| Close | Previous Close | Change | |

|---|---|---|---|

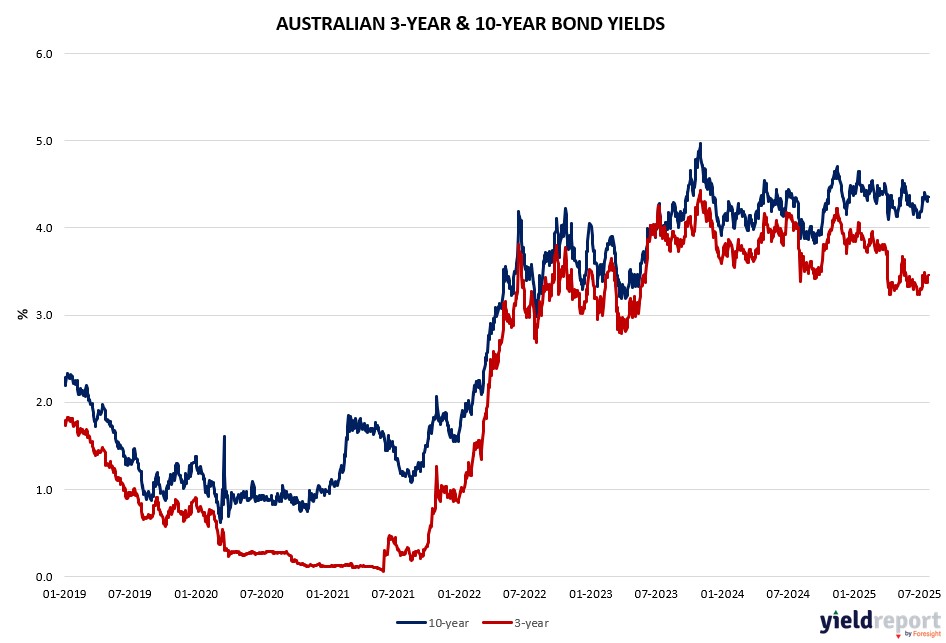

| Australian 3-year bond (%) | 3.43 | 3.454 | -0.024 |

| Australian 10-year bond (%) | 4.338 | 4.35 | -0.012 |

| Australian 30-year bond (%) | 5.052 | 5.506 | -0.454 |

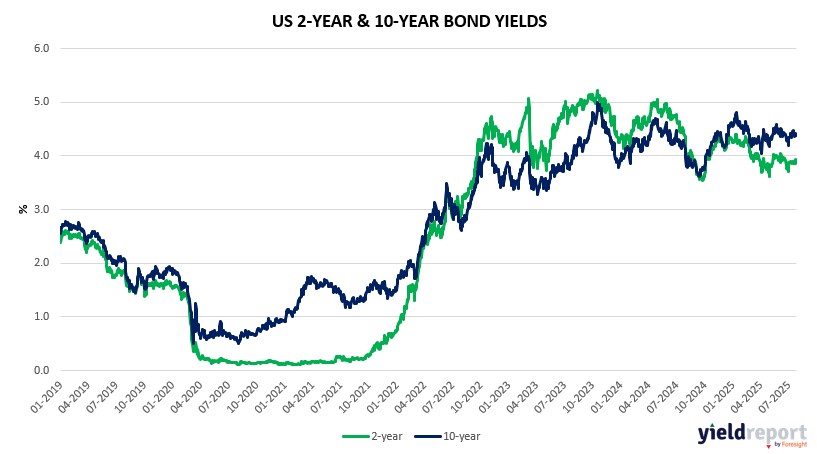

| United States 2-year bond (%) | 3.918 | 3.917 | 0.001 |

| United States 10-year bond (%) | 4.394 | 4.38 | 0.014 |

| United States 30-year bond (%) | 4.9337 | 4.9235 | 0.0102 |

Overview of the Australian Bond Market

Australian 10-year Treasuries dipped as markets braced for key inflation data, with the yield falling 5 basis points to 4.29%. The 2-year yield eased 5 basis points to 3.36%, while the 5-year yield dropped 6 basis points to 3.68%. The 15-year yield fell 5 basis points to 4.65%, reflecting a broader yield curve softening amid global caution.

