| Close | Previous Close | Change | |

|---|---|---|---|

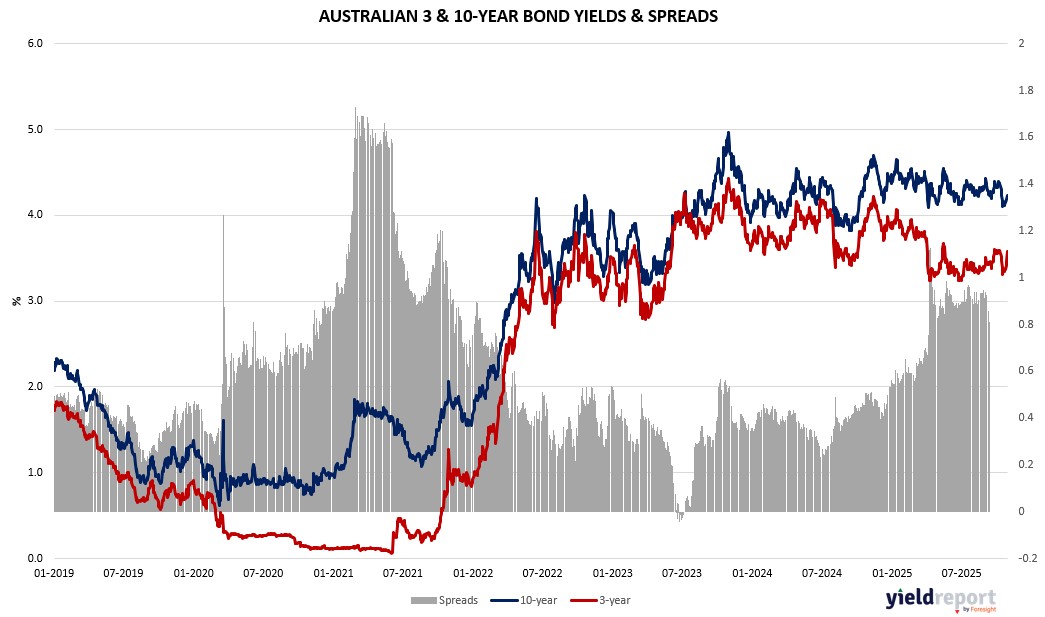

| Australian 10-year bond (%) | 4.235 | 4.179 | 0.056 |

| Australian 30-year bond (%) | 4.893 | 4.856 | 0.037 |

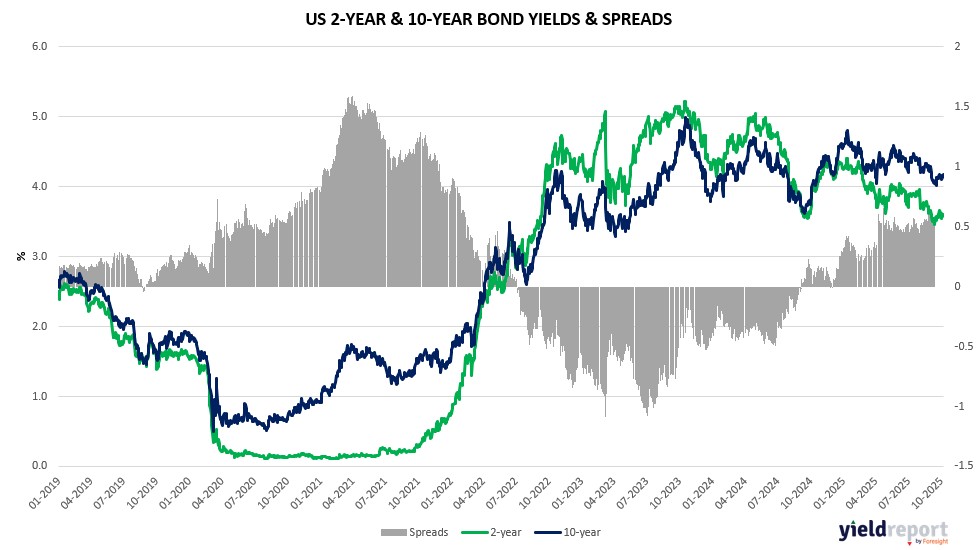

| United States 2-year bond (%) | 3.504 | 3.49 | 0.014 |

| United States 10-year bond (%) | 3.989 | 3.981 | 0.008 |

| United States 30-year bond (%) | 4.5512 | 4.5531 | -0.0019 |

Overview of the Australian Bond Market

Australian government bond yields rose sharply following the CPI overshoot released on October 29, as markets slashed rate cut expectations and braced for a prolonged RBA hold. The 2-year yield climbed 16 basis points to 3.58%, the 5-year advanced 15 basis points to 3.77%, the 10-year rose 13 basis points to 4.30%, and the 15-year increased 12 basis points to 4.61%. The move underscores the “big miss” on inflation, with headline CPI at 1.3% quarterly and 3.2% annually versus expectations of 1.1% and 3.0%, and the closely watched trimmed mean at 1.0% quarterly and 3.0% annually against forecasts of 0.8% and 2.7%. This outcome, described by AMP’s Diana Mousina as a significant deviation for inflation data, marks the first upward blip in the trimmed mean trend, though not yet confirming a reversal, and lands squarely at the upper bound of the RBA’s 2-3% target, eradicating any lingering odds for a year-end cut and pushing back easing timelines.

Macro dynamics blend persistent services inflation—despite some slowing in personal and financial services components—with a higher unemployment starting point at 4.5% in September and a brightening consumption outlook from internal data suggesting solid Q3 and Q4 gains. Westpac Chief Economist Luci Ellis emphasized that the 1.0% quarterly trimmed mean reading is “too high for the RBA’s comfort,” labeling even a 0.9% as a “material miss,” and argued for caution until inflation nears the target midpoint, potentially delaying cuts until February 2026 or later. However, she cautioned against over-interpreting, noting past September quarter upside surprises often reversed in December, and highlighted offsetting factors like a weaker labor market entry point and higher assumed cash rate path that could exert downward pressure on longer-term inflation forecasts. Convera’s Shier Lee Lim echoed the “material miss” sentiment, reinforcing the RBA’s likely decision to hold at November’s meeting and assess further, with the board reluctant to over-rely on the new monthly CPI series amid noise.

