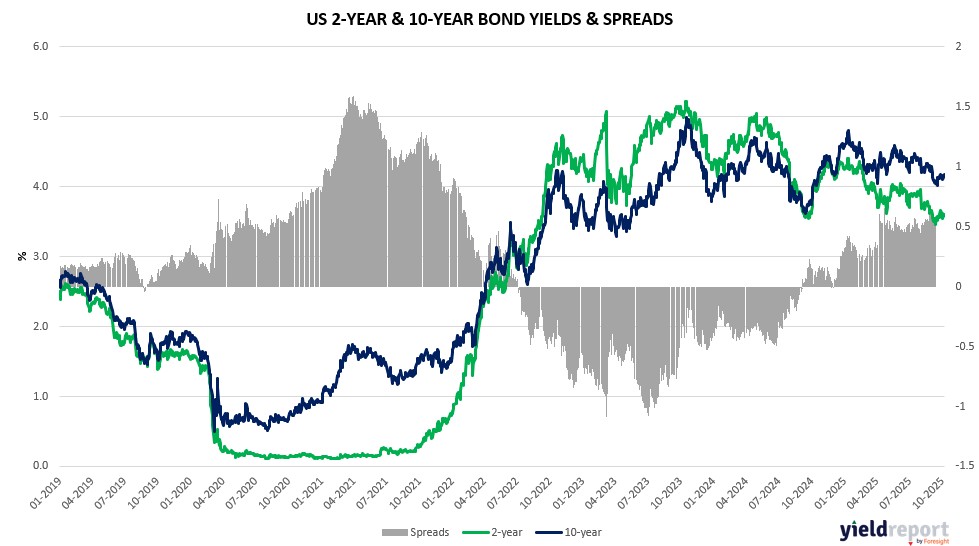

| United States 2-year bond (%) | 3.49 | 3.503 | -0.013 |

| United States 10-year bond (%) | 3.981 | 4.028 | -0.047 |

| United States 30-year bond (%) | 4.5531 | 4.6157 | -0.0626 |

Overview of the Australian Bond Market

Australian government bond yields edged lower as markets braced for CPI data and global cues, with the 10-year yield down two basis points to 4.16% and the 2-year up four to 3.42%. The curve steepened slightly, reflecting caution on RBA policy amid persistent inflation. Third-quarter CPI headlines are eyed Wednesday, with 1.1% quarterly growth forecast potentially affirming no near-term cuts, following June’s 0.7%; trimmed mean at 0.8% could signal core pressures easing from 0.6%.

US-China tariff rollback talks and Trump’s Fed critique added cross-currency dynamics, supporting AUD/USD up 0.06% to 0.656. Retail shop prices fell for the first time since March, hinting at consumer softness, while upcoming retail trade and factory orders data test resilience. Dealers anticipate steady issuance, with focus on Fed’s rate path influencing RBA shadow.

Strategists at Janney Montgomery Scott warn of 5-10% correction risks by year-end despite overbought US lift, while Interactive Brokers’ Jose Torres sees S&P 500 momentum toward 7,000 if Fed, earnings, and trade align. Morgan Stanley maintains long-term bull views but flags stretched valuations if tariffs bite, urging diversification.

Overview of the US Bond Market

Bond traders trimmed positions in Treasuries ahead of the Federal Reserve’s meeting, as yields held steady amid bets on a rate cut and potential quantitative tightening signals. The 10-year Treasury yield was little changed at 3.97%, while the 2-year stayed at 3.48% and the 30-year dipped one basis point to 4.54%, flattening the 2s-10s curve slightly to +49 basis points. A solid consumer confidence reading hit a six-month low, underscoring labor market concerns, but private payrolls rose modestly, supporting expectations for measured Fed easing.

Treasury Secretary’s comments on extending US-China tariff talks added to cross-border optimism, potentially easing inflationary pressures from trade tensions. With the Fed’s benchmark at 4.125%-4.375% since last adjustment, markets price in a 25 basis-point cut Wednesday, followed by gradual reductions amid resilient growth. Upcoming data like third-quarter GDP advance on Thursday, expected at 3% annualized, and core PCE inflation Friday at 0.2% monthly, will test this view; stronger figures could temper easing bets.

JPMorgan’s client survey showed net long positions shrinking to two-month lows, reflecting caution before the FOMC, though swap contracts hold steady at under half a point of year-end cuts. Asset managers pared longs across tenors by $23.5 million per basis point in CFTC data through October 22, while leveraged funds reduced bond shorts. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance, with 10-year and 5-year reopenings up $1 billion each.

Strategists from UBS and Goldman Sachs maintain bullish equity outlooks but flag bond risks if tariffs or AI spending spur inflation, keeping yields elevated. HSBC notes economic resilience post-EU and Japan deals has bolstered higher-for-longer views, though Trump’s Fed criticism adds dissent risks. Oil’s 2.3% drop to $59.93 a barrel on supply glut fears outweighed Russia sanction worries, aiding disinflation bets.