Yields have risen over the past month, with the 10-year up 16 basis points, supported by PMI data (composite 53.6) but tempered by a -0.03% leading index. The RBA’s gradual rate-cut path, targeting 3.00% by mid-2026 with an 85-basis point reduction, remains in focus, though today’s CPI (expected 0.8% quarterly, 2.2% yearly) and trimmed mean (0.7% quarterly, 2.7% yearly) could shift expectations. The AUD’s 0.21% drop to 0.6507 signals tariff and commodity pressures.

Interest-rate swaps show a slight flattening, with yields reacting to US consumer confidence beating estimates at 97.2 and global trade tensions, reassured by the announcement of US-China tariff pause deadline extension in Stockholm this morning. Today’s Australian CPI data and US Q2 GDP advance will be critical.

Overview of the US Bond Market

Bond traders cut bets on Treasuries over the past week, as markets brace for a Federal Reserve meeting that is expected to shed light on how aggressively the central bank will lower interest rates in coming months.

A rally in Treasuries gained steam after a solid $44 billion sale. Longer-dated bonds led gains, with 30-year yields down 10 basis points ahead of the US announcement on the size of future debt auctions. Oil jumped as President Donald Trump reiterated the US may impose additional levies on Russia unless it reached a truce with Ukraine.

Treasury Secretary Scott Bessent said that the US and China will continue talks over maintaining a tariff truce before it expires in two weeks and that Trump will make the final call on any extension. Adding an extra 90 days is one option, Bessent said.

On the economic front, US consumer confidence increased as concerns eased about the outlook for the broader economy and the labor market. While job openings fell, they hovered at a level that indicates generally stable demand for workers.

JPMorgan Chase & Co.’s weekly Treasury client survey showed net long positions shrank to the smallest in two months ahead of Wednesday’s meeting. That suggests investors are less bullish overall, though market-implied expectations for Fed policy have remained steady, with swap contracts pricing in just under half a percentage point of easing by year-end beginning as early as September.

The shift comes as countervailing factors cloud the outlook for Fed policy over the medium-term. Fed Chair Jerome Powell is under pressure from President Donald Trump to lower borrowing costs and may face dissent this week from other central bank officials. Bond yields have edged lower over the past week, while futures tied to the Fed policy rate show traders pricing in a roughly 60% chance of a 25 basis-point cut in September.

At the same time, the resilience of the US economy in the face of Trump’s trade war has bolstered the bearish view, which sees Treasury prices under pressure as interest rates remain higher for longer. Deals signed in recent days with the European Union and Japan have also dissipated uncertainty, strengthening the case for the Fed to keep borrowing costs elevated.

In the cash market, JPMorgan’s client survey in the week to July 28 found fewer longs and the most shorts since June 2; neutrals were unchanged. The net long position was the smallest since May.

Asset managers cut positions across Treasury futures for a second straight week, according to the latest CFTC data for the reporting period ended July 22. Meanwhile, leveraged funds and speculators pared their net short positions in the classic Bond contract. Asset managers pared their net long positions across Treasury tenors by a combined $23.5 million per basis point, concentrated in the 5-year and classic Bond contracts. Leveraged funds and the overlapping non-commercial category reduced their short positions in the bond contract by $5 million and $6.5 million, respectively.

US government bond dealers uniformly expect the Treasury Department to keep coupon auction sizes unchanged during the August-to-October period, in keeping with the department’s guidance in April.

The 10- and 5-year are expected to be larger by $1 billion relative to the most recent new issue or reopening, which would result in the following schedule, in billions of dollars.