Yields track US Treasuries’ post-Fed rise, with global factors like Trump-Xi soybean deals and tariff extensions adding volatility, though China’s pivot to South American supplies tempers US farmer relief. Domestically, the stagflationary mix—a softening economy with sticky prices—heightens RBA vigilance, as Rodda noted the “dangerous combination” complicating policy. Even with potential December quarter payback, the upside surprise elevates near-term risks, though Ellis warns of 2026 surprises from gradual labor softening, latent slack from flat participation assumptions amid upward trends for females and older workers, and benign wages, potentially dipping inflation below the midpoint and opening scope for less restrictive policy later.

Overview of the US Bond Market

Treasury yields climbed sharply after the Fed’s rate cut to the 3.75%-4.00% range, as Powell’s cautious tone on future easing and references to data gaps from the shutdown prompted traders to pare bets on aggressive policy support. The 2-year yield jumped 11 basis points to 3.60%, the 10-year rose 9 basis points to 4.07%, and the 30-year advanced 7 basis points to 4.61%, bear-flattening the curve. The move reflected reduced expectations for a December cut, now priced at roughly two-to-one odds, amid Powell’s acknowledgment of “strongly differing views” within the committee and a “growing chorus” favoring a pause to assess inflation risks.

Bond markets also reacted to mixed economic signals, with available indicators suggesting moderate growth despite the absence of key labor data like payrolls and unemployment rates for over a month. Powell emphasized using private data and surveys to navigate the “fog,” but warned that prolonged shutdowns could delay decisions, potentially affecting the December meeting. Macro pressures include persistent inflation at 2.7% PCE in August, expected to rise toward 3% by year-end due to tariffs, balanced against softening labor trends—private payrolls rose just 14,250 in early October per ADP, signaling near-zero growth. Layoffs announcements from Amazon (14,000), UPS (48,000), and others like Intel and Microsoft underscore a shift to “no hire, more fire,” heightening downside employment risks that Powell said outweigh inflation upside, though he views policy as still modestly restrictive.

Traders anticipate the Fed resuming limited Treasury purchases from December 1 to address liquidity strains, shifting maturing mortgage-backed securities into bills to stabilize the $6.61 trillion balance sheet. In futures, asset managers trimmed net long positions by $23.5 million per basis point, focused on 5-year and longer tenors, while leveraged funds reduced shorts in the bond contract. Dealers expect steady coupon auction sizes for August-October, aligning with April guidance. Broader macro factors, including Trump’s import tariffs and a resilient economy, support bears arguing rates stay higher longer, though deals like potential US-China extensions could ease uncertainty. Consumer confidence edged up, but job concerns linger, with strategists like Tatiana Darie noting hawkish undertones in Powell’s remarks suggesting limits to data-driven easing during the shutdown.