| Close | Previous Close | Change | |

|---|---|---|---|

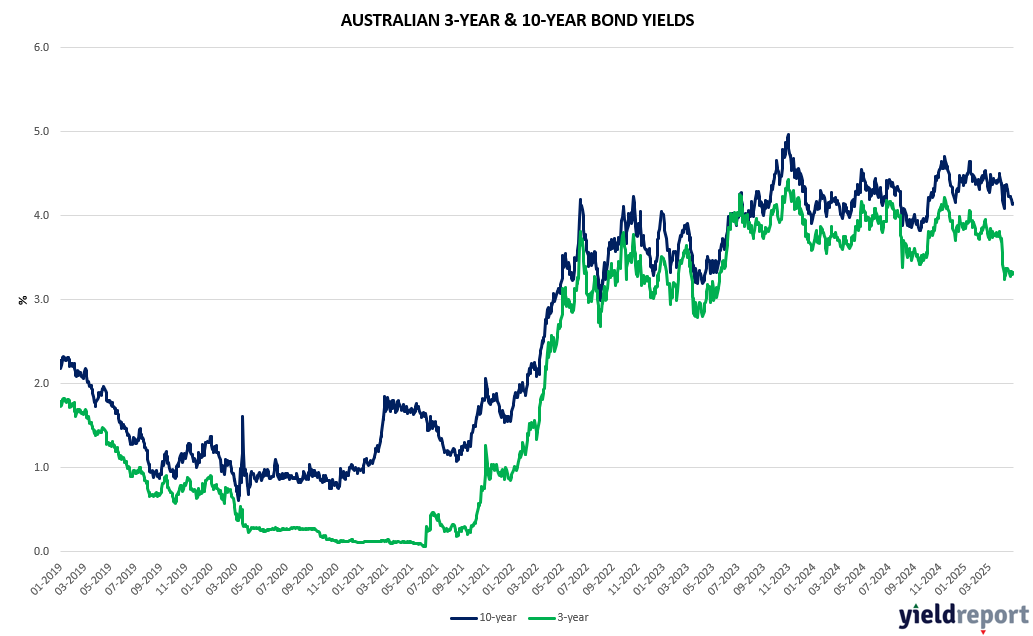

| Australian 3-year bond (%) | 3.324 | 3.308 | 0.016 |

| Australian 10-year bond (%) | 4.148 | 4.135 | 0.013 |

| Australian 30-year bond (%) | 4.875 | 4.863 | 0.012 |

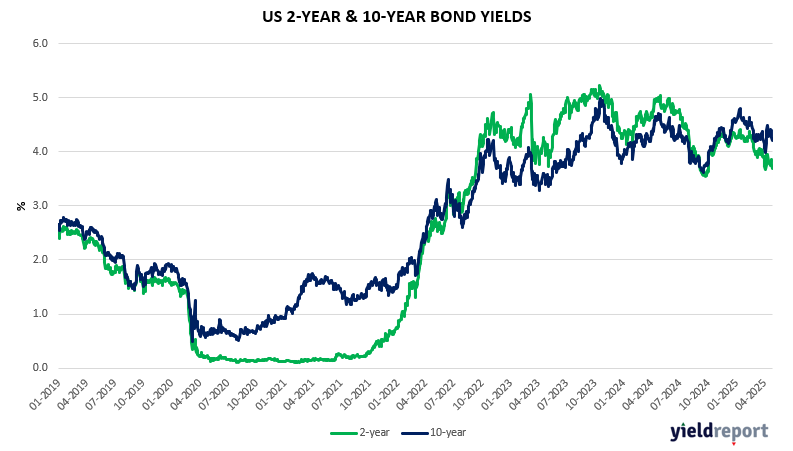

| United States 2-year bond (%) | 3.658 | 3.685 | -0.027 |

| United States 10-year bond (%) | 4.174 | 4.216 | -0.042 |

| United States 30-year bond (%) | 4.648 | 4.693 | -0.045 |

LOCAL BOND MARKETS

Australia’s 10-year government bond yield was up 4 bps to 4.19%. Despite today’s quarterly CPI print and expectations of cooling inflation (and subsequent RBA cuts) the rise in yields likely reflected the fact that on Monday S&P put Australia’s credit rating on notice.

S&P warned that Australia could be at risk of being downgraded if the Government pursues excessive, debt-funded public spending following the 2025 election. This reflects large spending commitments during the election campaign by both Labour and Liberal parties. Of note, the rating agency highlighted potential ‘off-budget’ spending of more than $100bn between 2025-29.

Australia has been rated AAA since 2003 by S&P. It is one of 11 countries to have been granted this status which filters through to the credit rating profiles of domestic banks. This means any adjustment to the sovereign credit rating could have a knock-on effect to the credit ratings of Australian banks.

In relation to today’s quarterly CPI print, the market consensus is for inflation to tick up 0.8% in the three months to March 31, pushing the annual pace from 2.4% to 2.3%. More crucial is the core inflation measure, which strips out the most extreme moves. That is expected to increase 0.7%, taking the annual inflation rate watched by the RBA from 3.2% to 2.9%.

US BOND MARKETS

The yield on the 10-year US Treasury note fell 4 bps to 4.2% on Tuesday, the lowest in three weeks, as the worsening macroeconomic backdrop strengthened bets that the Federal Reserve may be forced to deliver multiple rate cuts this year.

On the macro and sentiment survey front, the JOLTS showed that the US economy had 7.19 million job openings in March, well below expectations of 7.48 million, to challenge other labor reports that suggest a robust labor market. In the meantime, the leading indicators continued to show that economic policy uncertainty continued pressure sentiment, with the CB survey pointing to an aggressive increase in pessimism.

Rate futures reflect that the market has positioned for 100bps in cuts this year, despite the Fed’s warning that tariffs may be inflationary for US goods and services. In the meantime, the US Treasury increased its Q2 borrowing plans by more than expected, contrasting sharply with their signals of lower deficits in the Trump administration.

It is a big week on the macro data front. Markets are focused on Friday’s April jobs report, along with first-quarter GDP figures and the Fed-preferred PCE inflation gauge on Wednesday. Weaker-than-expected data could bolster expectations for earlier interest rate cuts by the

Federal Reserve, with markets currently pricing in a 25-basis-point cut in June and anticipating a total of three cuts by year-end.